Alternative Investments for Portfolio Management

Hedge Fund Strategy

Equity Strategy

Long/Short Equity

Extract Alpha return,

Return is similar as long-only approach, but standard deviation is 50% lower because short parts hedge risks.

May have leverage.

Dedicated Short Selling and Short-biased

bottom up

Typically take a bottom-up approach short的全是bottom-up

Activist short selling 在short后出报告

Look for poorly managed and overvalued companies 如 浑水

Activist short-selling funds take short positions and publicly share their negative fundamental views.

the stock’s high short-interest ratio and high cost to borrow (“on special”) are very concerning. Both factors suggest significant potential that a dangerous short-squeeze situation.

Dedicated short-selling funds take only short positions.

Short-biased hedge fund focus on good short-side stock picking.

Short-biased strategies are expected to provide some measure of alpha in addition to lowering a portfolio’s overall equity beta.

Equity Market Neutral (EMN)

Construct a zero beta portfolio, so immune to market risk, earn only alpha. Work well under non-trending and bearish mkt, as the strategy can earn stable with low volatility (because of zero beta)

Types:

Pairs Trading: two stocks hedge each other

Stub Trading: long short subsidiary and parent

Multi-class Trading: long short mispriced share classes of the same firm

The availability and cost of leverage are considered in terms of desired return profile and acceptable potential portfolio drawdown risk.

Low return, because market neutral.

Short horizon and active trading, so highly diversified and liquid

High leverage. EMN strategies typically do not meet regulatory leverage limits for mutual fund vehicles. So, limited partnerships are the preferred vehicle.

Work well when the market is vulnerable and weak.

Equity market–neutral managers are likely to have high levels of diversification and turnover ratios.

Sample Text: Overall, EMN managers are more useful for portfolio allocation during periods of non-trending or declining markets. EMN hedge fund strategies take opposite (long and short) positions in similar or related equities having divergent valuations while attempting to maintain a near net zero portfolio exposure to the market. EMN managers neutralize market risk by constructing their portfolios such that the expected portfolio beta is approximately equal to zero. Moreover, EMN managers often choose to set the betas for sectors or industries as well as for common risk factors (e.g., market size, price-to-earnings ratio, and book-to-market ratio) equal to zero. Since these portfolios do not take beta risk and attempt to neutralize many other factor risks, they typically must apply leverage to the long and short positions to achieve a meaningful return profile from their individual stock selections. 因为风险小,return小,所以加杠杆才能扩大收益

EMN strategies typically deliver return profiles that are steadier and less volatile than those of many other hedge strategy areas. Over time, their conservative and constrained approach typically results in a less dynamic overall return profile than those of managers who accept beta exposure. Despite the use of substantial leverage and because of their more standard and overall steady risk/return profiles, equity market-neutral managers are often a preferred replacement for fixed-income managers during periods when fixed-income returns are unattractively low.

Event-Driven Strategy

Merger Arbitrage

Merger arbitrage is a good uncorrelated source of alpha.

A: Acquirer

T: Target

If the merger successes, then use the T stock to A stock, and take cost difference.

If the merger fails, then prices should revert back to their pre-merger announcement levels

Cash-for-Stock

Buy target, T

Stock-for-Stock

Buy share of T, sell share of A. Because A issue share to buy T, then share price to A decrease, and demand of A stock increase, so A price increase.

Overall Characteristics:

If the deals fail, this strategy has market sensitivity and left-tail risk attributes.

The preferred vehicle is limited partnership because of merger arbitrage’s use of significant leverage, but some low-leverage, low volatility liquid alts merger arbitrage funds do exist.

typically apply 3 to 5 times leverage in order to achieve lowdouble-digit returns.

Kind diversified, because the Acquirer and Target together is a composite, pretty much irrelevant with other portfolio. Thus, diversified.

特点:

expose to left-tail risks,因为若失败了,损失格外大

Leverage:高杠杆(只要是arbitrage的,都高杠杆)一般3-5倍

Distressed Securities

Focus on firms that are (1) in bankruptcy, (2) under financial stress. Focus on:

Recovery Value

Undervalued Debt Securities

Characteristics:

High return, but return is cyclical. The distressed securities strategy works better under postive Econ environment.

High level of illiquidity

Low leverage

Sample Text: Event-driven strategies, such as merger arbitrage, tend to be exposed to some natural equity market beta risk. Event-driven merger arbitrage strategies have market sensitivity and left-tail risk attributes. Also, while event-driven strategies may have less beta exposure than simple, long-only beta allocations, the higher hedge fund fees effectively result in a particularly expensive form of embedded beta. 由于会受tail risk影响,而全部白给

Relative Value Strategy

Equity market neutral strategy

convertible bond arbitrage

Fixed-Income Arbitrage

Yield Curve Trades: taking long and short positions at different points on the yield curve

Sample Text: For yield curve trades, the prevalent calendar spread strategy involves taking long and short positions at different points on the yield curve where the relative mispricing of securities offers the best opportunities, such as in a curve flattening or steepening.

Carry Trades: long a higher yielding security and shorting a lower yielding security

Sample Text: Carry Trade: A classic example of a fixed-income arbitrage trade involves buying lower-liquidity, off-the-run government securities and selling higher-liquidity, duration-matched, on-the-run government securities.

Return profile is like put option.

If the strategy unfolds as expected, it returns a positive carry plus a profit from spread narrowing.

If the spread unexpectedly widens, then the payoff becomes negative.

Convertible Bond Arbitrage

long short volatility 与 long short option方向一致,因为option 与 vol 正相关

Convertible bond = straight debt + long equity call option

Conversion value = stock price * conversion ratio

If conversion value > bond value, then in-the-market

Vice versa

Conversion ratio = # of share a bond can exchange

Convertible bond is complex structured, so generally under-valued. Buy Convertible bond, short corresponding # of stocks.

If the convertible bond’s current price is near the conversion value, then the combination of a long convertible and short equity delta exposure will create a situation where for small changes in the share price and ignoring dividends and borrowing costs, the profit/loss will be the same.

Opportunistic Hedge Fund

Global Macro Strategy

Top-down, fundamental model, trend driven 追逐全球趋势

Heterogeneity 包括多种 assets 特异

leveraged 用杠杆放大风险

受制于全球经济risks,so perform worst during recession 。no diversified in crisis 全球金融危机时,全完蛋

Managed Futures

exotic contract: futures on weather / derivatives on carbon emission, etc.

time-series momentum trend 与过去自己的 performance 比

Absolute basis: can net long / net short

Sample Text: Time-series trading strategies are driven by the past performance of the individual assets. The manager will take long positions for assets that are rising in value and short positions for assets that are falling in value. Positions are taken on an absolute basis, and individual positions are determined independent of the performance of the other assets in the strategy.

Cross-Sectional Momentum 与其他 bond 的 relative value 比

Net zero or market neutral

Work well when market is out / underperformed relative to other mkt 因为net zero

Sample Text:

Such an approach is generally implemented with securities in the same asset class, which is corporate bonds in this case. The strategy is to take long positions in contracts for bonds that have risen the most in value relative to the others (the bonds with the narrowing spreads) and short positions in contracts for bonds that have fallen the most in value relative to the others (the bonds with the widening spreads). Cross-sectional momentum strategies generally result in holding a net zero or market-neutral position. In contrast, positions for assets in time-series momentum strategies are determined in isolation, independent of the performance of the other assets in the strategy and can be net long or net short depending on the current price trend of an asset.

cross-sectional strategies, where the position taken in an asset depends on that asset’s performance relative to the other assets.

Characteristics

Both: Derivative 多 -> leverage 多 -> 风险多,volatility

Both: 但是因为有derivatives可以hedge 风险,所以当经济差的时候 left tail的风险可控,right-tail skewness

Both are highly liquid

Managed futures take more systematic approach

global macro managers are more discretionary

Specialist Strategies

Volatility Trading

Roll down: Source and buy cheap volatility and sell more expensive volatility, earn premium

Equities and volatility are negatively correlated. In order to hedge the equity exposure in the portfolio, a long volatility position is necessary.

VIX option和stock之间可以diversify

Strategy:

Outright long volatility, 买期权 with delta hedging of the gamma exposure 交易所交易

OTC options 期限maturity长于2年的,OTC交易

VIX index

OTC volatility swap / variance swap

Characteristics:

Long volatility strategy is a convex strategy. Skew to the right 凸性策略,比较好 (期限越长越好

Liquidity 交易所交易的liquidity好,但期限短。OTC liquidity 差,但期限长

options 自带 leverage

Reinsurance and Life Settlements

insurance contracts are not liquid and difficult to sell.

the insurance and reinsurance themselves are independent with the market, so uncorrelated with the equity mkt. Thus, diversified

Hedge Fund 会一次性买一个 pool的保单, pay lump sum fee 一次性一笔的买断费,然后pay ongoing premium payments 按期付保费,在受保人die 的时候挣 death benefits:

Hedge funds look for policies in which the ongoing premium payments to keep the policy active are relatively low. 每期支付保费少的

Hedge funds also look for life settlements where the surrender value offered to the insured individual is also relatively low,不懂 surrender value 指的是提前终止 提出来的钱。可能是相对应,收益人想要提前终止,要把钱还给收益人,因为之前一次买断过,收益人会找hedge fund surrender

and the probability that the designated insured person is likely to die earlier than predicted by standard actuarial methods is relatively high. 先死给的理赔多

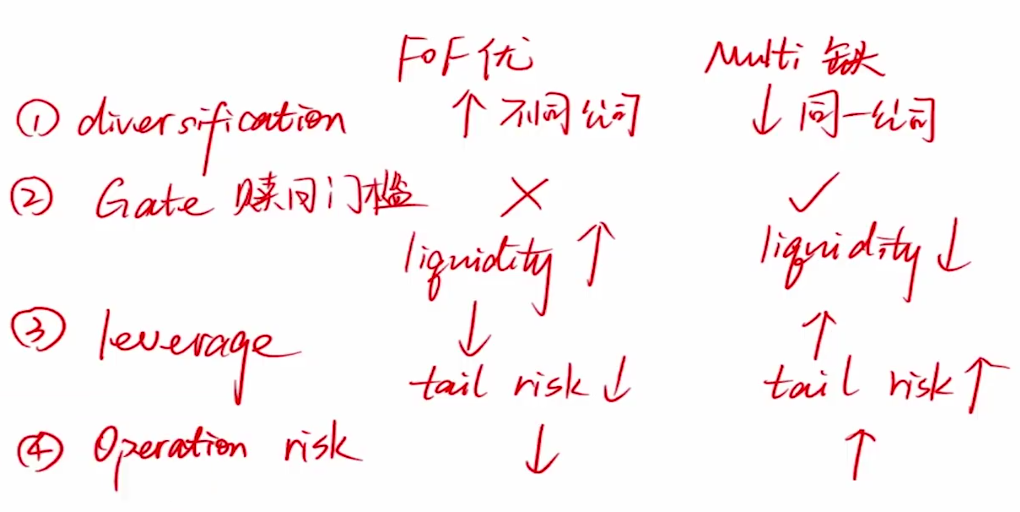

Multi-Manager Strategy

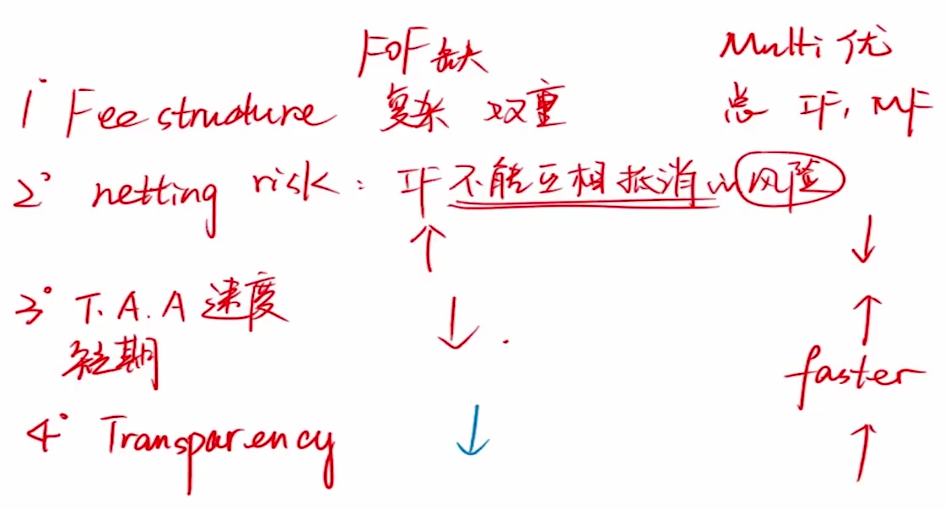

FoF一定有 double layer fees: FoFs have double layers of fees without being able to net performance fees on individual managers. The FoF investor always faces netting risk and is responsible for paying performance fees that are due to winning underlying funds while suffering return drag from the performance of losing underlying funds. Even if the FoF’s overall performance (aggregated across all funds) is flat or down, FoF investors must still pay incentive fees that are due to the managers of the winning underlying funds.

MSF (Multi-Strategy Fund) 的 fee 可以内部抵消(gain 的 loss 的可以net)The fee structure is more investor friendly at MSFs, where the general partner absorbs the netting risk arising from the divergent performance of the fund’s different strategy teams. This is an attractive outcome for the MSF investor because (1) the GP is responsible for netting risk and (2) the only investor-level incentive fees paid are those due on the total fund performance after netting the positive and negative performances of the various strategy teams.

MSF更方便切换战略做TAA,因为内部有自己的小团队。MSFs can reallocate capital into different strategy areas more quickly and efficiently than is possible in FoFs, allowing MSFs to react faster to real-time market impacts. This shorter tactical reaction time, combined with MSFs’ better strategy transparency, makes MSFs more resilient than FoFs in preserving capital.

FoF的FM更多,所以operational risks diversidied,但是MSF相对应内部有一大堆FM,还是有较高concentrated operational risks. MSFs have higher manager-specific operational risks than FoFs. In MSFs, teams of managers dedicated to running different hedge fund strategies share operational and risk management systems under the same roof. This means that the MSF’s operational risks are not well diversified because all operational processes are performed under the same fund structure. FoFs, in contrast, have less operational risk because each separate underlying hedge fund is responsible for its own risk management

More Sample Text:

Multi-strategy managers like Hedge Fund B can reallocate capital into different strategy areas more quickly and efficiently than would be possible by a fund-of-funds (FoF) manager like Hedge Fund C. The multi-strategy manager has full transparency and a better picture of the interactions of the different teams’ portfolio risks than would ever be possible for FoF managers to achieve. Consequently, the multi-strategy manager can react faster to different real-time market impacts—for example, by rapidly increasing or decreasing leverage within different strategies depending upon the perceived riskiness of available opportunities.

The fees paid by investors in a multi-strategy fund can be structured in a number of ways, some of which can be very attractive when compared to the FoFs’ added fee layering and netting risk attributes. Conceptually, FoF investors always face netting risk, whereby they are responsible for paying performance fees due to winning underlying funds while suffering return drag from the performance of losing underlying funds. Even if the FoF’s overall performance is flat or down, FoF investors must still pay incentive fees due to the managers of winning funds.

Multistrategy funds typically use more leverage and have more volatile return profiles than funds of funds.

Multistrategy funds have faster reaction times for tactical allocation changes.

Funds of funds potentially offer a more diverse mix of strategies.

Analysis of Hedge Fund Strategy

Conditional Factor Risk model - turbulent market period

in order to analyse whether hedge fund risk exposures that are insignificant during calm market periods may become significant during turbulent market period.

The Unexplained Returns are (1) alpha; (2) alpha (FM investment skills); (3) omitted factor; (4) random error

Conditional Factor Risk Model

reg HF return on

Equity Risks (S&P500) 整个市场的风险

Currency Risks (USD) 外汇风险

Credit Risks (CREDIT) 债券风险

Volatility Risks (VIX) Options风险

It is a conditional model as there is a dummy variable that distinguishes between calm market and turbulent market condition. 用dummy区分market condition

Traditional Portfolio: 60/40 Equity/Debt

If hedge fund is added, there could increase Sharpe and Sortino ratios, and diversify risks. 降低风险 提高收益

Risk-Adjusted Measure

high Sharpe and Sortino Ratio 指标好的策略

Systematic Futures

Equity Market Neutral

Global Macro

Event Driven Hedge Fund Strategy

Do not enhance risk-adjusted performance 指标不好的策略

FoF

Multi-Strategy

因为 分散风险 risk 降低,所以 return 也降低了

Drawdown

the higher the drawdown, the greater the tail risks

Event-driven (MA) 策略,是为了挣 high earning,若MA失败,会暴露大 tail-risks

Relative Value: 因为high leverage, 所以 market volatile 会带来大drawdown

Alternative Investment

Timber

Earn: Capital Growth, Inflation Resistance

Risks: Even Risks <- Insurance

Commodity * 4

Metals

Energy

Livestock/ Meat

Agriculture

Invest in (1) future (2) 实物 farmland

Real Estate

Public real estate has had a fairly high, positive correlation with equities, as well as a high, positive equity beta. In contrast, fixed income has broadly had a negative correlation with equity and a small but negative equity beta. Switching from fixed income to real estate will likely decrease portfolio diversification and increase return volatility.

Investment Consideration

Risk Characterisitcs

MVO might be s.t. constarints

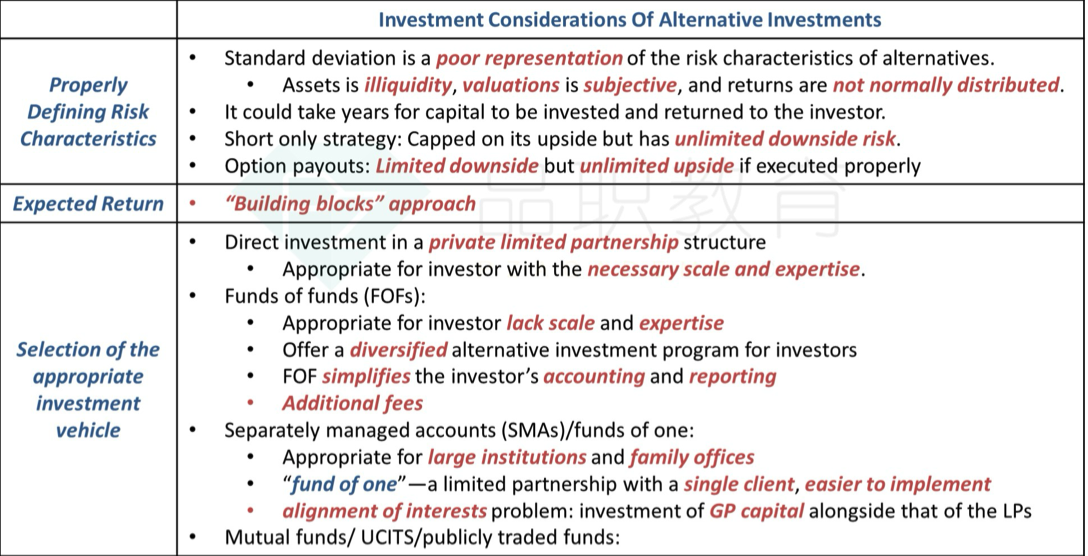

Returns are not normally dist

Might not be able to allocate assets as target

Establishing Return Expectation

limited data availability

Investment vehicle

LP 出钱,GP 管理 参与运营

Large investors, invest in LP

FoF <- lack of enpertise investors (pros: access and diversify, cons: additional fees layer)

Separately Managed Accounts (SMA, funds of one) 由GP独立管理,专户管理,给 large investors

Open-ended Mutual Funds and UCITS, give smaller investors access to alternatives 降低准入门槛,给小invetors

Liquidity

Notation: all 站在 PE fund 的 GP 的角度。GP 是基金经理,LP 是出钱的金主。GP call就是 fund 在要钱,distribute 就是把钱返给 LP

Commitment 承诺出资,如commit 10b

Call 召款,相当于花3年把10万投完,每投一笔之前都要 call

Calldown Period,相当于召款周期

Committed Captial (10b) = Paid in Capital (已经call的,已经投入的) + 未投的

Distribution

P.S. Sample Text:

"In a bear market, GPs may call capital at a higher pace and/or make distributions at a slower pace than had been expected. This suggests that in addition to the base case scenario planning, the analyst should develop an additional set of assumptions with faster capital calls and lower distribution rates."

Drawdown Structure

Captial Call and Distribtuion do not have predertermined schedule , 打款和提款的时间都没有确定

Opportunity, risks of missing a capital call 没办法按时打款,而错过投资机会的风险

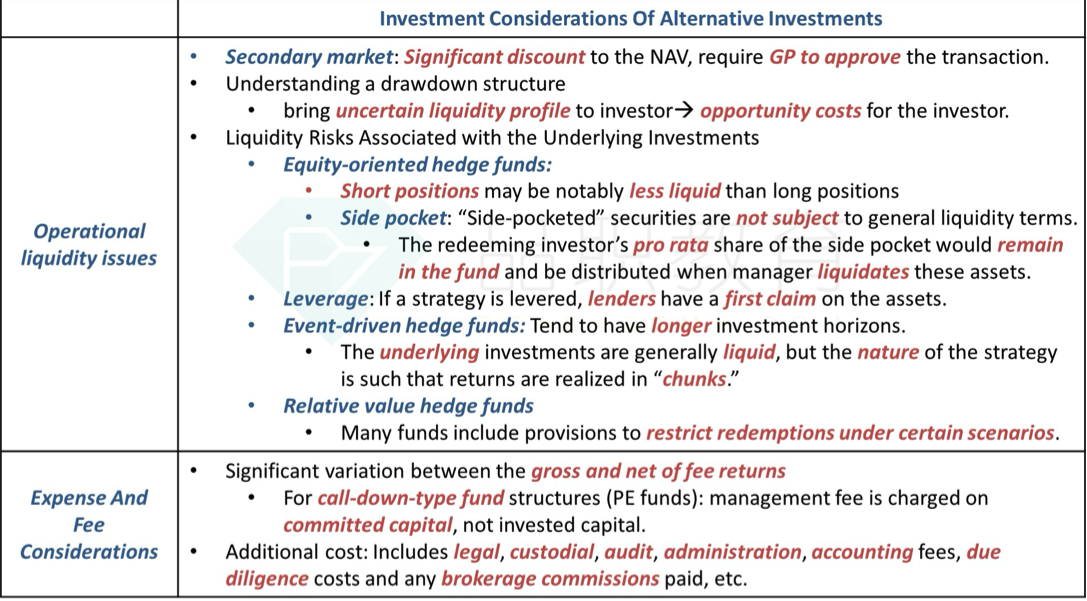

Side-Pocket. 侧袋账户。普通账户的钱可以按redemption polcy赎回,但是 side pocket的不行。所以 若 side pocket钱越多,则流动性越大

Types:

Event-driven Strategy: frequent redemption period

Relative value funds: hold significant portions of illiquid investments,

Leverage: Margin calls may force a leveraged fund to sell its most liquid holdings

Expense and Fee

2/20

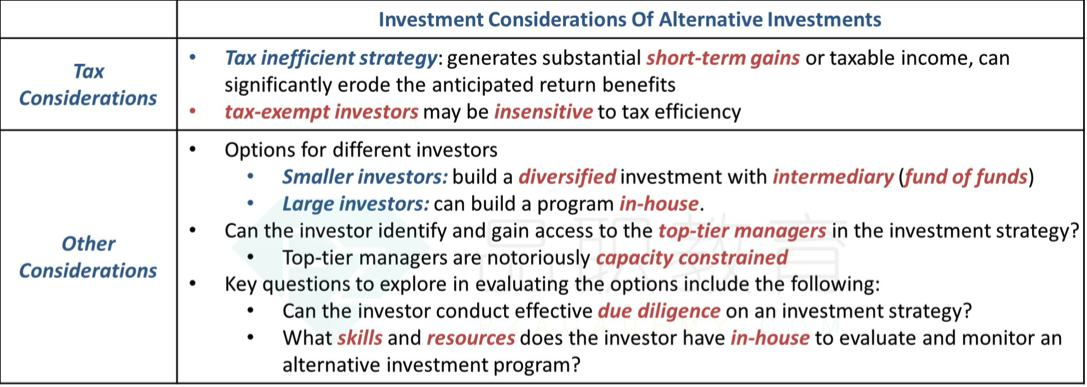

Tax Consideration

Build v.s. Buy

Asset Classification

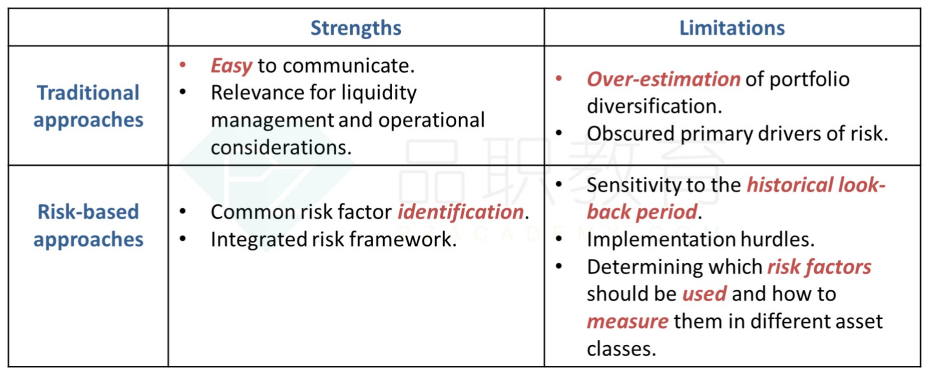

Traditional Approach 看表面

按流动性分:private 的流动性都差,public 的都好,包括REITs / Public Real Estate,包括上市公司股票的HF

按通胀,高通胀 real estate / commodity, 高通胀+low growth : inflation-linked bond TIPS, Gold

Limitation: 主观判断投资的asset,容易 over-estimate the diversification

doesn’t group assets together based on a few shared characteristics. 不会通过risk factor 对asset分类,如 traditional approach 会对待 high yield bond 和 gov bond 会在同一个 fixed-income portfolio中。但是 risk-based approach 会把两种bond 不同对待

Risk-Based Approach 和 risk factor 回归

因为是回归,所以 sensitive to historical look-back period

如果说: Risk-Based Approach does equally well accounting for risk levels of alternative assets as it does for publicly traded assets.

False: 因为 PE or Alternatives 不是定期report,data are non-continuous, so use appraisal data. Data are smoothed, 低估 vol,低估 corr, making diversification benefits

stale pricing和smoothing是同源的。因为另类资产因为没有活跃的交易价格,因此定价一般都是过时的(stale pricing),所以会用 appraisal data估算另类资产的价值,导致另类资产的收益率是smoothing的,从而在进行MVO的时候会把过多的权重给另类资产。 MVO会因为另类资产stale pricing的原因,低估风险,因此会把过多的权重配给另类资产。这是没错的。

Investment Consideration

Suitability Consideration

Investment Horizon: long

Enterprise: Skilled Manager

Governance: formal investment policy

Transparency: low

Sample Text: PE, real estate, HF 的 transparency 就是低,得认

Investors in alternative investments, such as private equity, direct real estate, and hedge funds, should not expect transparency in holdings or strategies; rather, investors in these asset classes must be comfortable with a lack of transparency in specific strategies and a “blind pool” of assets. If full transparency is desired or required, alternative investments will not be suitable.

用 appraisal data: Returns from private equity are based on infrequent reporting and typically use appraisal values, resulting in a smoothing of returns and less accurate return volatilities. In comparison, investment-grade fixed-income returns are based on transaction prices, resulting in more accurate return volatilities.

不能用 s.d. 分析风险,因为 risk 不对称

In sum, alternatives are suitable to high risk tolerance investors.

Soft Skills

communication skills

social skill, interpersonal skills

education and coaching skills

Business development and sales skills, lead new business development

P.S. 与 soft skill 对应的是 technical skills 包含: capital market proficiency, portfolio construction ability, financial planning knowledge, technology skills, language skill 多会说一种外语

Approach to Asset Allocation

Monte Carlo Simulation

MVO

establish limits

incorporate downside risks (mean-CVAR optimisation)

consider skewness

Cons: sensitive to small change of inputs

Risk Factor Based Optimisation

Liquidity Planning

Capital Contribution = Rate of Contribution * (Capital Commitment - Paid-in-Capital)

Distribution = Rate of Distrubiton_t * NAV * (1 + growth rate)

NAV_1 = NAV_0 (1+g) + Capital Contribution - Distribution

NAV

NAV net asset value 资产净值 , by BASE

A: Capital Contribution 打款 <- Call,

Capital Contribution = Rate of Contribution * (Capital Commitment - Paid-in Capital)

承诺要付的CC - 已经付的 Paid-in

Avoid Cash Drag

为了保证 Capital Contribution / call 的时候有钱可以投进去,又避免持有 cash 导致 return过低。

在 call 之前,把准备投

投 PE 的钱,投 Public Equity

投 RE 的钱,投 REITs (public real estate investments 为大类,其中 REITs 是其中之一)

Prepare for Unexpectation (Stress-test)

Stress test for unexpected events

Performance Evaluation

Benchmark:

Custom Index Proxies (i.e. MSCI world index + 3%)

Peer Group Comparison, percentile of Peers

Others:

Private Equity, Credit, Real Estate 流动性最差的三种 用 IRR ,

Cons 受CF出现的时间点影响,只考虑了 percentage 没考虑 Value Amount

Private Equity 还可以用

直接把现金流相加,不折现。Pros: 不受CF时点影响,Cons: 但是没考虑Time Value of Money

Monitor the Investment Program

投之前需要考虑的

Key person risk 关键FM离职的风险,p.s. 对于量化基金 关键的是model,所以Key Person Risk 不大

Alignment of Interests, whether FM's interests remain closely aligned with their own 是否执行之际的interest

investor 要理解 FM 的 Risk Management Philosophy 不会随意 提取钱出来

Investor gauge the profile