Equity

value & growth.

Growth typically means fast growing company, that is normally overvalued but have potential to create unexpected growth

Value typically refer to company that have already been large and mature, but are overlooked by investors, book value is high-qualitied, but market value is low.

Overview

Income associated with an Equity Portfolio

Dividend Income

Securities Lending Income: lend to short seller 借出后 div 和 voting right 都不归自己了, 但是可以主动 get cash equivalent to the dividend amount

By investopedia:

Rights and Dividends: When a security is transferred as part of the lending agreement, all rights are transferred to the borrower. This includes voting rights the right to dividends, and the rights to any other distributions. Often, the borrower sends payments equal to the dividends and other returns back to the lender.

dividends on loaned stock are compensated by the borrower

Reinvestment return of cash collateral are received

Dividend Capture

buy a stock before ex-dividend date

hold it throng the ex-dividend date

sell that stock after ex date

Writing Options

write Covered call: long stock + write a call = + S - c

Cash-coverd put: sell a put + buy bond, at same strike price = K - p

Fees

Management Fees 与业绩无关,只与 AUM 相关

Performance Fees (incentive fee): high water mark

Administration Fees, which is part of the management fees 如给证交所注册等

Marketing and Distribution fees

Trading Costs

explicit cost: broker com mission, stock exchange fee, taxes, etc , directly visible

implicit cost 在计算cost过程中不算,但是依然存在 : bid-ask spread, price impact cost from transaction 由于买卖量大导致价格被推高或拉低 造成的成本 Delay cost (slippage costs) 由于延迟下单导致的cost

弥补 trading cost 的方法

Dividend Capture

Security Lending

Wirite Options

Shareholder Engagement 股东主义

Shareholder engagement refers to investors and managers interacting with companies in ways to potentially favourably impact the stock price.

Pros: (1) improve efficiency (2) get internal information about that firm (3) for active and large investors, so benefits all shareholders, and (4) good for non-financial interests such as ESG.

Cons: (1) time consuming and costly, (2) aim to increase stock price, so focus on short-term goals, not long-term goals, (3) acquisition of material non-public info, so may have risks of insider trading (4) conflict of interest between large and small stakeholders.

Passive Equity Investment (选 benchmark 拟合)

Overall

Tracking Error T.E. (active risks

As

So, portfolio 偏离 Benchmark, 则 T.E 提升

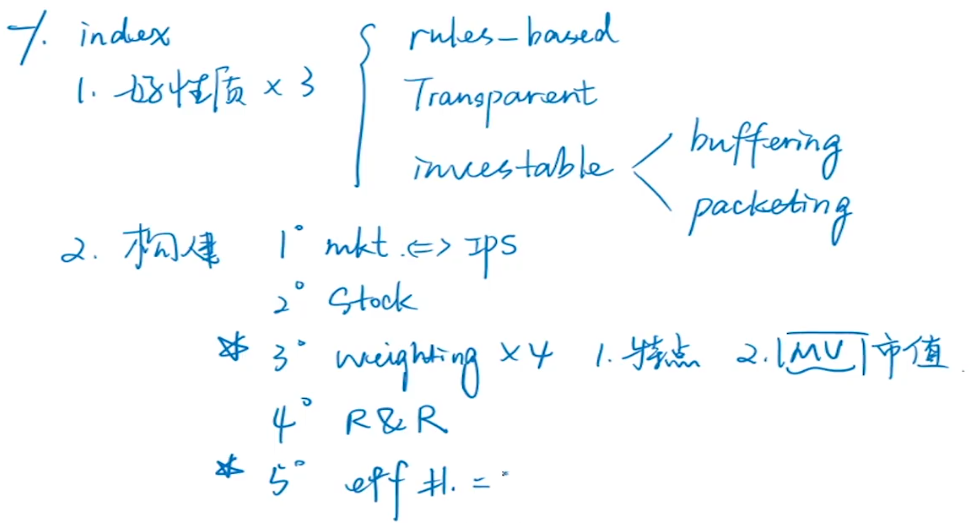

Indexes as a Basis for Investment

Rules-Based: follow the rules of weighting scheme, rebalancing frequency, etc

Transparent

Investable 如 HS300为市值最大的300只,那么300th可能会变化,此时 passive invest to replicate the index 会导致300th经常更换而带来transaction cost

To limit stock migration problems and to mitigate trading costs, 两个方法 buffering & Packeting

Buffering 缓冲区: establishing ranges around breakpoints that define whether a stock belongs in one index or another. 在 rebalance 和 reconstitution时设置一个边界,可以减少 trading cost

如 XX300 指数,设置 buffer意味着,到top200 才纳入,跌出 400 才剔除

左右两边取一个范围 构建更宽的边界,达到更大的边界才会纳入或剔除。

Packeting: splitting stock positions into multiple parts

如果 growth 转变为 value 了,那么先将一部分纳入 value index,等到下一个 reconstitution date 才把所有的转入

不能计算成分股权重的benchmark:

FOF, 2. Geographic Linked Approach . those two are not investable

free float: market cap 加权的指数,可能不能买回来,所用用 free float 的方法把权重买回来。股票市值中流动部分的比率

Determine the Market Exposure (based on IPS)

Market Segment (domestic or international, developed or emerging or frontier, etc)

Capitalisation (size factor): market size, large-cap, mid-cap, etc

Growth versus Value (style factor): choose exposure to growth stock (high PE high PB) or value stock (low PE PB)

Other risk factors

Stock Index Benchmark

Stock Inclusion

Exhaustive 穷举选取一定范围内所有的stock

Selective Approach 选取特定的stock

Weighting Methods

Market-Cap Weighting (S&P500) (偏向large cap stock)

Liquidity-weighted 这种方法会 heavily weighted Large-cap stocks, as they are higher liquid

Free-Float weighting 考虑在流通的 stock 的总市值(限售的 stock 被剔除了)

市值加权的结果接近于MVO,所以efficient,非系统风险 is diversified

Mean-variance efficient: x-axis is s.d.; y-axis is return 画出CML curve

Offer the highest return for a given level of risks

有 investment capacity,因为按市值加权,所以不受 investment capacity的限制(不像equal weighting一样)。与Equal weight 相对应

假设市场有效 market efficient ,与fundamental weight 相对应

Price Weighting (Dow Jones, Nikkei 225) (偏向高价股 high price stocks)

股数相同,都为 k 股,所以为 price weighted

高价股权重会更高,对 index 影响更大。growth stock (高价股) 往往 price 更高,所以 growth stock 在 index 中权重更大。P.S. Growth Stock 指的是有增长潜力的,如AAPL 股价一般比较高。Value Stock 指的是 price 被低估的,P/BV 小的

拆股 split 等影响 price,会影响 price weighting。但 拆股不会影响 market cap,所以不影响 market-cap weighting。

Rebalance weights 因为拆股会带来价格减半,但是实际上 index 不应受到影响,所以要调整 被拆 stock 的 weight 使得拆股前后 index 数值一致,然后反推 weights。所以 price weighting 会调整 weights

Equal Weighting (偏向小盘股 small cap stocks)

Least concentrated 不会受市值影响

Slow changing sector exposures, less reconstitution 因为无偏好,所以不会因为 index 内股票代表性不足而重构,所以 重构较少

受small cap 影响更大,因为小盘股 volatility大,所以此指数也 vol 大。Affected by price change, so small stocks (, which are highly volatile) would make the index highly fluctuated. 小市值股票会带来 index 波动

Require regular rebalancing. I.E. 如果 Price Increase,那么在 index 中 MV 上升,所以 weights 上升。要保证 equal weight 就需要 卖出该 stock。所以经常需要 rebalance。且 高抛低吸 contrarian

Limited Investment Capacity (1)因为小盘股多,流动性不好(2)需要老 rebalance 所以 trading cost 高 (因为要等权买,此时买小盘股时也需要买很多,可能流通的股不够,所以缺少investment capacity。market cap weighting 有好的 investment capacity)

minimise single stock concentration risks.

Randomise factor misplacing

Fundamental Weighting (上证50)(偏向 低价股 low price stock)(虽然叫 fundamental 但是实际上,假设是市场不有效 assume misplacing,market inefficient, 通过市场上的错误定价 而选择特定的 tilt 挣钱

weight stocks by fundamental factors

Contrarian

value tilt 偏向价值股 ,price 低,所以 dividend ratio

P.S.:

If Tax-Exempt, then equal-weighted 的 trading cost 的和 capital gain 的税被免了,所以 equal-weighted might get superior return

Market-cap weighted & Fundamentally weighted

Shared characteristics: low cost, rules-based, transparency

Different: market-cap-weight is based on EMH 在 CML 上。但 fundamentally weights exploit inefficiencies in market pricing.

Rebalancing and Reconstitution

Rebalance: reweighs

Reconstitution: add or remove new stocks

Rebalance and Reconstitution create turnover and transaction costs 这俩都会带来 transaction cost 成本提升

turnover for developed country's stocks & large-cap index are infrequent so less cost

benchmark using stock selection rather than exhaustive inclusion makes high turnover.

Concentration

Effective Number of Stocks 真正在市场上能影响股票价格 的 #,所以

the greater the efficient #, the more diversified

the lower the efficient #, the more concentrated

Effective # <=>

if equal weighted,

Passive Investment Strategy (Smart Beta)

因为是 passive strategy ,所以目的是与 benchmark 收益一致。

但是 实际操作上 要 face transaction cost, bid-ask spread etc。

所以 T.C. (transaction cost) 会导致portfolio 收益降低。

那么为了保证 port return 与 benchmark return 一样,就需要做一部分的 active management。如多投好的factor,挣positive active return;或者少投差的factor,挣positive active return

只需要一点点的盘子,做 active 来 cover transaction cost,所以主要还是 passive,smart beta 部分只有一点点

Pros and Cons of Smart Beta

Pros:

pure exposure to specific segments

less costly T.C. than active management

can have factor rotation that incorporate investors' view

Cons:

concentrate risk exposure

have tracking error

T.C. or management fee is less than active management but greater than passive cap-weighted investing

Factor-based Strategy

Most benchmarket returns are driven by factors, which are risk exposures that can be identitfied and isolted. 因子之间 identified , isolated

Growth factor

Value

Size

Yield

Momentum

Quality

Volatility

Three Passive Factor Strategies

Reutrn Oriented Strategy 为了挣钱

Divident Yield Strategy

Momentum Strategy

Fundamentally Weighted Strategy (value > Growth)

Risk-Oriented Strategy 为了降低组合的风险

Volatility Weighting

Minimum Variance Investing

Pros: lower risks

Cons: use historical data may not indicate future

Diverisifcation-oriented Strategy

Management fees:

Broad market index < passive factor-based < active strategy

Passive factor-based strategy provide pure exposre

Approaches to Passive Equity Investment (Tools + SMA)

Tools: Pooled Investment

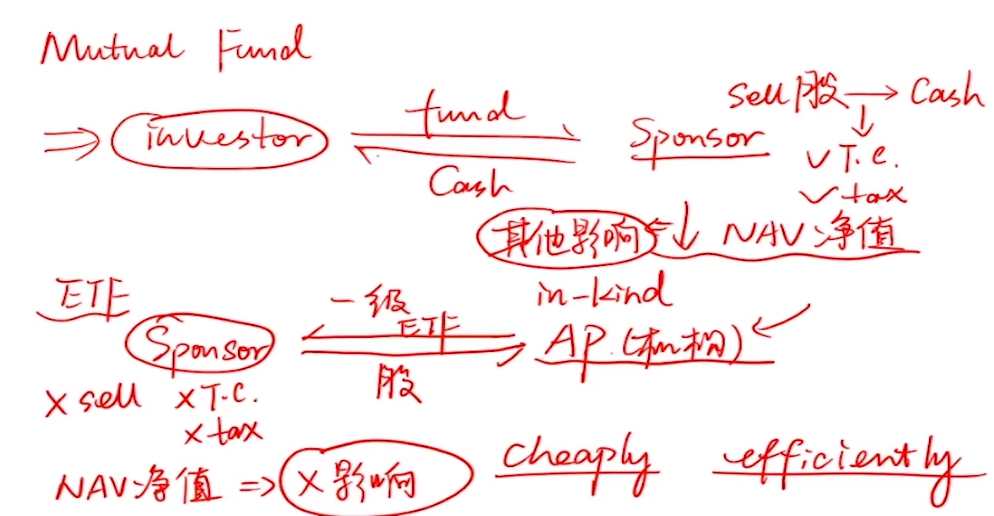

open-end mutual fund

买卖价格:(substription, redemption 申购赎回) 如在当日交易日前买,以当日3点收盘价 NAV 为成交价

买卖地方:可以在 market place买 去找蚂蚁金服买,要费, 2. Advisor 买 直接找直销账户买

ETFs

可以在交易所买,所以基金份额可以在二级市场交易

可以在交易所 做空,融资融券,leverage, short 因为可以在交易所交易。不像 open-end mutual fund 只能找基金公司申购赎回,不能用于申购赎回

不用现金交割,而是用 in kind 以物易物的方式交割,sponsor 拿一篮子stock 换 ETFs。也因此没有现金的 gain / loss realised,gain loss are un-realised 所以可以达到 tax defer 的好处

对比 mutual fund & ETFs

ETFs v.s. Mutual Funds

ETFs' redemption 拿ETFs换股,所以其他人 包括 NAV不会被影响,所以 redemption is more cheap and efficient, but Mutual Funds 会拿钱换stock

ETF s higher transaction costs from commission and bid-ask spread. 因为可以在二级交易 and might be illiquid in some secondary market

Derivatives

避免额外的 cash 产生 cash drag 拖累 fund收益

Completion Overlays: 用于建仓

Rebalancing Overlays: 用于调仓

Currency Overlays: 用于调整 FX risks

Pros:

Quick, efficient, cheap

liquid

Easy to leverage

避免 cash drag

Cons:

need roll over 因为有到期日,需要不断roll 展期

position limit, restricted by regulator

mgiht not be qualified to be traded in exchange. 可能无法在 交易所交易. OTC might be exposed to counterparty risk

basis risks 期货和现货价格的差距 can increase trading error 当 future/forward 的 selling date != expire date 可能会有 tracking error

Portfolio Construction

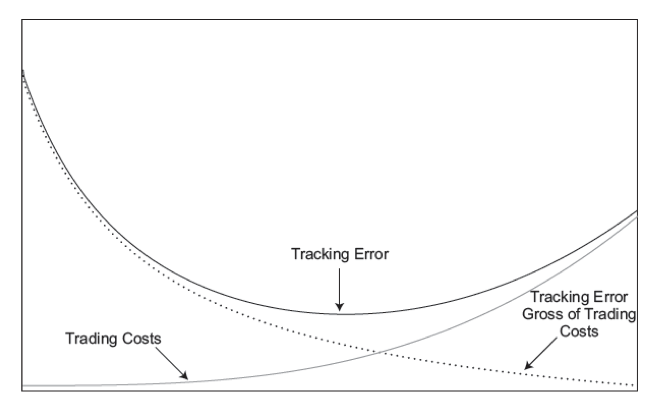

Full Replication

Full replication is preferred for indexes with small numbers of liquid stocks 因为 less liquid stock 会大幅增加交易成本T.C.

Pros: Closely matches the index return, and simple

Cons: Index does not consider trading cost, but build your own portfolio would take T.C.. Those T.C. would bring Tracking Error T.E.

whenever the index changes and we have to fully replicate by rebalancing or reconstituting, there would be T.C. and T.E. 当指数变带来重组和调权重的时候,会带来T.E.

如果复制的 stocks 少,则复制的不准确,T.E. 大,如果复制的stocks 多,则 T.C. 大,T.E. 大。That is a tradeoff

Stratified Sampling 分组抽样

把 constituent stock 分为 subset,之后从中选取。 Create strata that are mutually exclusive and exhaustive 遍历但不重叠的分组

Pros: avoid high cost of full replication, easy

Cons: size of strata might be matter, and high tracking error

Optimisation

Using Algorithm to find parameter

The optimisation process accounts explicitly for the covariances in the portfolio constituents and results in lowering tracking error when compared with stratified sampling alone.

Pros:

lower tracking error than stratified sampling

Can account for the covariance / correlation for diversification

Cons

Historical data, corr might change

Dynamic optimisation would also be costly

Might be mean-variance inefficient 如果 objective func 不是 mean-var optim。解决 可以先mean-var optim 再走别的 opti

Blended Approach

其中一部分股票 full replication ,其他股票 optim or stratified。三种方法排列组合

Sum

波动率,stratified因为只选了部分,所以波动率大

full replication < optimisation < stratified sampling

Transaction Cost

Optimisation < stratified sampling < full replication

Causes of Tracking Error T.E.

Number of Constituents

Number of constituents 成分股数越多, Tracking Error 越大。因为 illiquidity 大,且 T.C. 来自 rebalance and reconstitution 大

Fees and Trading Costs

Management Fees, Commissions or Bid-ask Spread

illqudity

Higher Expense Ratio

Cash Drag

由于指数不含cash,但是portfolio中往往有cash,且cash 部分没有 return,因此 portfolio 整体的return 会被拉低

Intra-day Trading

index往往是用 Close price 算,但是自己构建 portfolio 是要自己交易的,价格为 intra-day price,与close price 可能不同

In no cost world, Full replication produce lowest T.E., but real world there has be a tradeoff between # of constituents and Cost.

Control Tracking Error by

Minimising the trading cost

Netting investor cash inflows and redemptions 以减少 cash drag 的影响

Using equalisation tools like derivatives to compensate for cash drag 用 cash 去买 derivative 叫 equitisation,减少 cash drag 的影响

Sources of Return and Risks

Attribution Analysis 见后面reading

Security lending 借给 short seller

The securities lending income can be an additional return, and then reduce T.C. and T.E.

但是 由于借出了stock,会面临 credit risks, mkt risks, liquidity, etc 所以可能要 collateral 去弥补风险

Activism and Engagement

Passive Investment 也可以有 积极的股东主义 去 increase return

Active Equity Investing

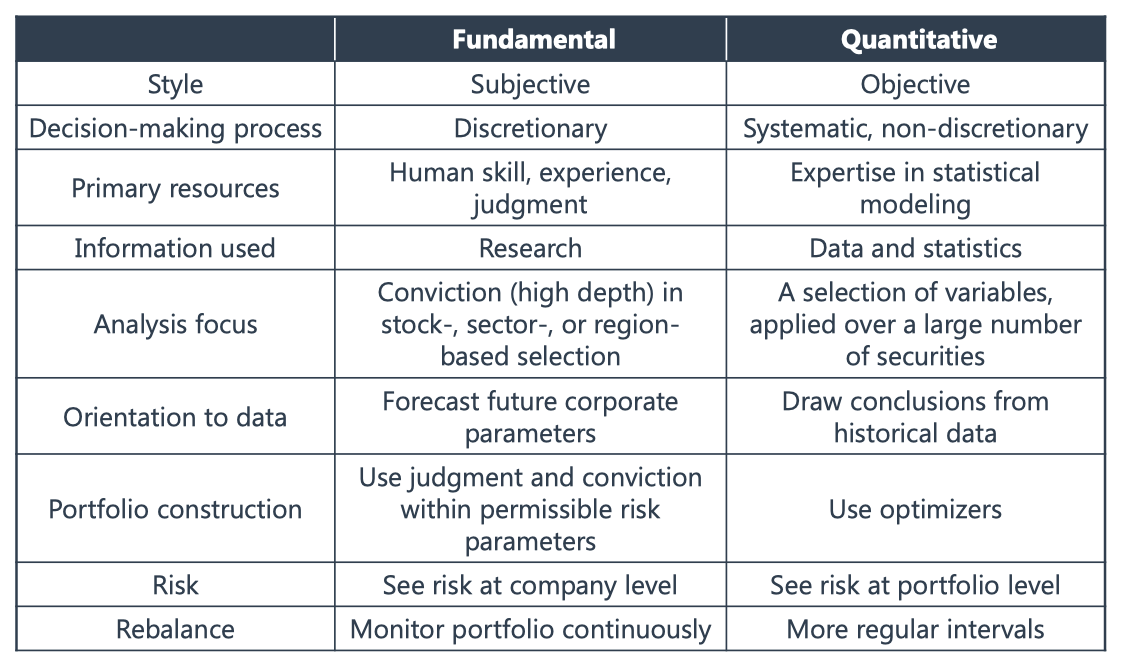

(1) Fundamental Approach (2) Quantitative Approach

Fundamental & Quantitative Approach

Fundamental Approach

Pitfall in Fundamental Investing (more subjective 更主观)

Behavioural Biases

Value Trap 不能只因为 P/B P/E 低就买,它PE低可能是因为 该公司要完蛋了,人们都在卖

Growth Trap 不能因为 expected growth 高就买,可能 expected growth 虽然高,但是可能不达预期,或者 timing 不合时宜

Quantitative Approach

Quantitative Approach (more objective 更加客观,由algorithm确定,但是 model building phase依然要主观判断参与)

Investment Process:

Define the market opportunity

Acquire and Process Data

Back-testing the strategy

Information Coefficient (IC) 用 信息系数,factor 与未来return的相关性。 衡量 factor 怎么样

Pearson IC:

sensitive to outlier 容易受异常值影响,如在算相关系数的时候有一期的数打错了,或者有一期有巨大异常值,那么影响会挺大

Spearman IC 计算相关系数 corr between factor score FS 和 SR 排序值of forward/subsequent return .

计算的是排序值,所以outlier的影响会被减少

P.S. 用 Factor Score @ t 和 Subsequent Month Ration @ t+1 算,因为是Subsequent 所以要 t+1。

Evaluating the Strategy 用 out of sample data去评价,因为 algorithm 会学习已有的数据

Avoid overfitting (overfitting 也叫做 data mining bias )

Portfolio Construction

Model Risks: estimation error

The error of the error term would contribute to the overall risks of model

Periodic Optimisation by algorithm may give different weights, rebalancing create costs

Pitfall in Quantitative Investing

Selection Bias:

Survivorship bias

Look-ahead bias

Overfitting (data-mining bias)

Constraints

Constraints on turnover

Lack of availability of borrowing / shorting

Transaction cost

Quant overcrowding (many quants conduct similar strategy 策略用的多了就失效了)

Comparison

Quantitative model consider correlation between factors, so it consider risks at portfolio level.

Active Strategies

Bottom-up

研究个股的基本面,因为针对个股,所以研究的比较精细,所以一般覆盖的股票比较少

Value-Based Approach 价值型,关注未来的 div 收益

Relative value: 投 low multiple (P/E, P/B) 即price 低的 为 value investment

Contrarian Investing: Purchasing or selling securities against prevailing market sentiment.

High-quality value: Warren Buffet 投 intrinsic value 高的 high quality 龙头

Income Investing: invest high dividend yields or high div growth rate firm

Deep-value investing: focus on low valuation or firms with financial distress 投 multiple 非常低的,面临退市风险的股票,把自己的expert能力发挥,主动参与管理,投资有困难的公司

Restrucuring and Distressed debt investing: invest prior to or during an expected bankruptcy filing 投资distressed firm,相信公司本身的manager有能力管理好

Special Situation: M&A, etc

Growth-Based Approach 成长型 关注未来的 增长

Consistent long-term growth 长期增长

Short-term earning momentum 短期增长

GARP (growth at a reasonable price):

e.g. P/E-to-growth (

Top-Down

从宏观分析到行业

Country / Geography allocation

Industry Sector Rotation

Thematic Investment Strategies: Focus on opportunities presented by new technologies, changes in regulations, and economic cycles.

Volatility-based Strategies: Volatility trading can be conducted through VIX futures, variance swap, option volatility strategy

Factor-Based Strategies

Rewarded Factors: factors have been shown to be positively associated with a long-term return premium, such as size, value, momentum 已经被公认为有效的 factor

Unrewarded Factors: Factors that have not been empirically proven to offer a persistent return premium. 如果基金经理能发现 unrewarded factor 这代表FM的能力

Hedged Portfolio Approach (Fama & French)

Construction Process

Rank stocks by factors

Divide the list into quantiles

Long best quantile short worst quantile

long好的short差的,在long short过程中,大盘的系统性风险被对冲了

Factor Mimicking portfolios (FMP) is a long-short portfolio that is dollar neutral with a pure factor exposure

Track the performance overtime

Drawbacks

Middle quantiles is ignored 所以中间部分的盈利机会被放弃了

Cannot capture non-linear relationship between factors and stocks (as there is only rank, which is linear)

Hedged portfolio is not a pure factor portfolio, as there are many other factors not exposed to a single factor 不是pure factor port

Portfolio is concentrated.

Assume no short limitations

Factor-tilting portfolio

Long only. Will expose to a factor. Controlled level of tracking error 因为只expose to a factor

Factor-Mimicking Portfolio (FMP)

Implement a pure factor portfolio 找只暴露一种risk factor 的stocks

Factor Timing 因子则时

Equity Style Rotation

Activist Strategies 积极的股东主义

持有 < 10%,号召其他小股东以其反对管理层

short-term interest 和 long-term interest。activist追求短期利益,但是管理层追求长期

不受上市公司欢迎,所以用 dual class, staggered board 防止investor做 activist

东西方culture 差异。东方喜欢集权,西方喜欢分立

taking stakes in companies and pushing for companies to make changes that are expected to enhance the value of the activist’s stake. 通过参股,参与公司运营决策,推动公司战略向为股东好的方向走

Target Companies 大原则是经营不太好的公司,这样才有改进的空间

Slower revenue & earning growth 增长慢的

Suffer negative share price momentum

Have weaker-than-average corporate governance

Tactics

Seeking board representation

Writing open letters to management

Proposing changes

Proposing financial restructuring

Reducing extravagant management compensation

Launching legal proceedings

Launching a media campaign

Breaking up a large inefficient conglomerate

Ending

Growth increase

为了提升 ROE ,借钱,发debt,leverage提升

Price 提升,因为empirically activist strategy 确实会带来好的收益

Other Strategies

Statistical Arbitrage: mean-reverting, exploit pricing inefficiency

Market microstructure-based arbitrage strategies (high frequency)

Pairs trading (highly correlated stocks)

Event Driven

M&A

Earnings on Restructuring announcements

Share buybacks, special div, etc

Risks: deal fails, deal duration is long, overestimated

Style Classification 分辨基金经理的投资风格

Holding Based Approach

人工划分 portfolio 中的个体持仓 stock 应该归属于哪个 style ,然后加总看整个portfolio是什么风格

look at the attributes of each individual stock in a portfolio

aggregates these attributes to conclude the overall style of the portfolio.

Morning Star & Thomson Reuters

Net Style Score = Growth Score - Value Score

<0 value, =0 blend, >0 growth

MSCI, FTSE Rusell

Z-score 如 Zscore =0.6 意味着value成分为0.6 growth成分0.4

Return-Based Approach

拿 portfolio return 跟 各种指数回归,判断受那个 style index 影响大

Regress portfolio return On returns of style index

Self-identification FM自己宣称的

根据基金经理 self-described 自己的描述,看是什么style的投资风格

Active Equity Investing

(Systematic + Discretionary) X (Top-down + Bottom-up)

2*2 一共四种管理组合的方式

Targeting low idiosyncratic risk along with low concentrations indicates a systematic approach

Active Return

Overweights outperformed securities 多配好股票

Underweights underperformed securities 少配差股票

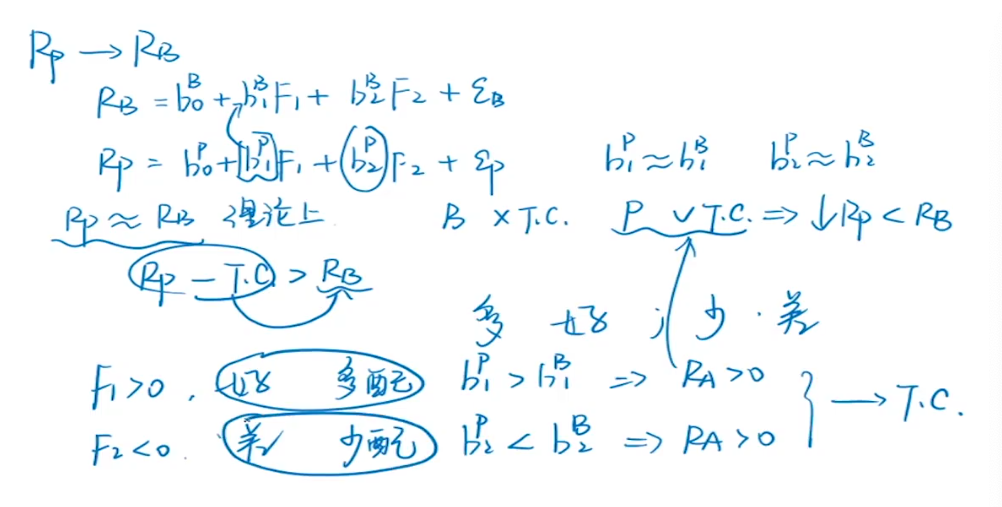

Sources of Active Returns

We all play with factors (not stocks) in this part.

By regression,

(1) for the portfolio:

(2) for the benchmark:

(1) - (2):

The intercepts are approximately equal, so we get the

Finally, the Ex Post Active Returns are

Let

According to the above function, we decompose it into three parts.

Strategically Adjusting, exposure to rewarded risks. Return from factor weighting:

Tactically Adjusting. factor timing, security selection. Return from identifying misplacing, 因为回归的factors 都是 rewarded factor,所以residuals会留下 unrewarded factors。这部分体现了基金经理的的能力 (security selection + CME factor timing),即 Alpha

Sustainable 可持续,取决于基金经理的能力,基金经理越nb alpha越大

Luck and unluck return, Idiosyncratic Return,

Un-sustainable 不可持续,为 Luck

可以根据 diversification程度调整,越diversified 系统性风险越小 epsilon越小

Three Building

Factor Weighting 多配好的,少配差的

Alpha Skills

CME: factor timing 根据宏观经济择时配置 factors (配置 rewarded factors)

Unrewarded Factors (thematic exposure) 选择了不常规用的factors

Sizing Position 权衡购置单一因子的权重 balance confidence in alpha and factors insights

如控制 factor weighting 与 alpha skill 的权重,体现 level of confidence of analytics

A factor-orientated manager 主要从weighting获利的投资者,unexplained part

Systematic manager 不做 factor timing

A stock-picker, with higher confidence 更愿意投资个股,所以

所以discretionary managers are likely to run concentrated portfolio

Breadth of Experience (BR)

Portfolio Construction Approaches

Relative Risks 衡量 active investment的指标

Relative risk is measured w.r.t. the benchmark. There are two measures of the benchmark-relative risks.

Active Share:

要除以 2 因为有主动偏离的部分,需要有其他share 让开匀给 active部分,所以要/2

% of portfolio assets deployed the same as benchmark

即为 一个 portfolio 中,和 benchmark 表现一致的部分

Between (0,1)

Sources 来源:(1) 与 benchmark 中成分股不同 (2) weights 不同。P.S. 如果 portfolio 中 stocks 数比 index 少很多,那么active share一定会大,因为如果数少,则 concentration 集中度大

Active Risks ( Tracking Error )

Source of Risks

Recall:

收益被拆成了 3 部分(或者说 2 部分,即 1 和 2+3,同理 风险也将被拆成 2 部分

与 factor exposure 相关的

和与 个股相关的

high net exposure to a risk factor leads to high active risks 来自beta (risk exposure)差异 提升active risks

neutralised factor exposure will have active risk entirely attributed to active share 如果beta差异(risk exposure) =0 ,那么 active risk 全部来自 active share。因为 alpha & epsilon 即FM主动管理的程度,这个东西可以由 active share 衡量 (注意上面公式,active share 指的是

active risks attributed to active share will be smaller if the number of securtities is large or idiosyncratic risk is small 如果组合中股票数量多,diversification大,

active risk increase with the increse in factor and idiosyncratic volatility

Active Share v.s. Active Risks

The level of active risk will rise with an increase in factor and idiosyncratic volatility

High net exposure to a risk factor will lead to a high level of active risk, irrespective of the level of idiosyncratic risk 即 weights diff 会提升

A portfolio with neutralised factor exposure will have active risk attributed entirely to Active Share. 因为 factor neutral 所以 factor exposure risk 为 0,idiosyncratic risks 贡献了所有的 active risks

If # of stocks 小,那么 concentration 小, active weights 小,所以 active share 小,active risks 也小

Correlation 会影响 active risks 但是不影响 active share

active share 高, active risk不一定高。因为active risk 受 cross correlation影响,越相关,越concentration,risks越大

FM 可以控制 active share ,但是不一定能调整 active risks

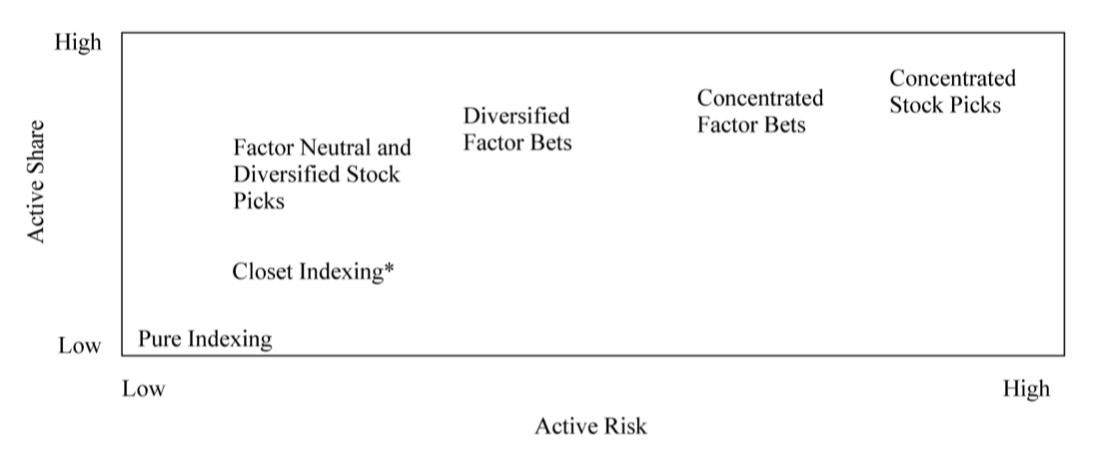

Closet Index: 伪主动管理,说是主动,但实际上是 被动,所以active risk & active share 都低

Factor Neutral:

Factor Bets: active risks is high。active risks 等式的第一部分不等于零,第二部分较小。较为贴合benchmark 的 factors

Concentrated: active share is high,factor exposure 比较高

Concentrated Stock Pick: 全高

Risk Budgeting

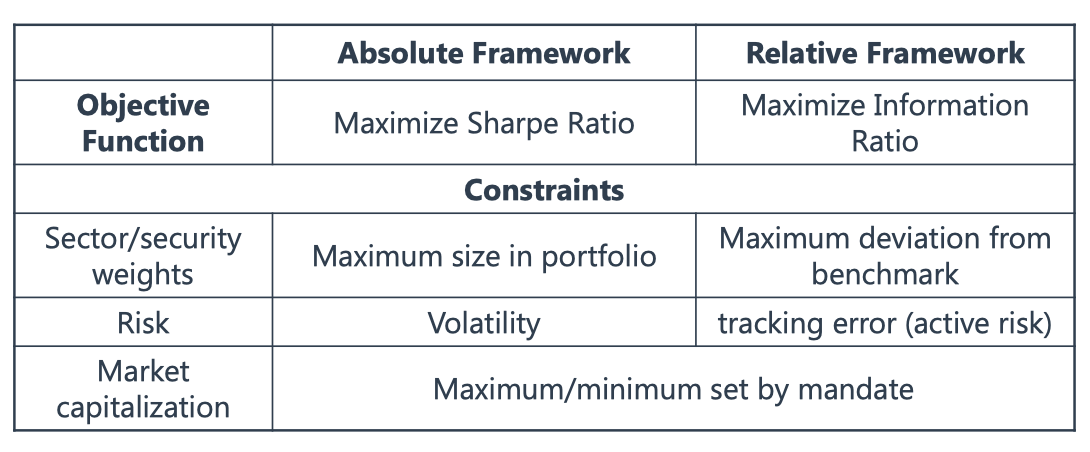

Absolute and Relative Risks

Absolute Risk Measure: express in terms of total return

Sources of Absolute Risks

for Asset 1:

for Asset 2:

Contribution of each asset to total

For a Portfolio in regression model

Relative Risk Measure: relative to the benchmark 所有指标都减去benchmark 获得 active risk or active return 这才是relative term

Derivatives

Allocating the Risk Budget

For Cash, it naturally has no total risks. However, if there are more cash in the portfolio, the portfolio would definitely deviate from the bechmark (and there are low corr ). Then there would be active risks 如果组合中有 cash,那么组合一定会与benchmark偏离,即带来 active risks

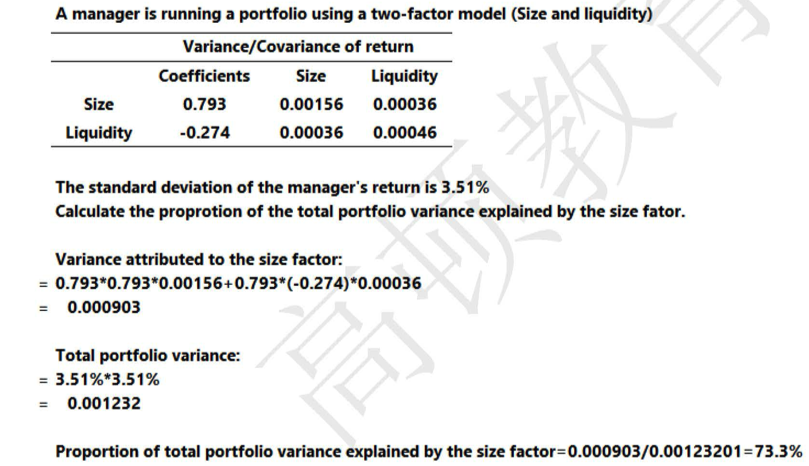

Active Portfolio Variance can be segmented into two parts:

Variance Explained by factor exposures

Unexplained (

Risk Constraints

由于很多 securities 不符合正态分布,或者其他原因,所以用以下三个补充方法

Heuristic Risk Constraint

Liquidity Constraint

Allocation Constraint

Index Weight Constraint

Formal Risk Constraint

VaR (Conditional VaR, Incremental VaR, Marginal VaR, etc)

Drawdown

P.S. the distinction between formal and heuristic risks

Other Considerations:

Leverage

Risk Measures

Implicit Cost

Delay Cost

Ask-Bid Spread

Market Impacts Cost

由于买卖时推高或者拉低price Slippage Cost 带来的价格变化,而产生的成本

Slippage Cost = Market Impact Cost + Delay Cost

Factors affects the market impact cost

AUM v.s. Market Cap (交易规模越大,价格会被推的越高

Higher Portfolio Turnover and shorter invetment horizon (交易越频繁,cost越多

the tading signal is informative to the mkt

Delay Cost 由于订单分散在多期买,delay时间带来交易的股价与预期的股价不一样了,叫delay cost

Four Conclusion about slippage cost

slippage cost is more important than commission ocst

greater for small cap stock than large cap stock

no necessarily greater in emerging mkt

slippage cost is higher if market volatility is higher

Strategy

Long-only Investment

Long term risk premium 历史看 涨多跌少

Capacity and Scalability 一般 买股票的 liquidity 比short大的好

Limited Lagal Liability Laws 损失是limited,不同于short方 损失时无限的

市场一般会谴责 short, 而 long 是美德

Long/short Investing

Gross Exposure = Long Position + Short Position

Net Exposure = Long Position - Short Position

if net exposure < 0 , net short exposure

i.e.

130/30 funds 为long 130,short 30

market neutral portfolio, 为 remove market exposure 多空net = 0, beta = 0 如 long 50 short 50

Benefits of Long/Short Strategies

Express negative ideas

use leverage

remove mkt risks

control exposure to risk factors

Drawbacks

Complex

Costs are higher coz there need more management

not personal ideology

leverage might be unacceptable

might have losses on the short position, short squeeze 由于price increase 导致保证金需要补充

Pitfall

Behavioural Bias

Confirmation Bias: 疑邻窃斧, stock love

Illusion of Control: Excess Trading, Concentrated

Availability: Reduce the Opportunity Set

Loss Aversion: 卖的早gain的stock,不舍得卖loss股 disposition effects,导致 unbalanced account 持仓都是亏钱的

Overconfidence Bias: overestimate return, underestimate risks

Regret Aversion Bias: 持仓过度 long-term

Value and Growth Trap

低PE 和 低PEG 的股票 长期不动,不涨价(如果PE低于行业均值,但是growth负的,说明他活该PE低,要倒闭)

Well Constructed Portfolio

weights 能清晰的 体现 investment philosophy

Factor Risk Contribution 中 unexplained 部分少。unexplained 越多表示 FM 自己都不能解释自己 fund risks

组合中 number 越多,按理说 越 diversified。此时 如果 number多的 portfolio 的 active risk 大,那么管理的不有效。

Number 和 active risks 不能 contradict

Fee / Active Share 越小,说明 fee 越便宜

Sample Text

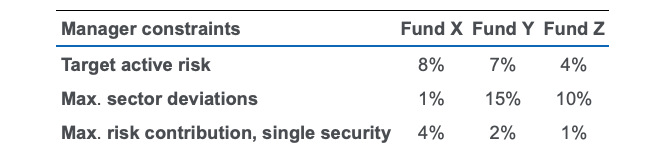

The risk targets for Fund Z are most likely those of a manager using a diversified multi-factor approach. Low single-security risk of 1% and modest overall portfolio risk of 4%, combined with flexibility on sector risk, demonstrate a highly diversified portfolio that primarily emphasizes factor exposures. Fund X has risk targets consistent with an emphasis on stock picking—namely, high active risk, high exposure to risk from a single security, and low sector deviations. Fund Y has risk targets consistent with an emphasis on sector rotation—namely, high active risk and a high tolerance for sector deviations.

Active Share: differ from the benchmark

Active Risks: concentration or diversification

Style/Sector Deviation: style / sector rotation would have high deviation

Stock Picking: high active share (pick so high active share and high concentration)

diversified stock picking: high active share (pick so high active share, diversified so low active risks),

style rotation: high active risks (concentrated)