Asset Allocation

Economic Balance Sheet

Definition: includes (1) conventional assets and liabilities (in Accounting Statement) and (2) extended portfolio assets and liabilities (not appear in conventional B/S).

Extended Portfolio Assets includes:

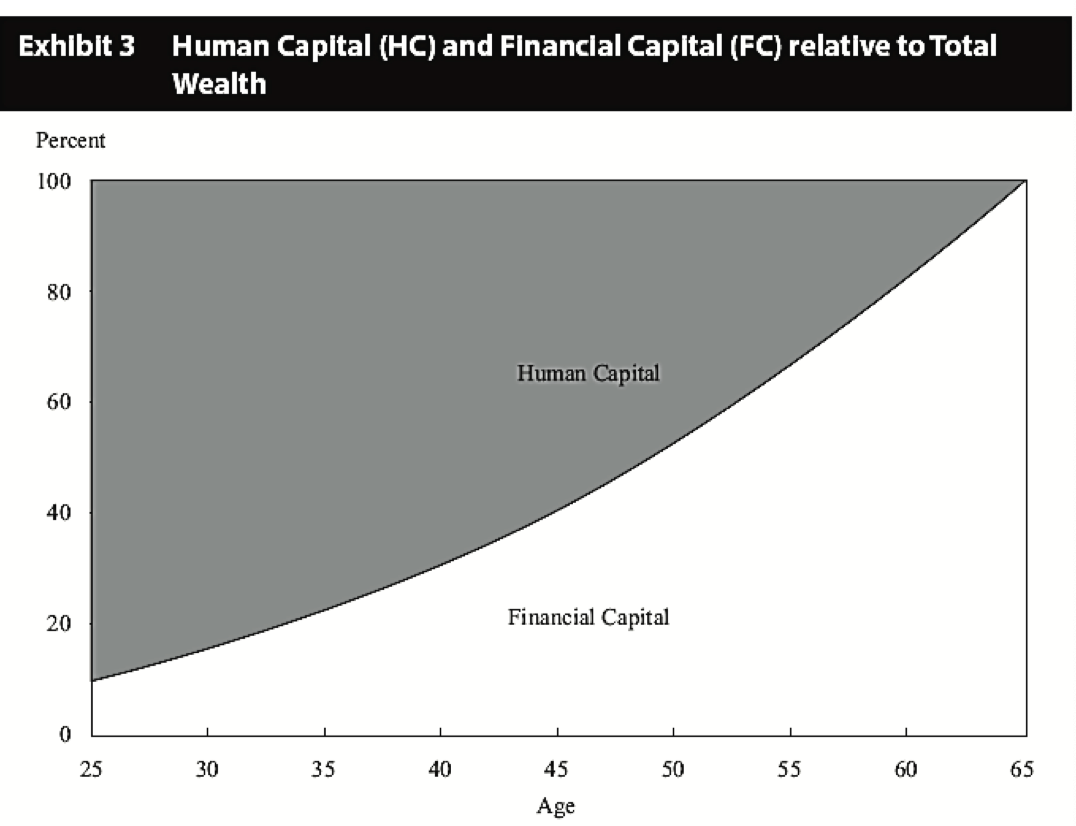

Human Capital (PV of Future Earnings),

PV of Pension Income (Un-vested Benefits),

P.S.

PV of Expected Inheritances (Bequest).

Above is for individual investors, and before is for institutional investors.

Underground Mineral Resources

PV of Future Intellectual Property Royalties

Extended Portfolio Liabilities include:

PV of Future Consumption.

Economic Net Worth = Net Worth (Financial Asset - Fin Lia) + 1,2,3

| Asset | Lia and Net Worth |

|---|---|

| Financial Assets | Financial Liabilities |

| Extended Assets: PV of Expected Contribution | Extended Liabilities: PV of Expected Future Support |

| Net Worth |

Asset Allocation Approach

Asset Only - MVO

Liability-Relative - fund a lia

Goals-Based - address goal

| Asset Allocation Approach | Relation to Economic Balance Sheet | Typical Objective | Typical Uses and Asset Owner Types | Risk Objectives |

|---|---|---|---|---|

| Asset only | Does not explicitly model liabilities or goals | Maximise Sharpe ratio for acceptable level of volatility | Liabilities or goals not defined and/or simplicity is importantSome foundations, endowmentsSovereign wealth fundsIndividual investors | augmented by Monte Carlo simulation, which can provide tail risks. |

| Liability relative | Models legal and quasi-liabilities | Fund liabilities and invest excess assets for growth | Penalty for not meeting liabilities highBanksDefined benefit pensionsInsurers | focus on the risk of having insufficient assets to pay obligations when due |

| Goals based | Models goals | Achieve goals with specified required probabilities of success | Individual investors | concerned with the risk of failing to achieve goals |

Asset Classification Rationale

Homogenous. Assets in the same class have similar attributes.

Mutually Exclusive. Not Overlapping.

Diversifying. Not highly expected correlated with other classes.

Preponderance of world investable wealth. Increase Expected Return for a given level of risks.

Asset classes selected for investment should have the capacity to absorb a meaningful proportion of an investor’s portfolio.

Asset classes often include:

Global public equity

Global private equity: VC, LBO

Global fixed income

Real assets: includes assets that provide sensitivity to inflation, such as private real estate equity, private infrastructure, and commodities. Sometimes, global inflation-linked bonds are included as a real asset rather than fixed income because of their sensitivity to inflation.

( Inflation-Linked Bonds are a proxy for REAL interest rate, because inflation linked bonds' prices vary with inflation so if you remove the effect of inflation, you should end up with the real rate.

Strategic Asset Allocation

An allocation between the portfolio and risk-free asset.

F.O.C. w.r.t.

Two Dimensions

Passive Management: does not react to changes in the investor’s CME or insights into individual investments;

Active Management will respond to changing CME

Tactical Asset Allocation (TAA) and Dynamic Asset Allocation (DAA)

TAA involves deliberate short-term deviations from the SAA; 短期 deviate from SAA

DAA incorporates deviations from the SAA that are motivated by longer-term valuation signals or economic views. 长期 deviate from SAA

Rebalancing - make portfolio close to SAA

Two Approaches:

Calendar Rebalancing: on a certain period basis

Percent-Range Rebalance (or Corridor)

Factors affecting the Optimal Corridor Level

Transaction Cost: high costs, high hurdle for rebalancing, high corridor. Positive

Risk Tolerance: high tolerance, less sensitive to divergences from SAA, high corridor. Positive

Risk Aversion. Negative

Asset Class Correlation: highly correlated, high corridor. Positive

Belief in Momentum: has momentum, high corridor. Positive

Liquidity: Less liquidity, higher cost, high corridor. Negative

Volatility: Positive or Negative:

Negative because The higher the volatility of the rest of the portfolio, excluding the asset class being considered, the more likely a large divergence from the strategic asset allocation becomes, which should point to a narrower optimal corridor, all else being equal.

Positive because higher vol, more transaction cost

Rebalance Frequency

The narrower the corridor, the more frequent to rebalance

More frequent monitor, the greater the precision

More frequent rebalance, more cost

Rebalance earns return, and the returns are generated from being short volatility

In the case of a portfolio consisting of a risky asset and a risk-free asset, the return to a rebalanced portfolio can be replicated by creating a buy-and-hold position in the portfolio, writing out-of the-money puts and calls on the risky asset, and investing the premiums in risk-free bonds.

As the value of puts and calls is positively related to volatility, such a position is called being short volatility

Principal of Asset Allocation

Asset-Only: MVO

Characteristics: (1) sensitive to inputs 因为optimisation process makes that (2) might concentrate to certain class 会集中于某个asset class,而不是 disperse

0.005 is bull shit for balancing the decimal, if the input ignore %. Use

0.005 = 1/2 /100 为了平衡 sigma^2 的量纲,输入时直接拿掉%才这么算,SB才这么算。

带小数点做input,直接用正常公式就行,不用0.005

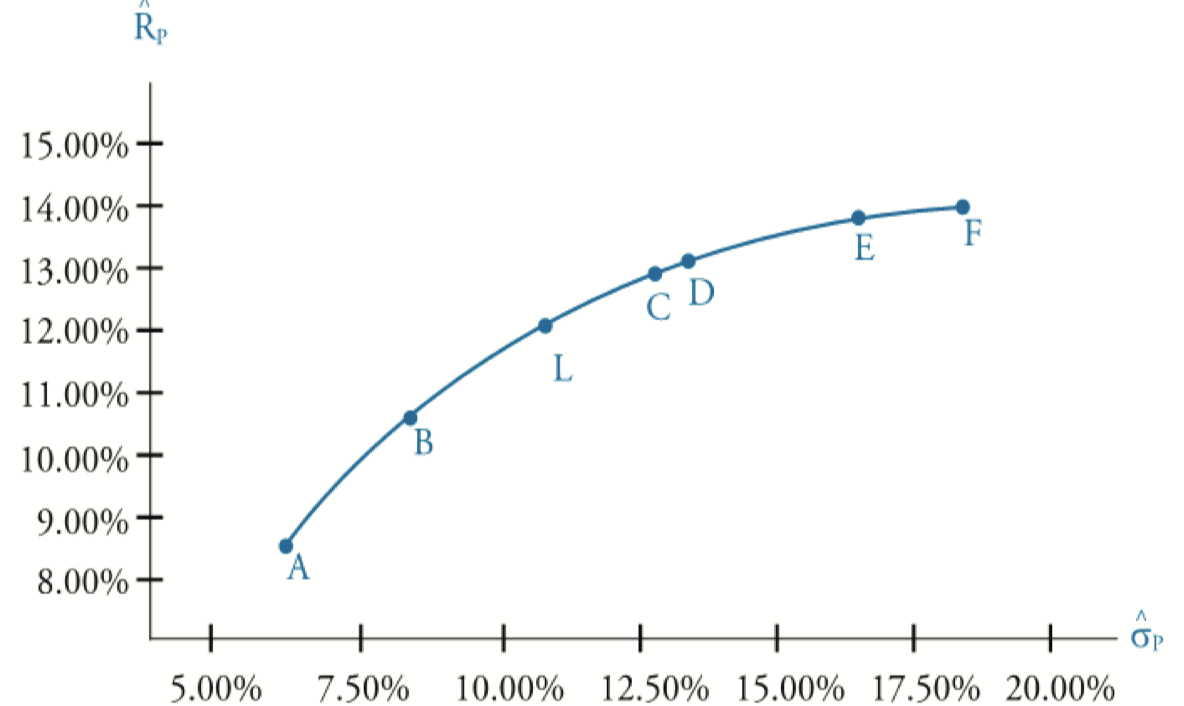

if the non-negative constraint is made, then there are points on the efficients frontier becoming unavailable. The efficient frontier becomes non-continuous. To approximate the standard deviation of those points, we use adjacent corner portfolios. 如果点在non-continuous的地方,用两边的adjacent点拟合

Reasoning:

the adjacent corner portfolios (use D, L to approximate C) give more accurate results, than far away portfolios (A,F to approx C). 越近的点拟合越好

one of the adjacent portfolio has the high Sharpe ratio. The adjacent portfolios would artificially have a max Sharpe one

assume the adjacent portfolios have correlation of 1. Then the variance of approximation is

If there is a risk-free asset, then combine the risk-free asset with the tangent portfolio.

Pros and Cons of MVO

Pros: commonly, widely, easily, used

Cons:

The optimisation process make output highly sensitive to inputs (see 2)

Outputs are highly concentrated 结果weights集中在某个资产上 (1. apply constraints, 2. Resample, 3. Reverse Optimisation, 4. Black-Litterrman)

MVO assume standard normal dist, so not account for Skewness and Kurtosis (use other dist instead)

sources of risks may not be diversified (use factor-based model)

no consider liability or consumption stream (use ALM, Surplus MVO)

MVO is a single-period framework that not consider trading / rebalance cost and tax (use MCS instead)

Overcome those Cons

Constraints

incorporate real-world constraints, can restrict percentage of asset class.

Non-negative constraint, percentage constraint, upper limits

However, if constraint is made, the problem is no longer optimisation of the original. 不再是原来的 Optimisation, 而是 optimisation with constraints.

Resample

Resampling uses MCS to estimate a large number of potential capital market assumptions, simulated frontiers are saved and averaged to get the resampled frontier.

As multi paths are simulated, the resampled frontier would be smoothed not in-continuous.

However, there might be

concave bump where expected return decreases as expected risk increases

Risky asset allocations are over-diversified. (as there are simulations)

inherit estimation errors. (有estimate by Monte Carlo 就有estimation errors)

Lack of theoretical foundation.

Reverse Optimisation

to cope with the problem that the expected return of expected return and standard deviation are not reliable. We use:

Way 1:

Allocation Weights of Global Market Portfolio (Mkt Cap %)

Input: Implied Return

Way 2: Reverse Beta

use the weights of asset class (or index) to form a working version of the global market portfolio;

use the beta of each asset relative to the global market portfolio.

use CAPM to infer expected return

run a MVO

Black-Litterman Model

view adjusted

Like a weights average of

如果没有view,则为 implied return 即与 reverse opt结果相同

Non-normal Optimisation

As normal dist has only two parameter, mean and variance, the first and second moment, it do not account for further moments, such as

Skewness - the asymmetric ~ity

Kurtosis - the thickness of tail

Other optimisation could be use to account for the non-normal return dist characteristics: (1) mean-semivariance opt, (2) mean-condition VaR opt (3) mean-variance-skewness opt; (4) mean-var-skew-kurt opt. etc

Factor-Based Model

use investment factors.

requires three sets of inputs: returns, risks (s.d.), correlations

Pair-wise correlations with the market and with one another are generally low. Constructing factors in this manner removes most market exposure from the factors because of the short positions that offset long positions

Monte Carlo Simulation MCS

MCS is the complements of the MVO. MVO can only do with single-period. However, MCS can grapple with a range of practical issues:

path dependence, and

taxes triggered by rebalance.

Liquidity Consideration

Liquid Asset Classes: publicly listed equity and bond

Less Liquid: direct real estate, infrastructure, and PE

To solve the illiquid problem, practical options include

exclude less liquid asset classes

model input by representing the highly diversified characteristics. such as use REITs instead of direct real estate.

?? Include less liquid asset classes in the asset allocation decision and attempt to model the inputs to represent the specific risk characteristics associated with the likely implementation vehicles.

Liability-relative Asset Allocations 基本上只要涉及Lia 或者考虑过 lia 的就都要用 Lia-relative AA

The asset allocation with considering the investor's Liability.

Surplus Optimisation / Surplus MVO

We consider the Surplus.

The objective function becomes the follow, where we use the surplus expected return and surplus variance instead.

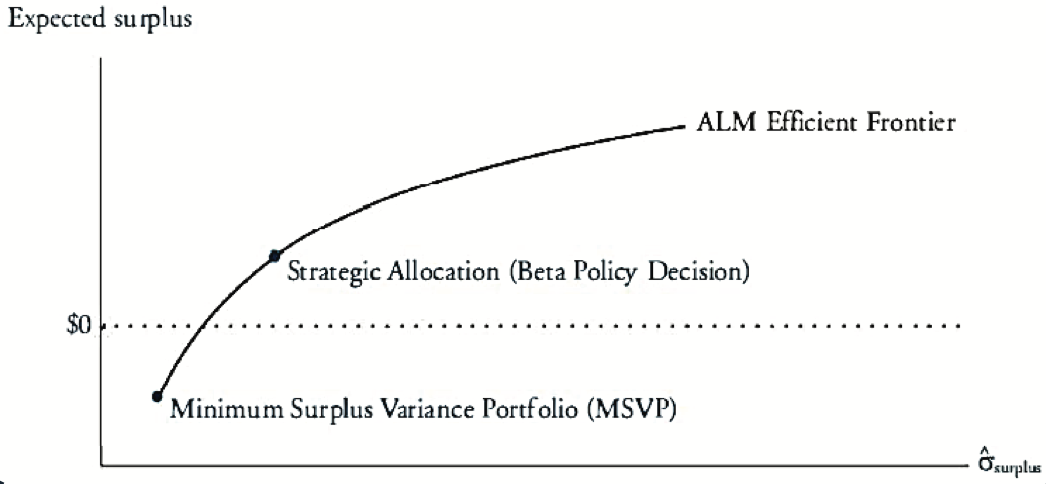

ALM Efficient Frontier

Asset Liability Management (ALM) approach minimise the difference between assets and liabilities at each level of risks

Difference between Surplus & Asset-only

Expected Surplus & Variance of Surplus

ALM Efficient Frontier & Efficient Frontier

Minimum Surplus Variance Portfolio & Global Minimum Variance Portfolio

The Minimum Surplus Variance Portfolio might be negative

ALM MVO - minimise surplus variance & AO MVO - minimise portfolio variance.

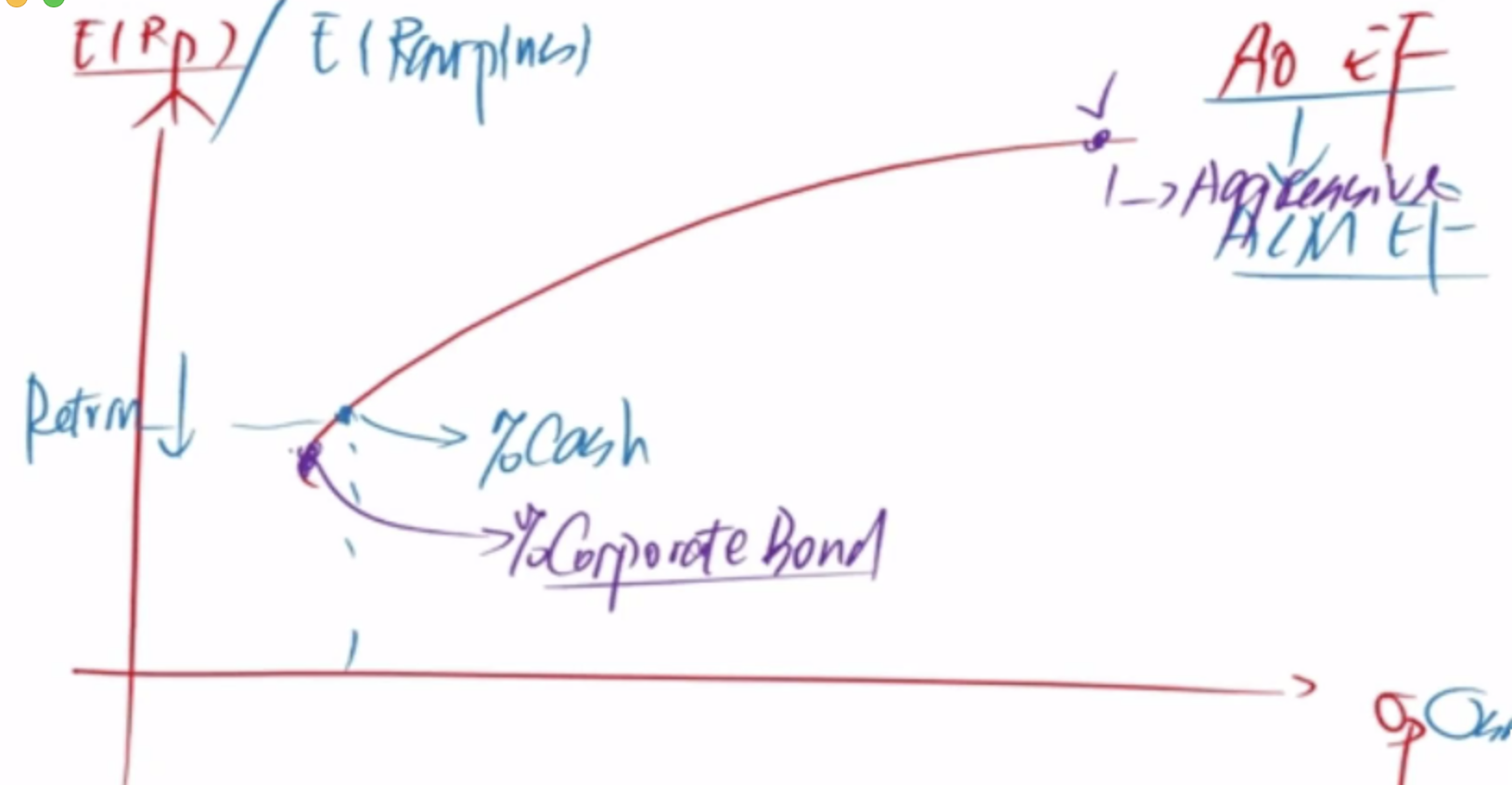

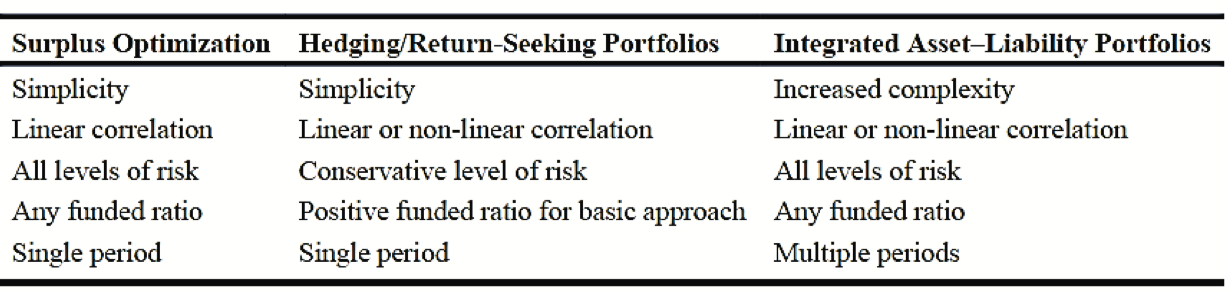

Comparison

The most conservative mix of Surplus Efficient Frontier consists mostly of US corporate bond 因为要考虑 -L,需要正收益的资产对冲。而the most conservative mix of Asset only is Cash

当risk 提升时,Surplus & Asset-only have identical aggressive portfolio (PE), 两者一样当aggressive时

当expected surplus提升到一定程度时,持有的bond将disappear,因为return不足以

Hedging / Return-seeking Portfolio Approach ( Two-portfolio Approach )

Basic: A > L (hedge fully, or called True Hedge)

Two portfolio, with one that includes riskless bonds that will pay off the fixed obligation in 10 years and the other a risky portfolio that earns a competitive risk-adjusted return. This approach is a simple two-step process of hedging the fixed obligation and then investing the balance of the assets in a return-seeking portfolio.

The Liability-relative Asset Allocation task is divided into two parts (1) hedging portfolio, (2) return-seeking portfolio.

Hedging Portfolio is used to hedge fully Liability

Return-Seeking Portfolio can be managed independently of the hedging portfolio (e.g. using MVO).

Variant: A < L (hedge partially) - Aggressive or less conservative

Not fully hedge the Liability. Partially hedge the liability, and use the other to do AO-MVO

Variant of Variant: An Alternative

use Asset to purchase derivative and use derivative to hedge the change of liability

Difference between Hedging/Return-seeking (two portfolio) and Surplus Opt

Surplus Optimization is a holistic approach focusing on the surplus of assets over liabilities, integrating the risks and returns of both.

In contrast, the Hedging/Return-Seeking approach separates the portfolio into two parts, each with a distinct focus: one to hedge against liabilities and the other to seek additional returns.

Integrated Asset-Liability Approach

把 A & L 一起考虑。由于 Two Portfolio 适合用于 Over-funded pension,因为可以把大于 L 的部分拆开。

Integratred Asset Lia Approach 可以应用于任何 A > < = L 的情况

逻辑倒序,但对于 Under-funded Pension 就应该用 Integrated AL Approach 。对于deficit pension plan 要 A L 一起考虑

Integrate or jointly optimise asset and liability decision

Has to potential to improve the institution's surplus

Can be implemented in a factor-based model

因为Asset和Lia一起考虑,所以decision可能更加 紧密,也因此有可能 improve institution's surplus

可以考虑 multi-period 可以多期,与其他不同

Comparison

Surplus Optimisation & Two Portfolio

Surplus Optimisation approach links assets and the present value of liabilities through a correlation coefficient. 用Correlation算Surplus Efficient Frontier, 而 Two-portfolio Approch不需要

Two Portfolio (Basic) needs over-funded, (Variant) need not. 而Surplus Optimisation method 不考虑overfunded or not

与 lia一起考虑,即为非线性

Goals-Based Asset Allocation

Apply best to Individuals

Allocate capital to sub-portfolio, pick the highest probability, use horizon-adjusted discount rate to discount the expected CF, obtain lowest initially required capital for each goal

Drawback of Goal Based: (1) inefficient, (2) not consider correlation between asset class

Heuristic and Other Approaches

120 - age

60 / 40 stock/bond (Noway Sovereign Fund)

Endowment Model (Yale Model)

High allocation to non-tradition assets (alternatives)

Seek to earn illiquidty premium

Commitment to active management

long time horizon

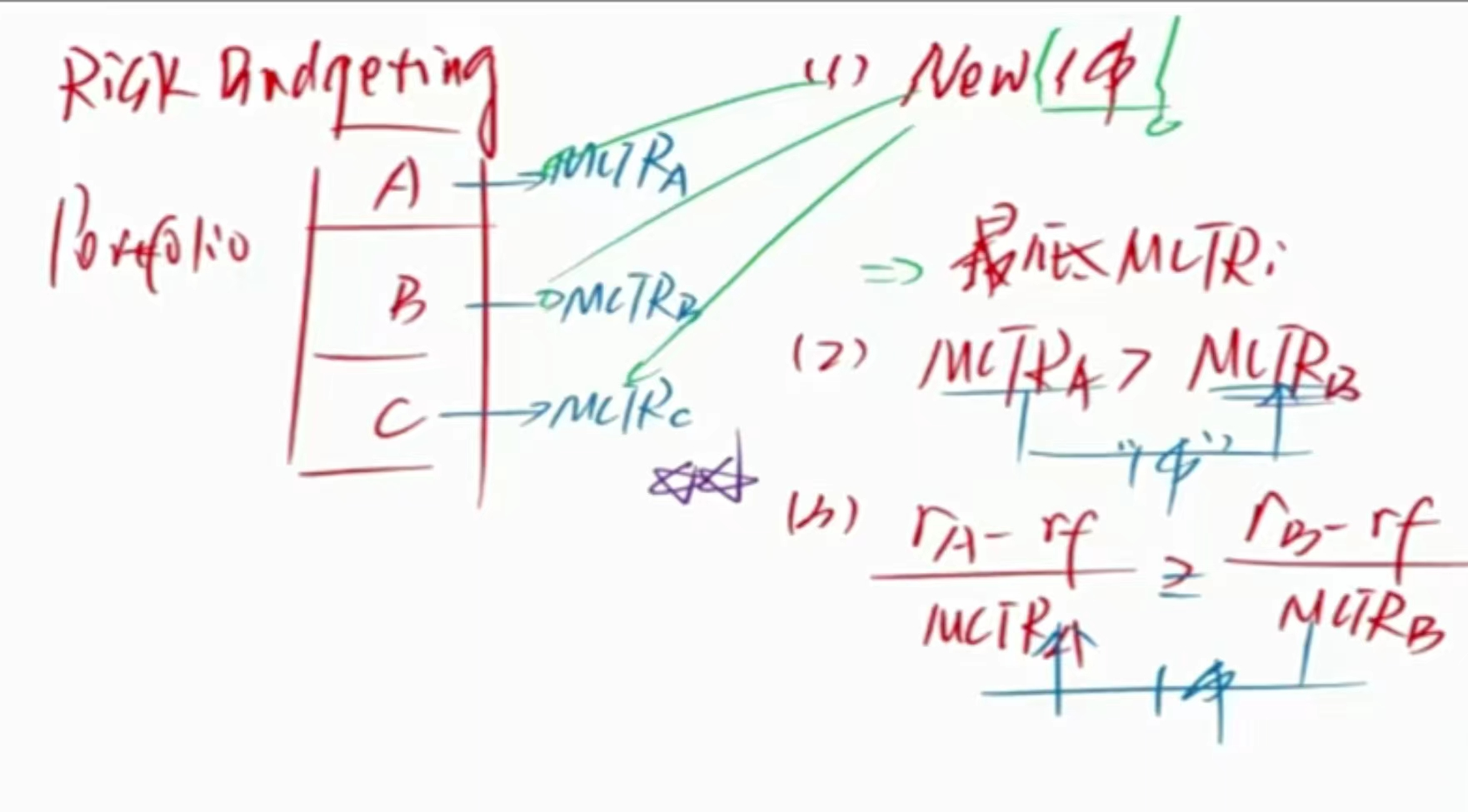

Risk Budgeting and Risk Parity

Risk Budgeting

The goal of risk budgeting is to maximise return per unit of risk. A risk budget identifies the total amount of risk and attributes risk to its constituent parts. An optimum risk budget allocates risk efficiently.

MCTR Goal: maximise the return per unit of risk 每承担一单位风险获得的收益

投资 MCTR 最低的 portfolio

MCTR, Marginal Contribution to Total Risks

As,

Thus,

Ratio of Excess Return to MCTR =

ACTR, Absolute Contribution to Total Risks, how much it contributes to portfolio return volatility.

multiply

Risk Parity

每个资产给组合的风险贡献

Each asset (asset class or risk factor) should contribute equally to the total risk of the portfolio for a portfolio to be well diversified. 每个asset class贡献同样的资产,那么比如有 bond, equity, commodity, 因为bond的风险小,那么portfolio中配置的就bond就更多,这样可以达到1/3 portfolio total risk

Pros and Cons

Pros: risks are diversified

Cons: as we include more bonds by the risk parity, risks are diversified, but expected returns are scarified.

Cons: Dependent on the ability to use extremely large amounts of leverage at low borrow rates

Real-World Constraint

Assets Size

Large Asst: (1) illiquidity, (2) make small-cap stock price wildly fluctuate, (3) reluctant organisational hierarchies.

Liquidity

Life-Insurance has long time horizon, so less liquidity demand. Bank has higher liquidity demand.

Taxable Investors

The correlation between assets are not affected by tax rate

Rebalance Corridor

tax 大

因为 after tax range 大,所以 除以 1-t

Tax-Deferred Account (TDA)

Deal with Behavioural Bias

Identify Anomalies

Loss-aversion bias: Goal Based

Illusion of Control (cognitive bias): global portfolio performance

Mental Accounting: Goal Based

Representative / Recency(representative problem 的三个层次:(1)过去好的投资,将来也是好的;(2)好公司就是好的投资;(3)只看了短期收益就认为是好的基金经理): Governance

Framing Bias: 多角度看。看return同时看risk,Sharpe ratio, max drawdown等

Availability Bias (买的是最先想到的股票): global portfolio

Pension Funds

影响 pension fund 的因素

Average Participant Age 越高,离把pension折现提出的时间越短,折现的越少,则 lia 越大

Salary Growth 收入越多,Fund Lia越大 commitment

Short term rate increase,Pension Fund 大多数是长周期,不是short term,