Institutional Investors

Types

Pension Plan (35 tn USD)

Sovereign Wealth Funds (7 tn USD)

University Endowments and Private Foundations (1.6 tn USD)

Banks and Insurers (9 tn USD)

Common Characteristics

Scale (Asset Size)

Small institutional investor小的机构,outsource外包给别的人做投资。<500 millions,

small number of analysts,

not do in-sourcing alternative investments as they need people.

might not be able to invest in PE fund

Larger institutional investor 大的机构

experience scale benefits,

get access to a large universe of assets

cons: s.t. market price impact

large size can get access to PE fund, 资金规模小的 PE 投不了

Long-term Investment Horizon 相对于 individual 投资期限更长 & Low Liquidity Needs 不太容易被提款

Banks and insurance companies however tend to be more asset-liability focused

周期长可以投 private real estate & alternatives

Governance Framework

board of directors -> investment committee (CIO) -> investors

制定 risk appetite, set investment strategy

Regulatory Frameworks 为了 lower leverage, increase centralised clearing, improve reporting transparency

Principal-Agent Issues 由于组织架构,所以会面临 board 和 investor的分歧

Overview of IPS

stakeholders

Liabilities and Investment Horizon

Liquidity Needs

External Constraints affecting Investment

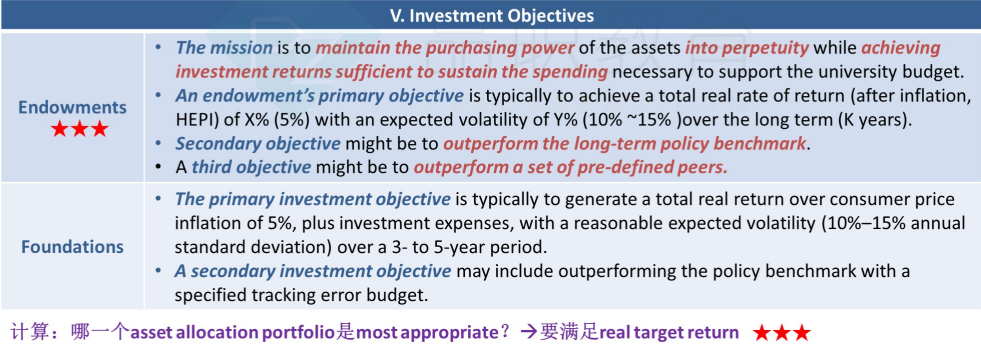

Investment Objectives

Asset Allocation

(Risk Consideration, for Pension Plan)

Investment Approaches

Scales matters:

for the small scale, funds may use the endowment model, however, might be unable to access to the PE funds that require minimum liquidity needs.

for the large scale, funds can get access a large universe of assets, however might easily get exposed to market price index, hard to invest in small cap stock, etc.

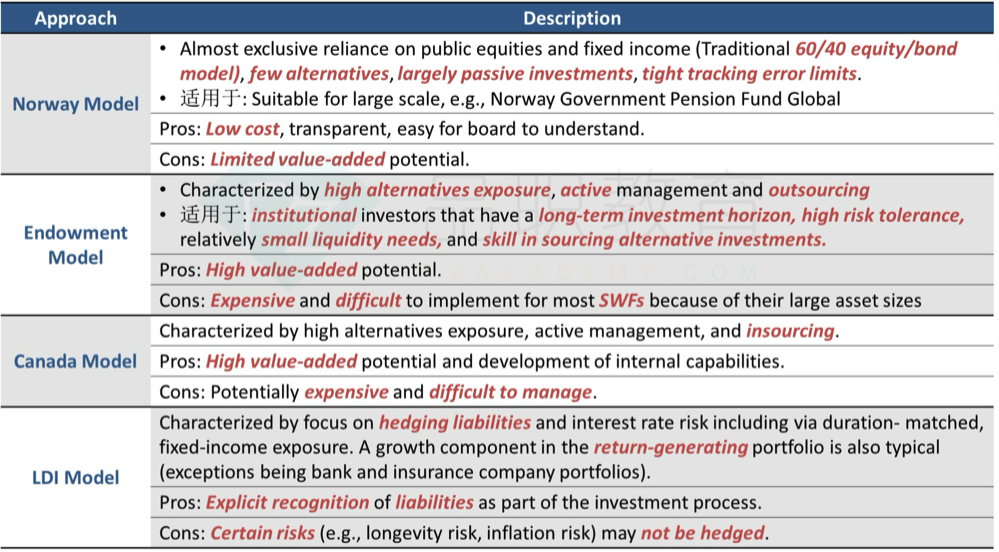

Norway Model (Sovereign Wealth Funds)

因为是养老金,所以保守

Traditional Style characterised by 60%/40% equity/fixed income. Few Alternatives, Large Passive Investment, tight tracking error limits

Pros: low cost, high transparency, suitable for large scale

Cons: limited valued-added potential 因为主要是 passive

Endowment Model (university endowment, SWF, DB) 原为Yale基金

激进,外包

High alternative exposure, active management and outsourcing

Pros: high value-added potential

Cons: high fess and high cost

Canada Model

激进,自己管in-hourse,internally managed。加拿大的养老金,但是也很active。

High alternative Exposure, active management, internally managed (不同于 Yale外包,Canada都自己管in-house)

20% 投 reference part,如Norway的60/40 benchmark

剩下80%,

加入 active + alternative,使risks提升return提升

降低上市股%,提升PE%。两者exposure一致,但是return提升

Pros: High value-added potential and development of internal capabilities.

Cons: Potentially expensive and difficult to manage.

Liability Driven Investment, LDI model (banks & insurers) 因为为DB用和银行用,所以比较保守,考虑资产如何覆盖负债

focus on hedging liabilities and interest rate risk

Pros: Explicit recognition of liabilities as part of the investment process.

Cons: Certain risks (e.g., longevity risk, inflation risk) may not be hedged.

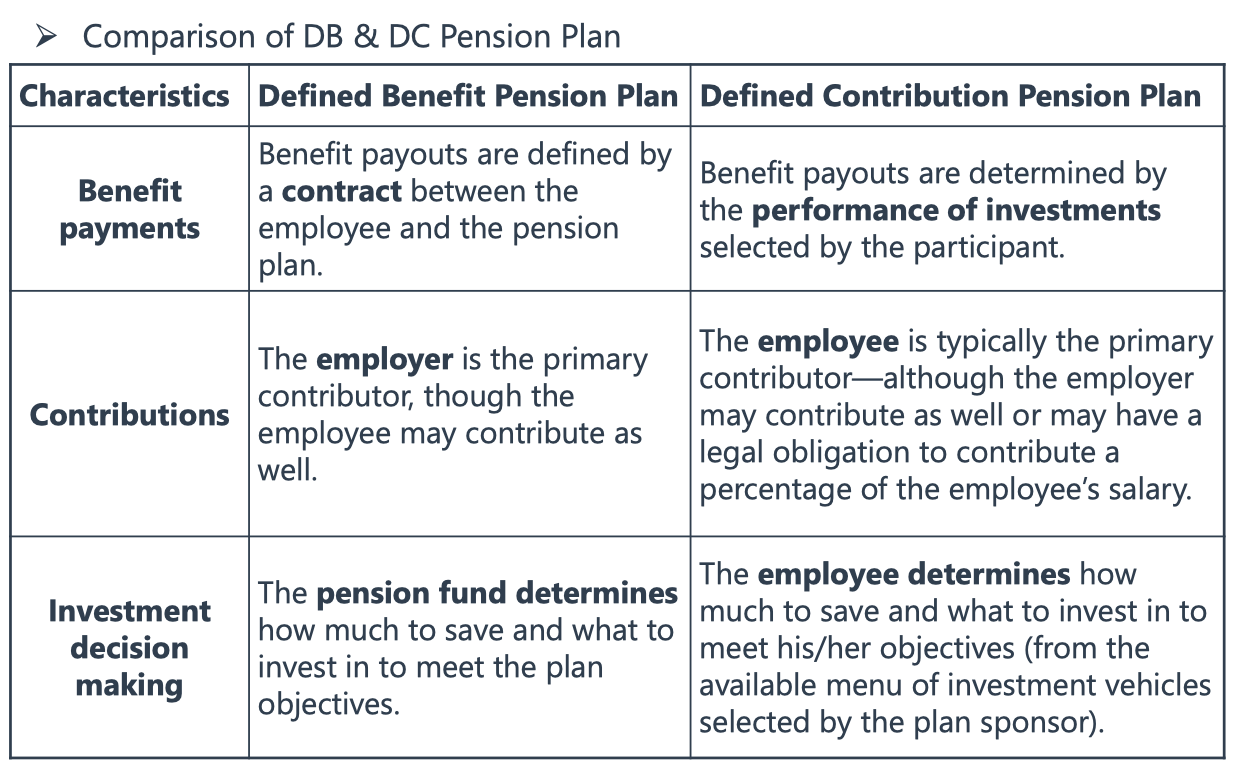

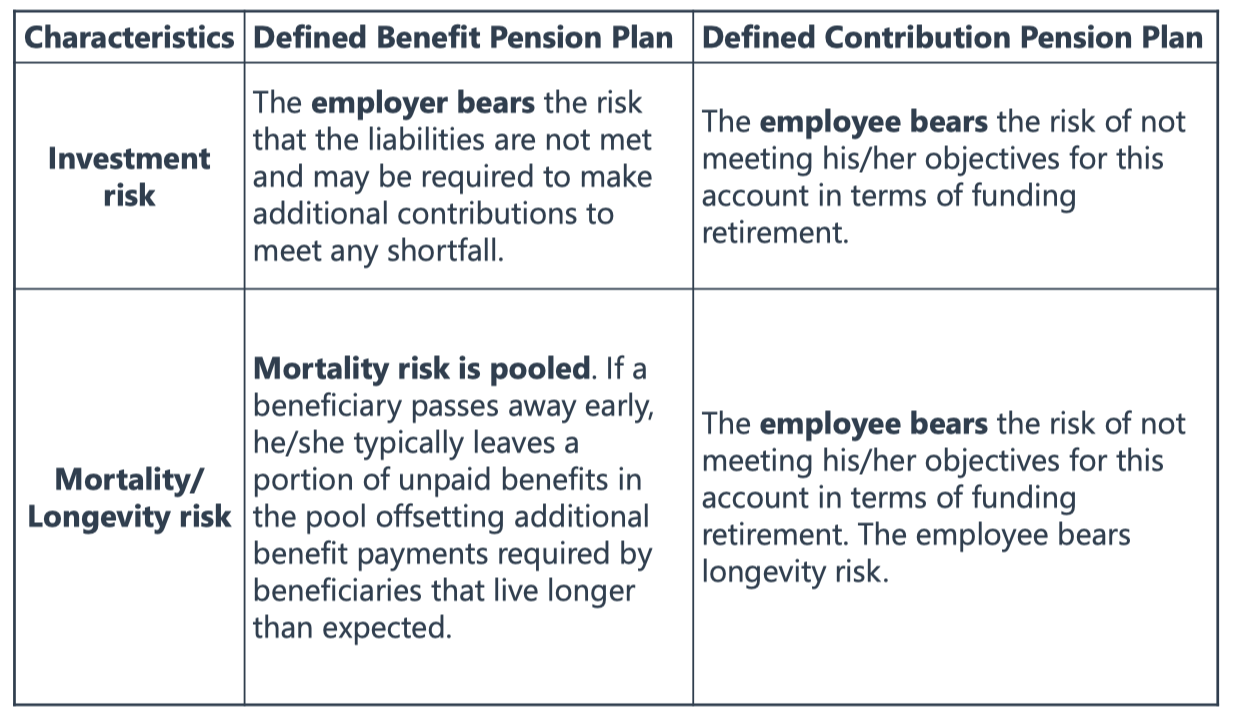

Pension Funds

DB Plan 由 employer承担风险,所以相对于 institutional investment

DC Plan 由 员工 承担风险,所以相对于 individual investment

DB Plan

如果 DB pension fund is not fully funded, then have risks

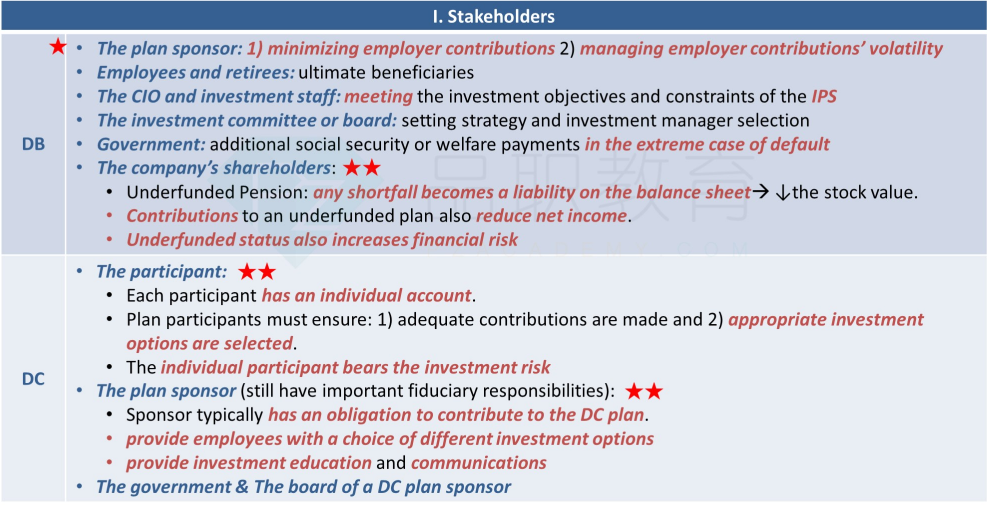

Stakeholders 利益相关方

Plan sponsors (employers)

Plan beneficiary (employees and retirees)

Investment staff & investment committee

Government (1)设置税收优惠,鼓励investor把钱存入 pension plan。(2)政府为养老金兜底,如果pension plan毁约

Funded Status = FVA - PBO

正,表示net asset;负,表示net lia

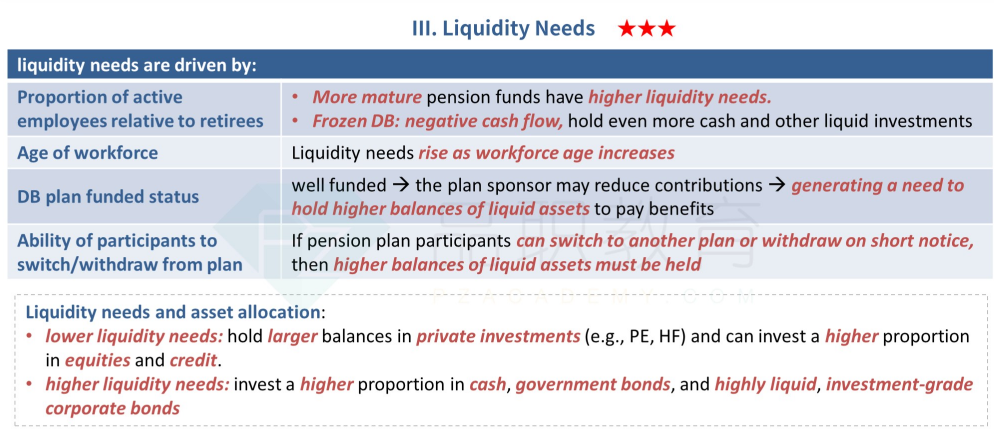

影响 Liquidity needs 的因素

proportion of retired lives in the plan

Frozen plans

Workforce of the employer is older

Funded status 如果 fund status 为正,相当于 A > L,倾向于提出钱来,liquidity needs大

Ability to switch or withdraw

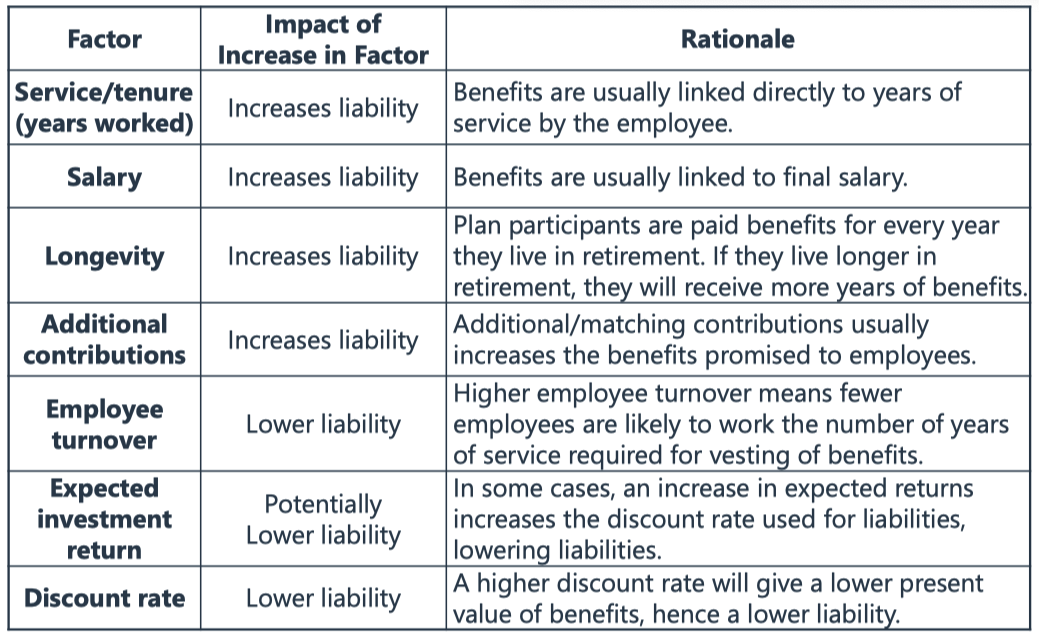

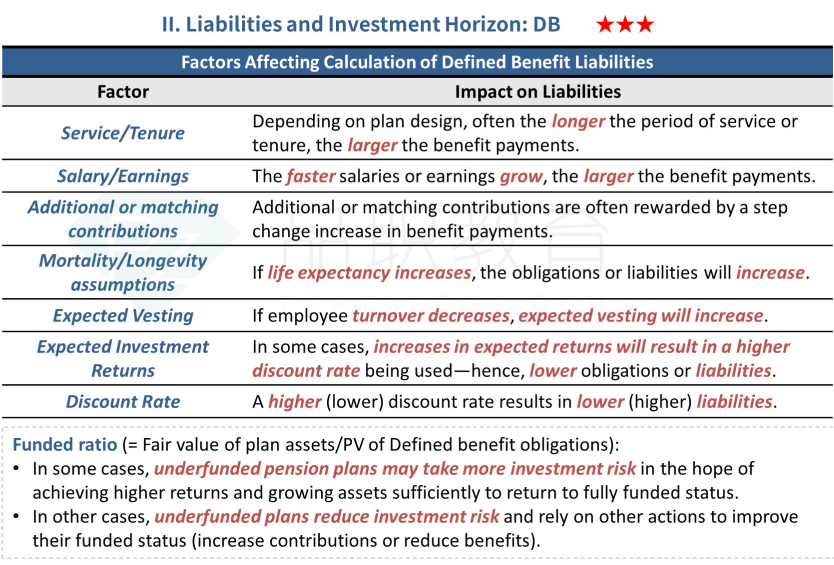

Caluculation PBO <- DB liability

Prob of Alive * ratio * final wage * working year

final wge = initial wage * (1+g)^T

分子

Funded Ratio =

Fund Status, F.S. = PA - PBO

if FS < 0, underfunded, then the pension plan may have high risks, 当FS负数,风险高,对于 risk tolerance investors may cannot increase the investment return 因为提高 return 则 risks 一般也会提高,但是FS已经<0了。

Then, 怎么办? 提高 sponsor's contribution

由公式可以看出影响 PBO的因素

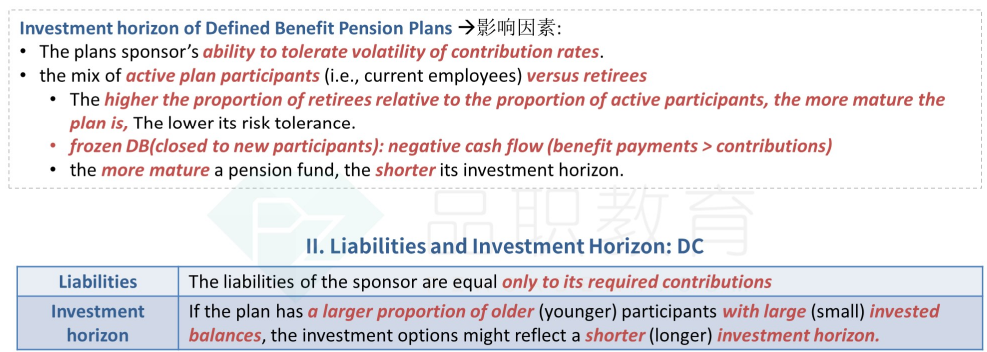

Investment Horizon

投资期限越长,意味着 ability to tolerate volatility of contribution rates 越大。能承受更多风险

people are older, pension plan gets more mature, might have less risk tolerance 人越老,pension越mature ,越老承担风险多能力越低

the more mature the pension fund, the shorter the investment horizon pension的期限越短,对流动性需求越高,investment horizon越短

frozen 的养老金计划(没有新人增加的),此时随着时间过去,老人变老,承担风险能力变低

negative CF (benefits payment > contribution)

External Constraints (Reporting)

Regulation 要披露 fees and costs both internally and externally

tax perspectives: pension funds have favorable tax treatment

(1) 必须report (2)accounting rules 在B/S上披露 net funded status

PA <- fair market value

PBO <- the blended approach

discount the funded portion using (higher )expected return on PA, and discount the unfunded portion based on the (lower) yield on tax-exempt municipal bond

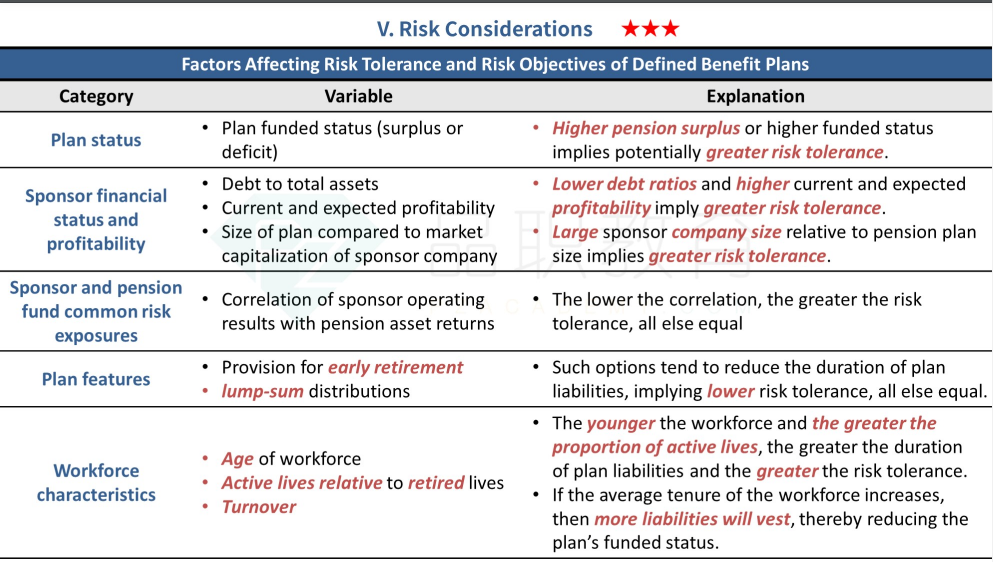

Risk Consideration 承担风险的多能力 5个影响承担风险能力的因素 (above or below average)

plan status 目前上 surplus or deficits, higher surplus implies greater risk tolerance

Firm's financial status and profitability: 公司经营越好,pension承担风险能力越低。因为公司可以contribute. greater firm's profitability, less the debt ratio, then greater ability to tolerent risks

Sponsor and pension fund risk exposure (correlation between sponsor's business & pension) 公司business和 pension 相关性corr越小,则两者风险可以diversified,risk tolerance强

Plan features 提前退休 early retirement & lump sum distribution 一笔大提款,会降低 risk tolerance 如果fund可以提前提款等,则对流动性liquidity需求高,则 less risk tolerance

workforce characteristics 人员结构相关的 人越年轻 risk tolerance 越好,因为能往pension里贡献钱越多

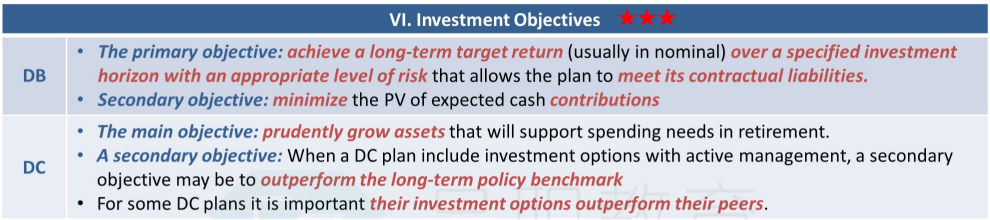

Investment Objective

Match liability with assets (PBO & PA)

Minimise Contribution

DC Plan

Plan Sponsors 不负责 investment risks

IPS Pension Fund

Stakeholders

Liability and Investment Horizon

Liquidity Needs

External Constraint

Risk Consideration

Investment Objective

Asset Allocation

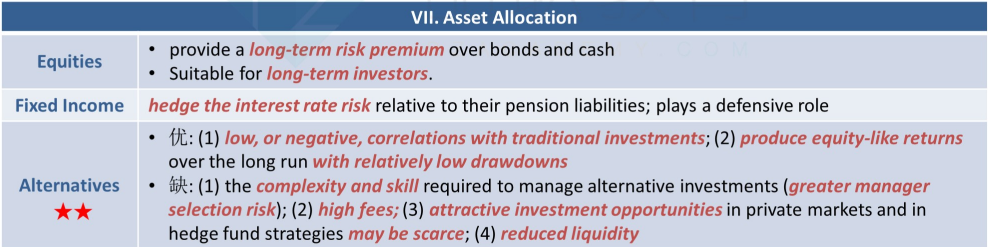

Pension Asset Allocation

如果 pension 的 lia payment 稳定,所以要有稳定的asset匹配支出。所以买 bonds

如果 time horizon 长,可以承担更多risks,为了减少contribution可以增加高收益的,买 equity

如果为了抗通胀 (1) risk tolerance低,买TIPS 通胀债券 (2) risk tolerance 高,如人员年轻 可以买 RE Commodity

P.S. remember, alternative investments

require higher specialties, require complexity and skills (greater selection risks)

higher fees (because of high management and skills)

for Pension Fund (large scale), attractive opportunity might be scarce.

reduce liquidity of the fund, such as private real estate

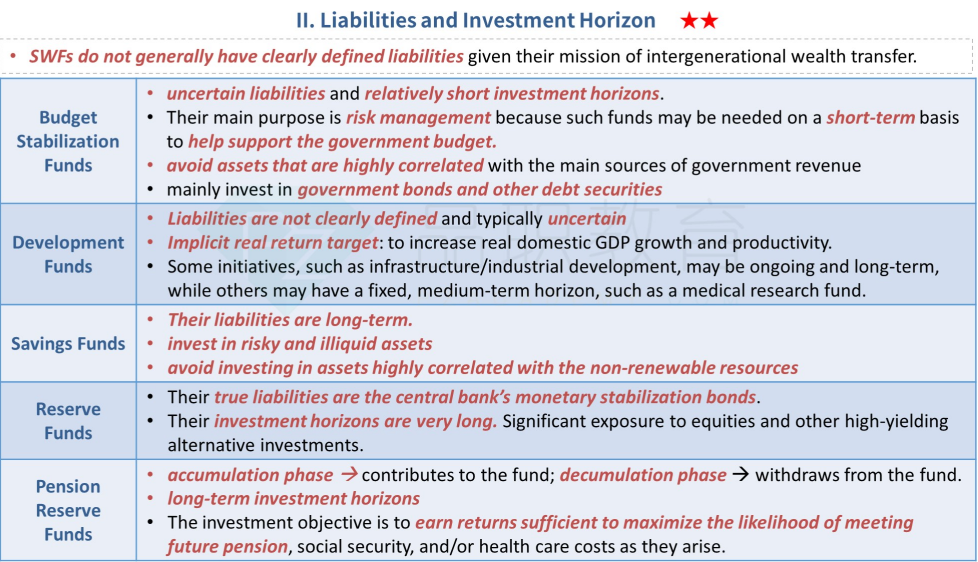

SWF Sovereign Wealth Funds

Type

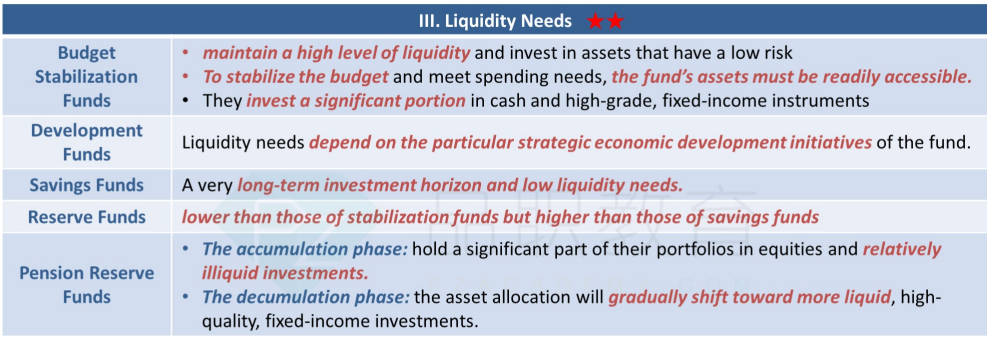

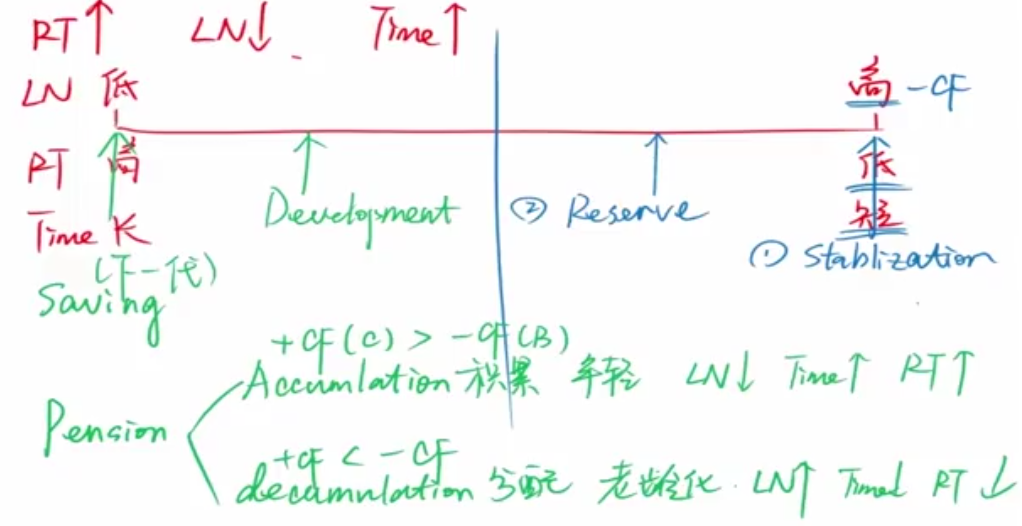

Budget Stablisation Funds 平准基金 insulate the budget & economy from commodity price volatility and external shocks 用于平衡经济和财政,from 大宗价格变化,如俄罗斯石油

Chile: Economic and Social Stabilization Fund; Timor-Leste Petroleum Fund; Russia’s Oil Stabilization Fund

Development Funds 发展基金 support economic development

造桥修路 infrastructure,由 project 项目主导

Mubadala (UAE); Iran’s National Development Fund; Ireland Strategic Investment Fund

Saving Funds 储蓄基金,share wealth across generations by transforming proceeds from the sale of non-renewable assets into long-term wealth and diversified financial assets

用于把能源开采提前赚的钱投资起来,避免将来能源枯竭了没钱了

Abu Dhabi Investment Authority; Kuwait Investment Authority; Qatar Investment Authority; Russia’s National Wealth Fund 如沙特

Norway 北海油田的钱

Reserve Funds 外汇储备基金,reduce the negative carry costs of holding reserves

用于稳定外汇,reduce the negative carry costs of holding reserves or earn returns on ample reserves

China Investment Corporation; Korea Investment Corporation; GIC Private Ltd. (Singapore)

Pension Reserve Funds 为了保证国家pension outflows . Set to meet identified future outflows of pension payments

National Social Security Fund (China); New Zealand Superannuation Fund; Future Fund of Australia

SWF IPS

Stakeholders

the ultimate SWF stakeholders are the current and future citizens (or residents)

the management or investment office: invest according to investment policy and objectives

SWF's board: oversee the management or investment, and has a fiduciary duty to the ultimate beneficiaries

Liabilities and Investment Horizon

Liquidity Needs

External Constraints

Legal and Regulatory: transparent and accountable manner

Tax: tax-free

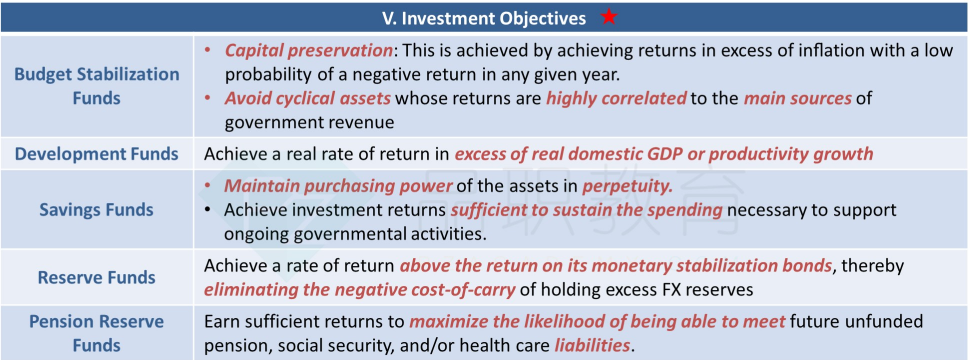

Investment Objectives

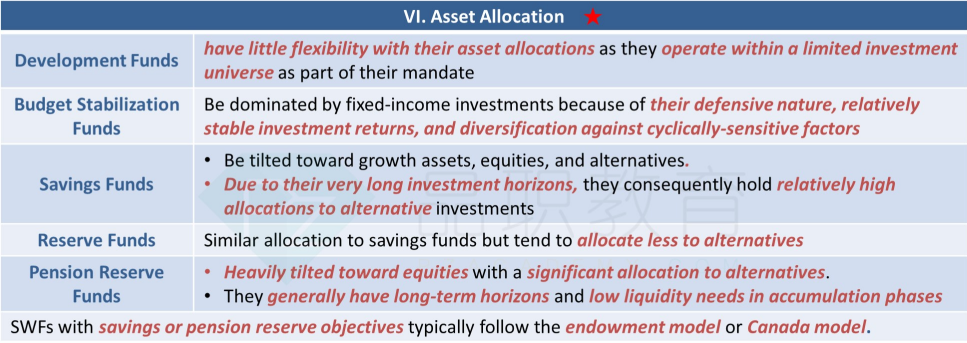

Asset Allocation

Budget stabilization funds.

The majority of fixed income and cash is due to the defensive nature of the fund.

Development funds.

These are driven by the socioeconomic mission of the fund (e.g., investment in local infrastructure projects).

Savings funds.

A long investment horizon means relatively high allocations toward equities and alternative investments, such as private equity and real assets.

Reserve funds.

Allocations are similar to those of savings funds, but with lower allocation to alternatives due to the potentially higher liquidity needs. 大多数为低风险的,因为 RT(risk tolerence)低,但是为了挣收益还需要配少部分alternative高收益

Pension reserve funds.

These have high allocations to equities and alternatives due to a long investment horizon and low liquidity needs in the accumulation phase.

Risks Tolerance

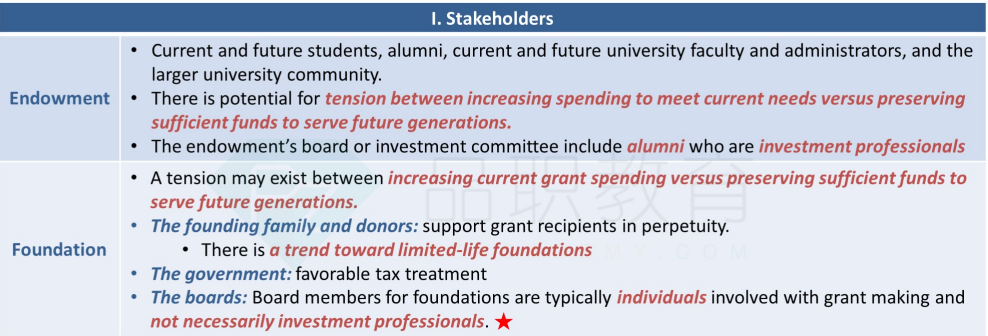

Endowment & Foundations 如校园基金会

Stakeholders

Stakeholder: Student Alumni, employees 因为免税,所以没有 government作为 stakeholder

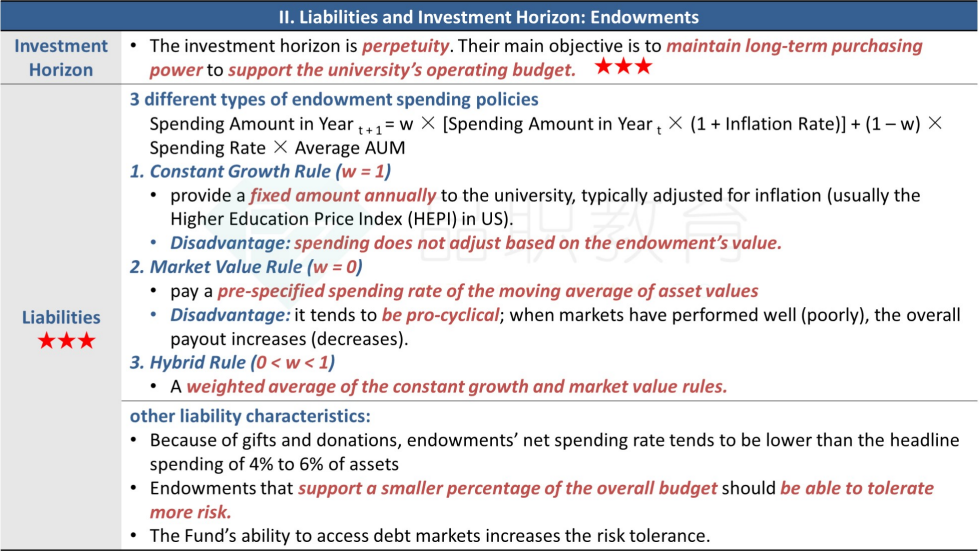

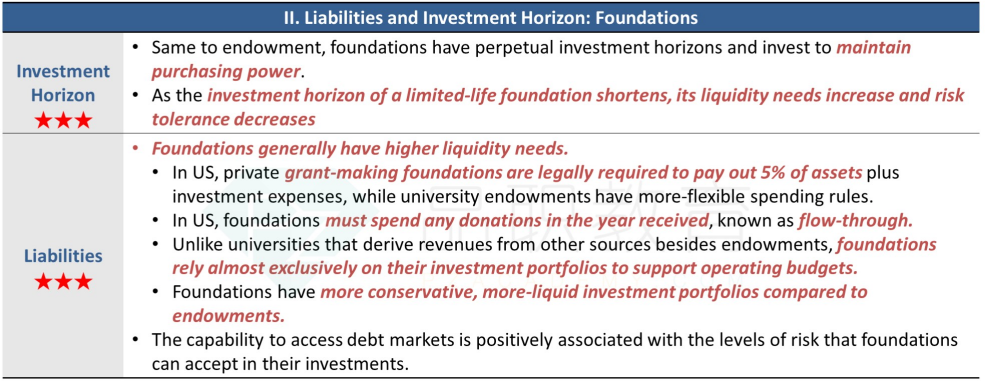

Liabilities and Investment Horizon: Endowments

Time Horizon: perpetual

Pending Rules:

Constant Growth Rule: if w = 1, then

Market Value Rule: if w = 0, then

Hybrid Rule:

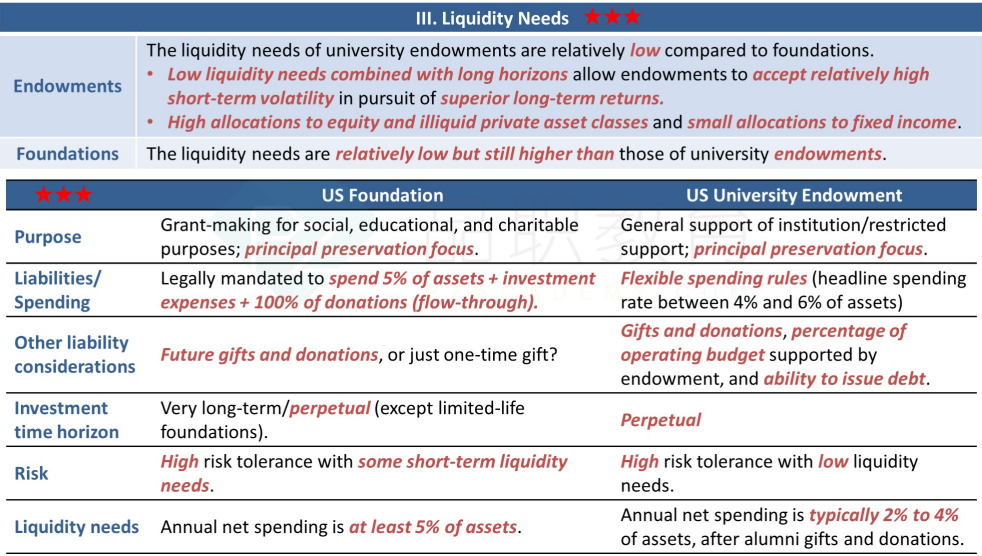

Liquidity Needs

flow-through: A flow-through entity is a legal business entity that passes any income it makes straight to its owners, shareholders, or investors. 相当于 donate 对钱,直接立刻全部花掉,且不占用 5% 的额度

External Constraints

requirement investor boards/committees/officers to invest on a total return basis and consider portfolio diversification

fiduciary duty

typically enjoy tax-exempt status

Investment Objectives

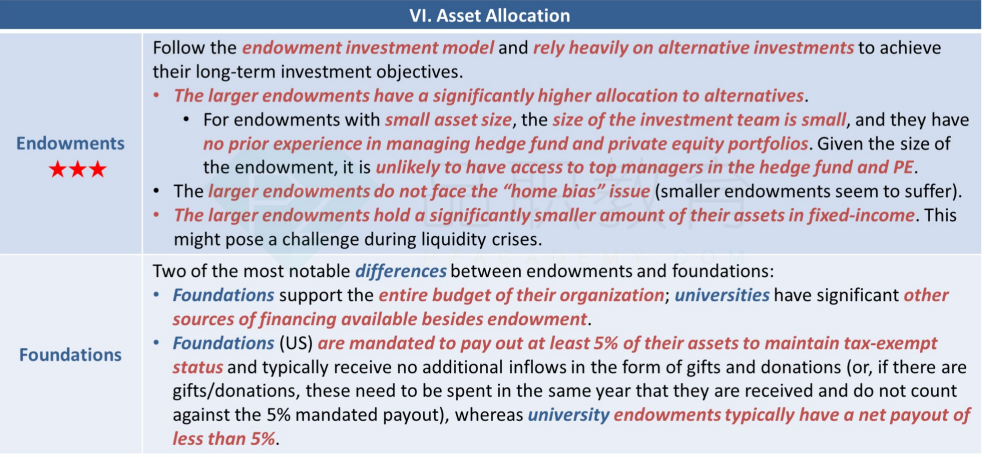

Asset Allocation

Difference Between US Foundations and University Endowment

| US Foundations 主要是慈善 | US University Endowment 主要是维持运营 | |

|---|---|---|

| Purpose | Grant-making for social, educational, and charitable purposes; principal preservation focus. | General support of institution or restricted support; principal preservation focus. |

| Stakeholders | Founding family, donors, grant recipients, and broader community that may benefit from foundation’s activities. 有政府 | Current/future students, alumni, university faculty and administration, and the larger university community. 无政府 |

| Liabilities/ Spending | Legally mandated to spend 5% of assets + investment expenses + 100% of donations (flow- through). | Flexible spending rules (headline spending rate between 4% and 6% of assets) with smoothing. 无spending rule但是一般在4-6 |

| Other liability considerations 收入来源 | Future gifts and donations, or just one-time gift? | Gifts and donations, percentage of operating budget supported by endowment, and ability to issue debt. |

| Investment time horizon | Very long-term/perpetual (except limited-life foundations). | Perpetual |

| Risk | High risk tolerance with some short-term liquidity needs. | High risk tolerance with low liquidity needs. |

| Liquidity needs | Annual net spending is at least 5% of assets. | Annual net spending is typically 2% to 4% of assets, after alumni gifts and donations. |

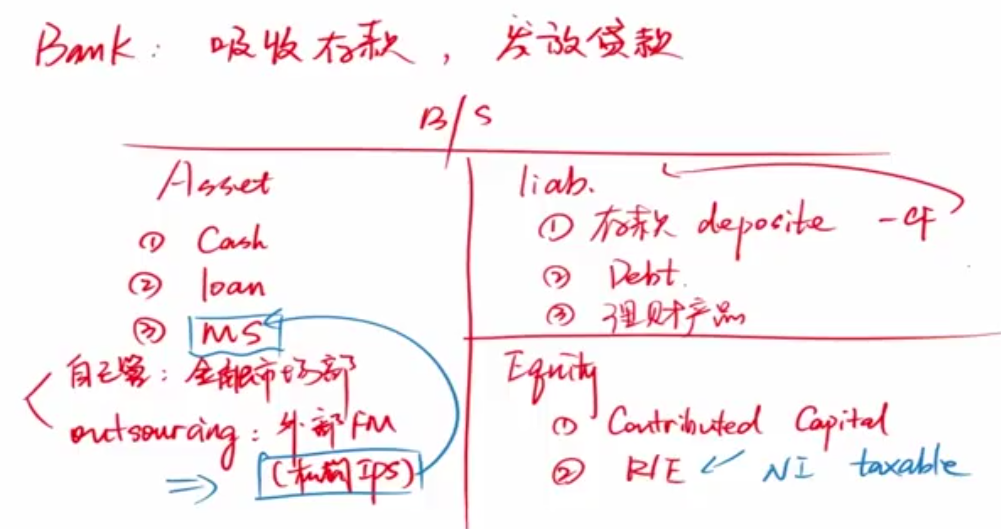

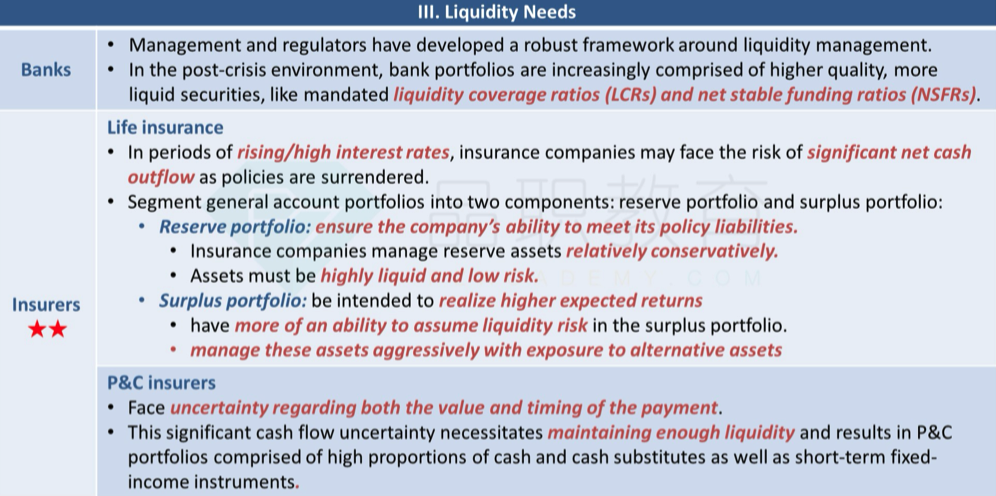

Banks & Insurers

银行会面临 Asset Lia 期限错配的问题,久期错配

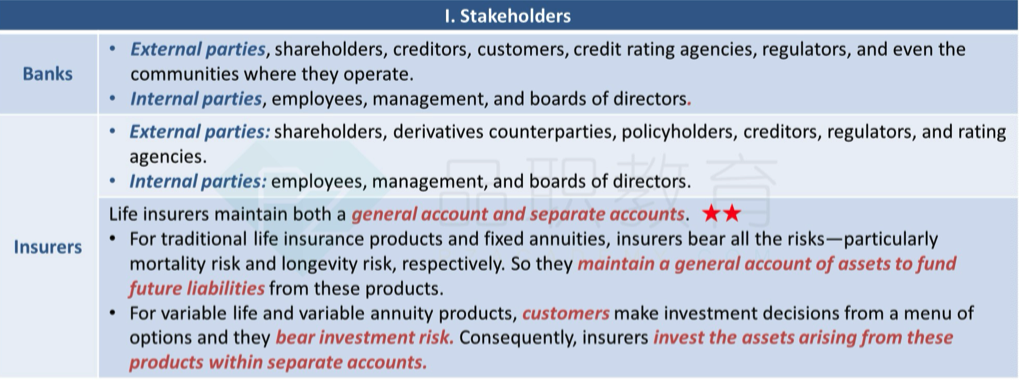

Stakeholder

shareholders

Customer: Borrower & Depositor

Internal stakeholders: employees, managers, director

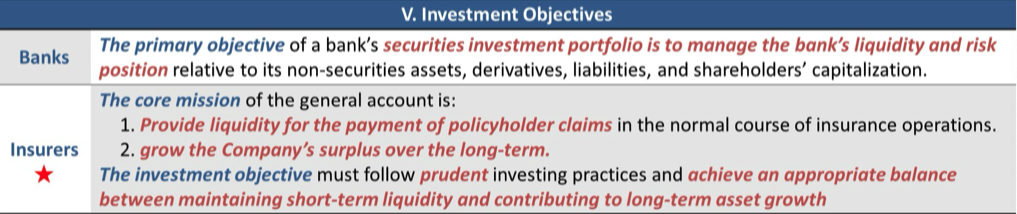

Investment Objectives

Manage Liquidty Needs, reduce risk mismatch

establish a ALM committee that sets the IPS, monitor performance, etc

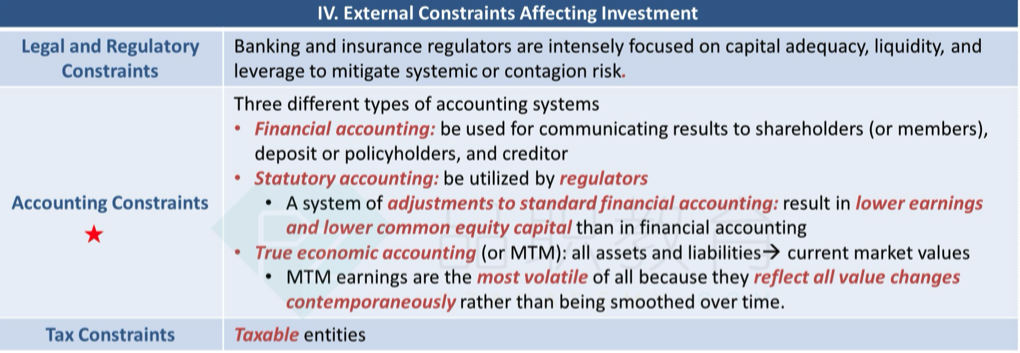

Constraints

Legal and Regulatory perspectives: 因为银行时 systematically important 所以有更多的监管

typically are fully taxable entities

Accountancy Perspective 也是因为银行重要,所以一般会做三份报表

standard financial report by GAAP or IFRS 由于很多银行时上市公司,报表要符合准则

statutory accounting by regulatory 由监管要求的,一般会conservative

True Economic Accounting using market value 反应其真实经济情况的

IPS

Stakeholders

Liability and Investment Horizon

Liquidity Needs

External Constraints

Investment Objectives

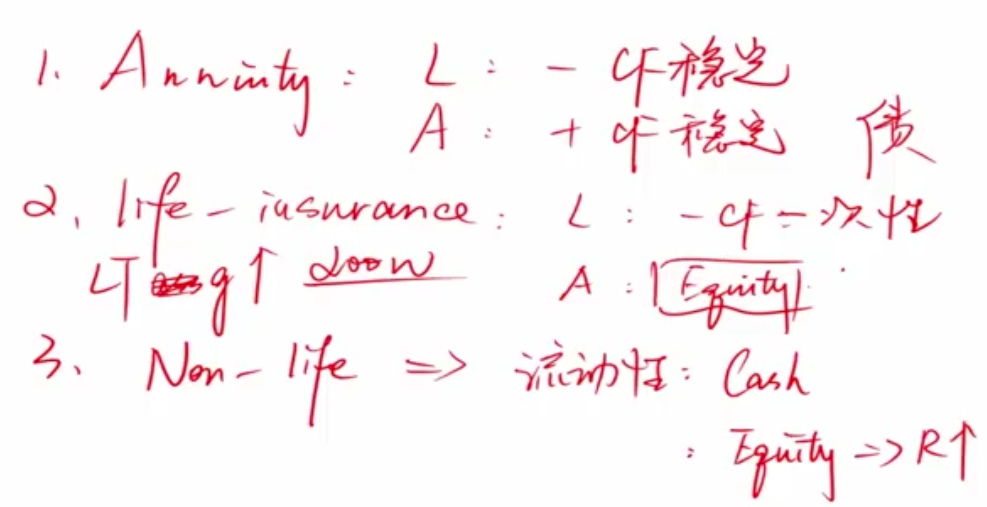

Insurers 保险公司 见individual的章节

Life Insurers 寿险

死亡险 whole & term 保终身 & 保一段时间

annuity 年金 Fixed & Variable * immediate & delayed 2*2

Property and Causlty (P&C) Insurers

车险

房屋险

巨灾险

Diff 在于能否重复投保

Stakeholders

Publicly listed companies 上市公司

Multual companies 互助公司 由投保人设立 owned by their policyholders, either retaining profits as a surplus against potential losses or distributing them to policyholders through dividends or premium reductions.

general account 投资风险 investment risks 由 insurer 保险公司承担

separate account 在这个账户内 投资产品由policyholder受保人选择,所以 investment risk 由 policyholder 自己承担

Difference between Life Insurance & PC Insurance

Time Horizon 寿险长,PC短

巨灾险损失

long tailed

理赔周期长 3-6个月

Replacement coverage 只有 PC可以抗通胀

Underwriting Cycle 寿险周期长 受econ cyc影响小

LN流动性需求,PC险大

Asset Allocation

相对利率敏感性 寿险周期长,久期高,所以 r 变化对寿险影响大

Investment Objectives

Manage Liquidity

Reduce risk mismatch

定量计算

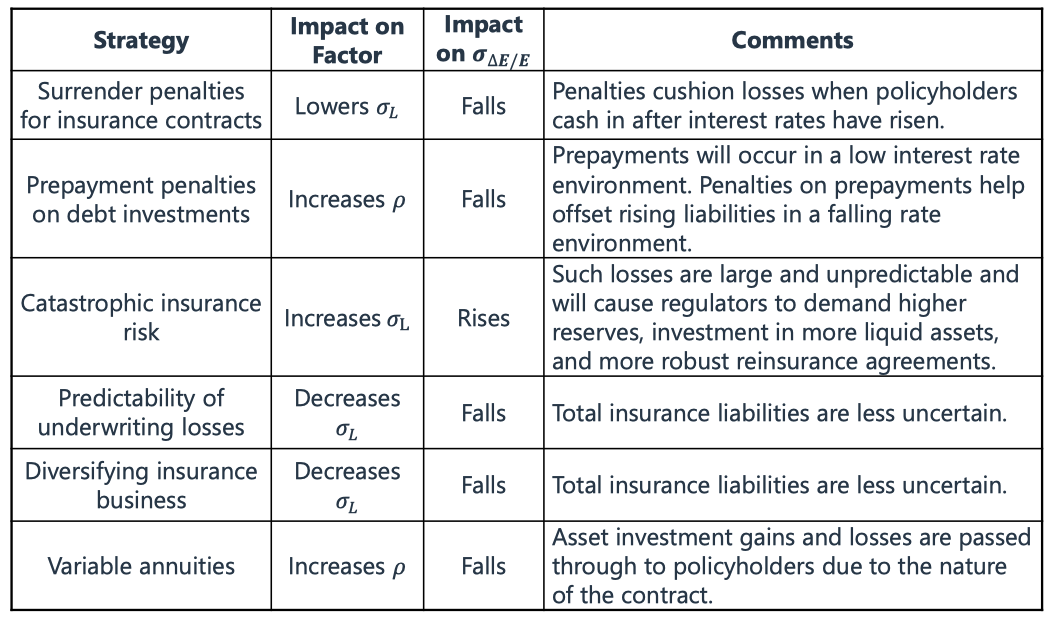

退保 Surrender

当利率 r 上升,由于 liability 和 asset 的 duration 不同,资产的久期一般比负债的大,那么利率上升,资产减数更大,会造成资不抵债

解决办法 1. 不处理 。

解决办法 2. 处理。

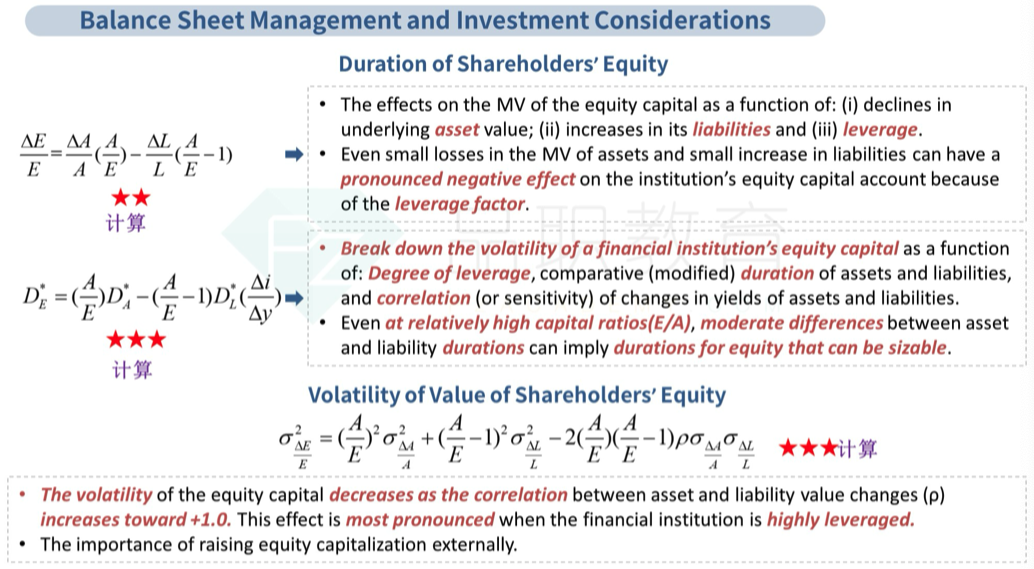

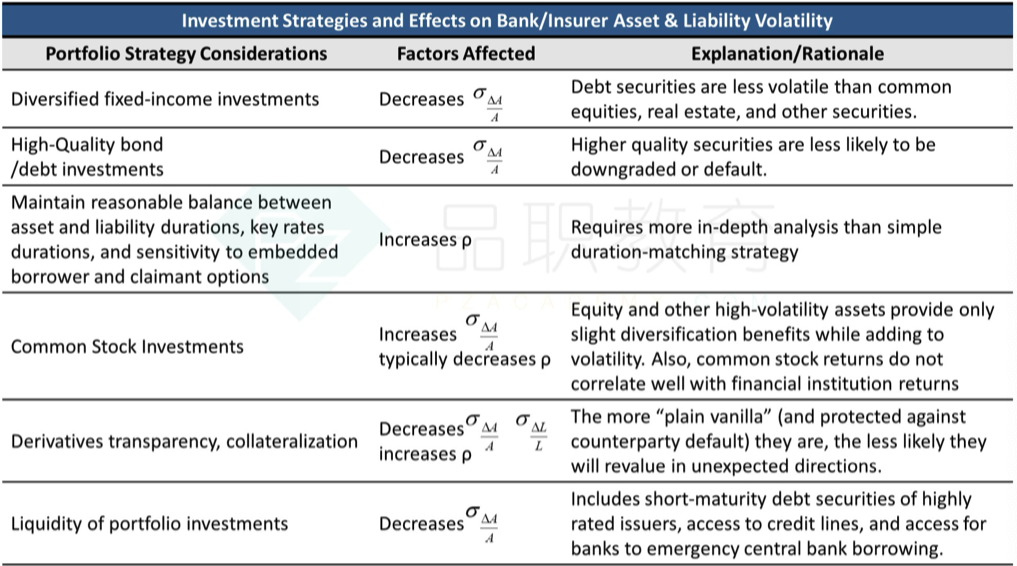

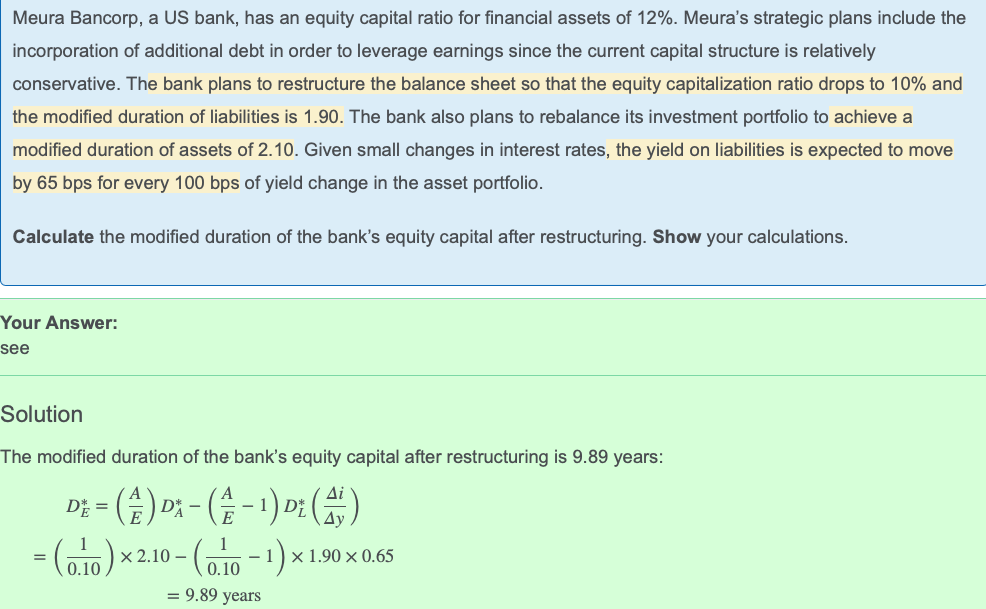

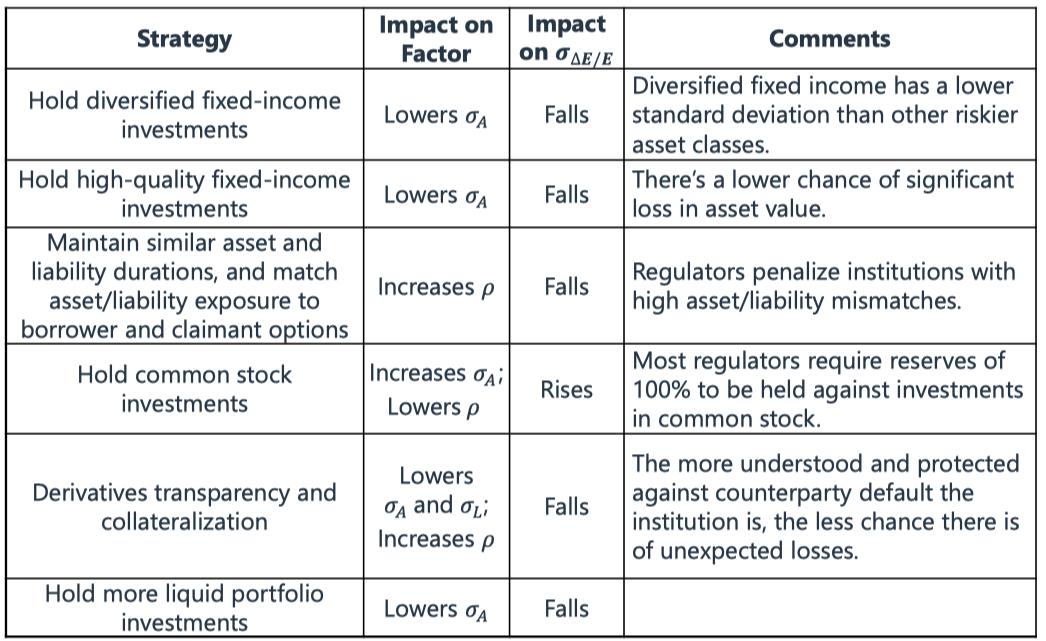

Bank & Insurers: Balance Sheet Management

LDI (Liability Driven Investing)

Return of Equity

For the portfolio (total portfolio is "E")

Portfolio Duration

We consider E = A - L, 其中 A 占 A/E, L占 -L/E

Duration of E 加权平均

As the interest rates for Asset and for Lia are different, the adjustment is consider to adjust A & L's interest rates. Let

btw, the liability is has less rate, duration is less affected by interest rate change, so the adjustment is less than 1.

or Generally,

So,

So,

In a portfolio

or,

Portfolio RIsks

影响因素

Sample Text

Evaluate risk considerations of private defined benefit (DB) pension plans in relation to 1) plan funded status, 2) sponsor financial strength, 3) interactions between the sponsor’s business and the fund’s investments, 4) plan design, and 5) workforce characteristics

Liquidity Management

Liquidity Profiling and Time-to-Cash Table

| Time to Cash | Liquidity Classification | Liquidity Budget (% of the port) |

|---|---|---|

| < 1 Week | Highly Liquid | At least 10% |

| < 1 Quarter | Liquid | At leasr 35% |

| < 1 Year | Semi-Liquid | At least 50% |

| > 1 Year | Illiquid | Up to 50% |

Rebalancing and Commitments

Systematic rebalancing policy. based on discipline 依据准则,如calendar, percent-range rebalancing

Automatic Rebalancing 在自己portfolio中,高流动性和低流动性大权重调整

Stress Testing

use historical data

use statistical assumption, Monte Carlo, VaR

scenario analysis

Derivatives

Sell Stocks <=> Short Derivatives (short futures)

没有直接买卖股票,所以没有realised gain/loss

Earning an Illiquidity Premium

Illiquid Asst Price = Marketable Asset Price - Put Price

因为只要能买到put,就能保证一定等把它卖掉,可以保证流动性

Illiqudity Premium(%)=Expected Return on Illiquid Asset % - Expected Return on Marketable Asset % 即流动性差的 - 流动性好的 return 的差值