Facts

- Trump Administration is widely seen as likely to increase or maintain high fiscal deficits.

-

To assess the impact of large deficits on yields, it is important to look at the total debt in the economy,

not just government debt.What matters for markets and the economy is how much collective new credit is being created, and the incentive and desire of investors to buy it.

-

Debt Supply & Demand amount would flow to Rate. If government spending increases, then it means debt supply increases (there would be more borrowing), pushing up rate to increase.

High Borrowing -> High Rate -> Depressed the private borrowing.

Low/Normal level of credit creation would otherwise drive down inflation.

Two Cases:

-

Bad Scenario: Push up Inflation.

Total Debt/GDP increase (private and public debt / GDP) increase && Currency Weaken. Then Yield Curve would steepen, derived by long term rate increase, as nobody purchase the long term bond.

Think about a graph with x-axis (term), y-axis (yield), and a upward sloping curve.

Yield curve steepens.

-

Good Scenario (now the US situation): Do not drive up Inflation

Under this case, no buyers are buying the long-term debts.

Total Debt/GDP increases, but yield curve is flat. Public squeezes private investment. The increase in public debt does not increase private borrowing, so no extra purchasing resulted from households. Help relieve the inflation.

Yield curve flattens.

-

Example:

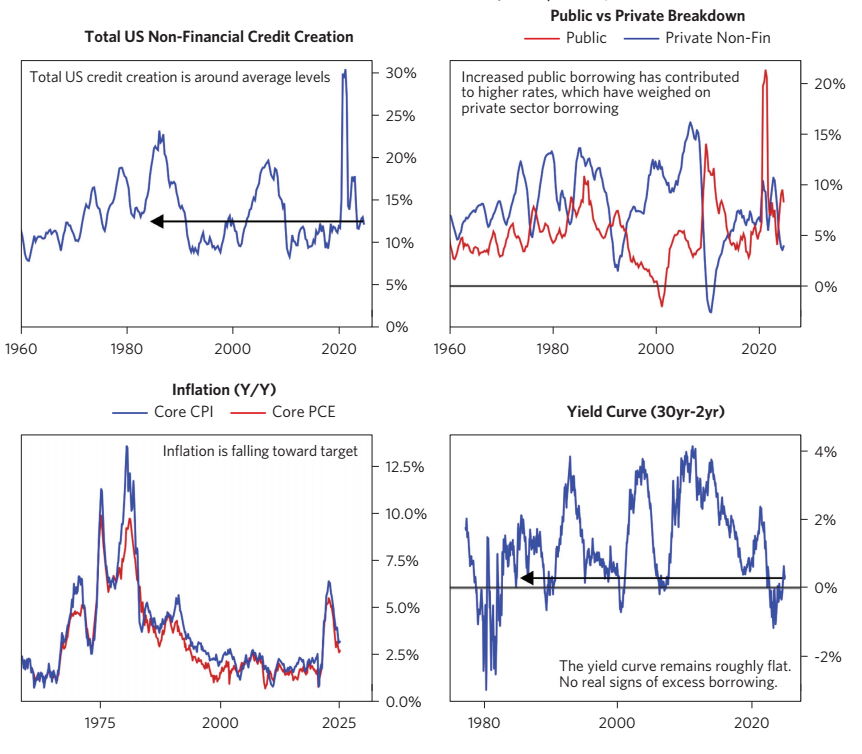

Now is the Good Scenario: The top-left figure shows the current credit creation in US is under normal level. Top-right figure shows that Public and Private debts are negative correlated. Public squeezes private, so total debt did not get up too much high.

1980s: Top-left figure shows total debts went high; Top-right figure shows public and private were positively correlated. So, bottom-left figure shows inflation hikes.

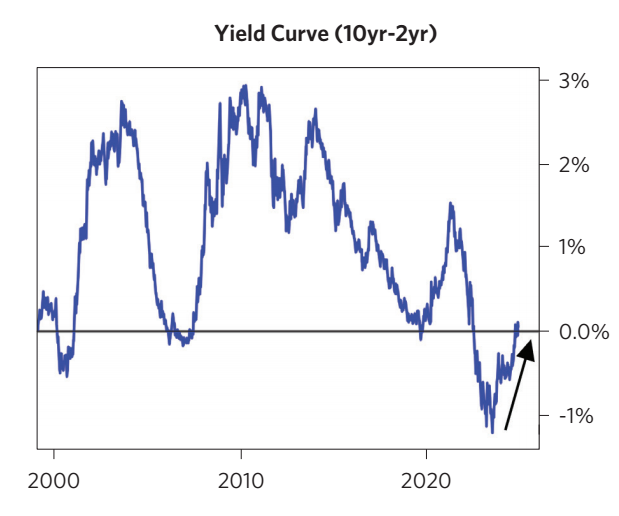

Bottom-right figure shows implicitly that the current long minus short term rate is at low level, imply that the yield curve is flat, consistent with our Good/Bad Scenario Rationale.

Supply & Supply Side of Debts

-

Supply Side: Currently, there are high public borrowing, and low private borrowing.

-

Demand Side:

Due to previous QE, Debt yield is high for investors => that would be attractive to un-levered investors, because Debts still bring enough return and less risks, attractive to people.

However, the levered investors fact different situation. As they hold debts already, high debt rate would become both their costs and returns.

-

The current real yield is about 2% in US, which is high relative to much of the rest of developed world. US nominal yields are at levels where the yield is attractive and diversifying relative to stocks allocation for those who need to supplement debts into their portfolio.

Again, the current yield curve is flat. For leveraged investors, they have debts liability already. Returns and Costs of debts offset.

Reference

Bridge-Water

Our Thoughts on Large US Deficits and Their Impact on Bond Yields