by Professor Aswath Damodaran who disclose some myths in this note.

Myth 1. The Fed as Rate Setter.

The Fed sets only one interest rate, the Fed Funds rate. FFR is an overnight intra-bank borrowing rate, and that none of the rates that we face in our lives, either as consumers (on mortgages, credit cards or fixed deposits) or businesses (business loans and bonds), are set by or even indexed to the Fed Funds Rate.

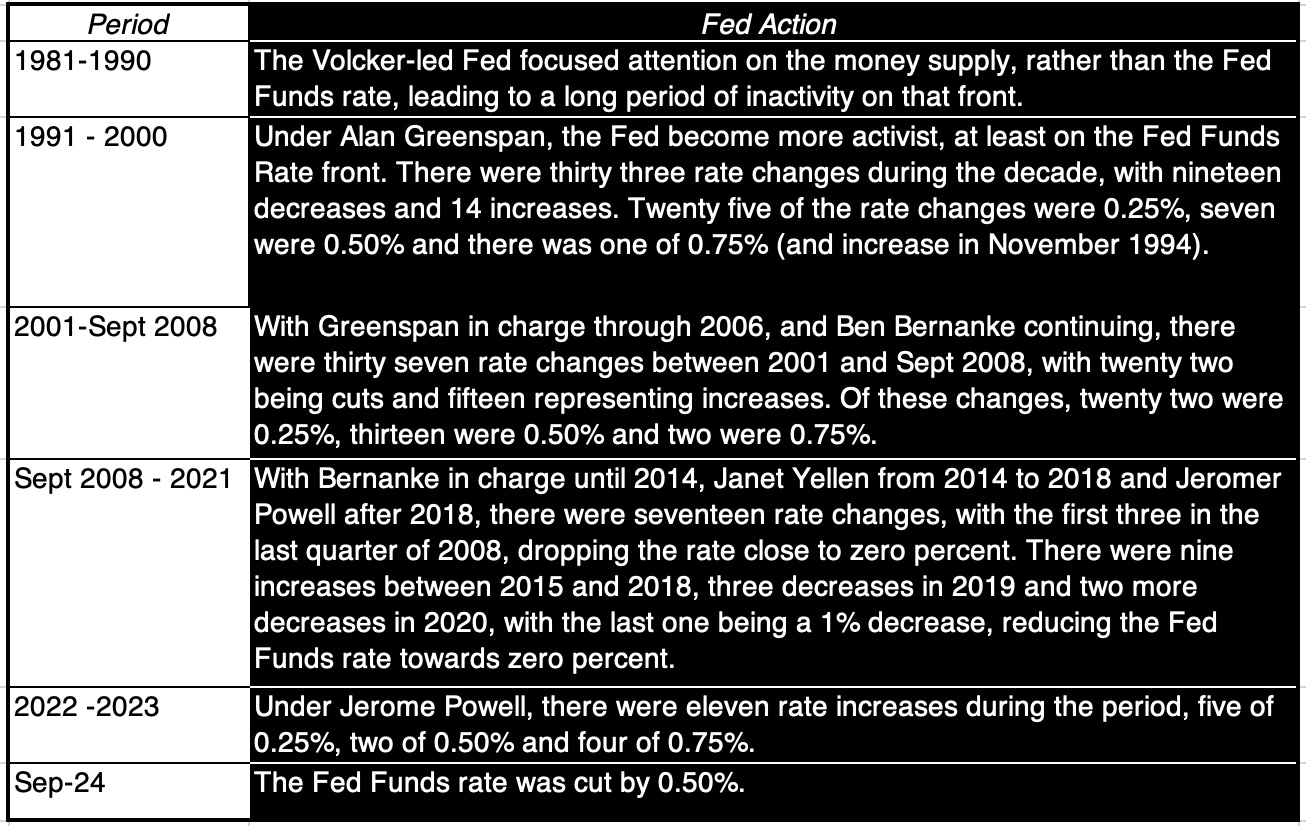

The Federal Open Market Committee (FOMC) has the power to change this rate, which it uses at irregular intervals, in response to economic, market and political developments. FOMC meets 8 times each year.

The table below lists the rate changes made by the Fed in this century:

FFR is a range such as 5.00%-5.25%, so we usually use the effective FFR, which shrink to a figure.

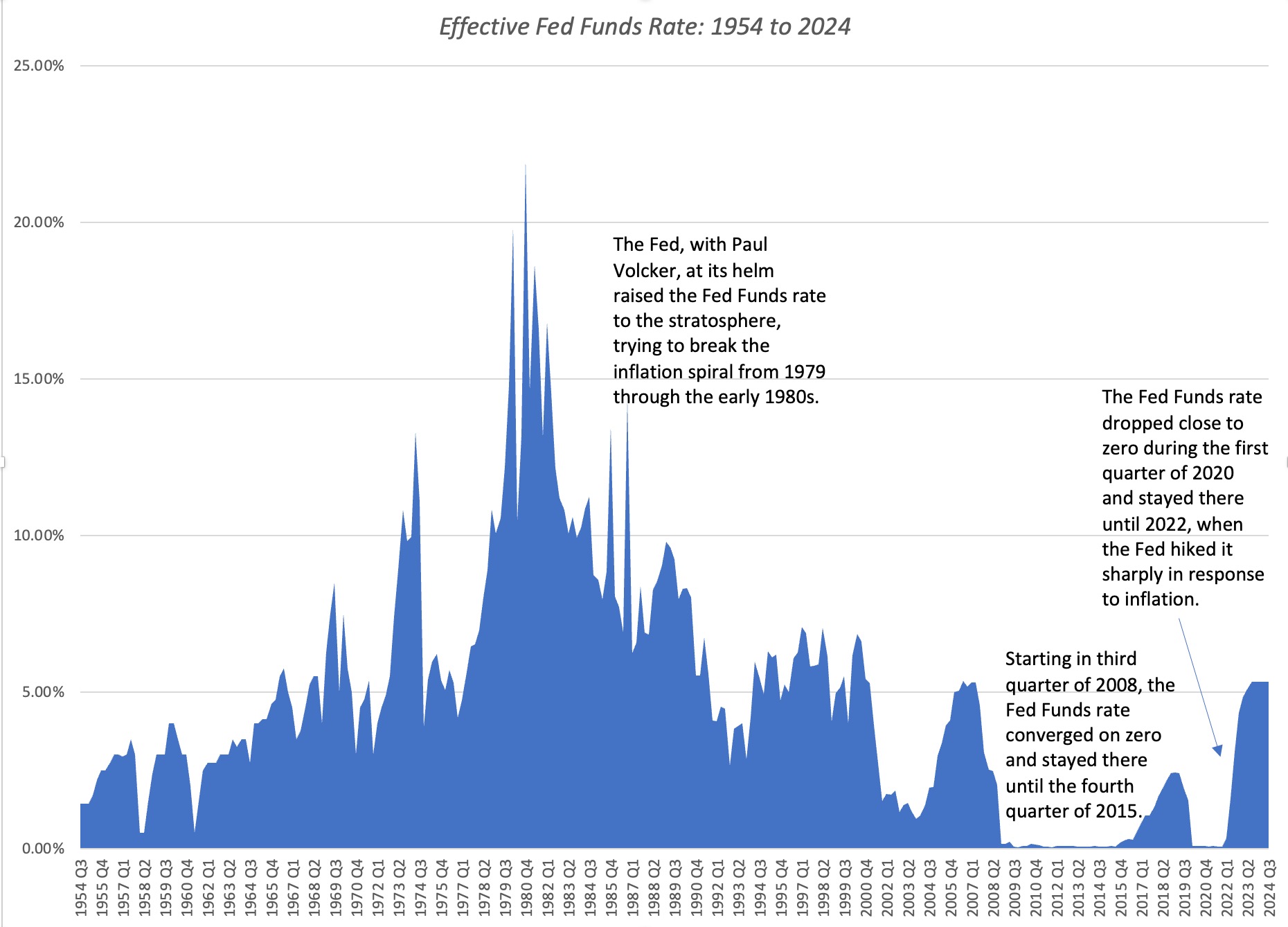

The Figure below shows the move of effective FFR over time.

There are two periods that stand out.

- The first is the spike in the Fed Funds rate to more than 20% between 1979 and 1982, when Paul Volcker was Fed Chair, and represented his attempt to break the cycle of high inflation that had entrapped the US economy.

- The second was the drop in the Fed Funds rate to close to zero percent, first after the 2008 crisis and then again after the COVID shock in the first quarter of 2020. In fact, coming into 2022, the Fed had kept the Fed Funds rates at or near zero for most of the previous 14 years, making the surge in rates in 2022, in response to inflation, shock therapy for markets unused to a rate-raising Fed.

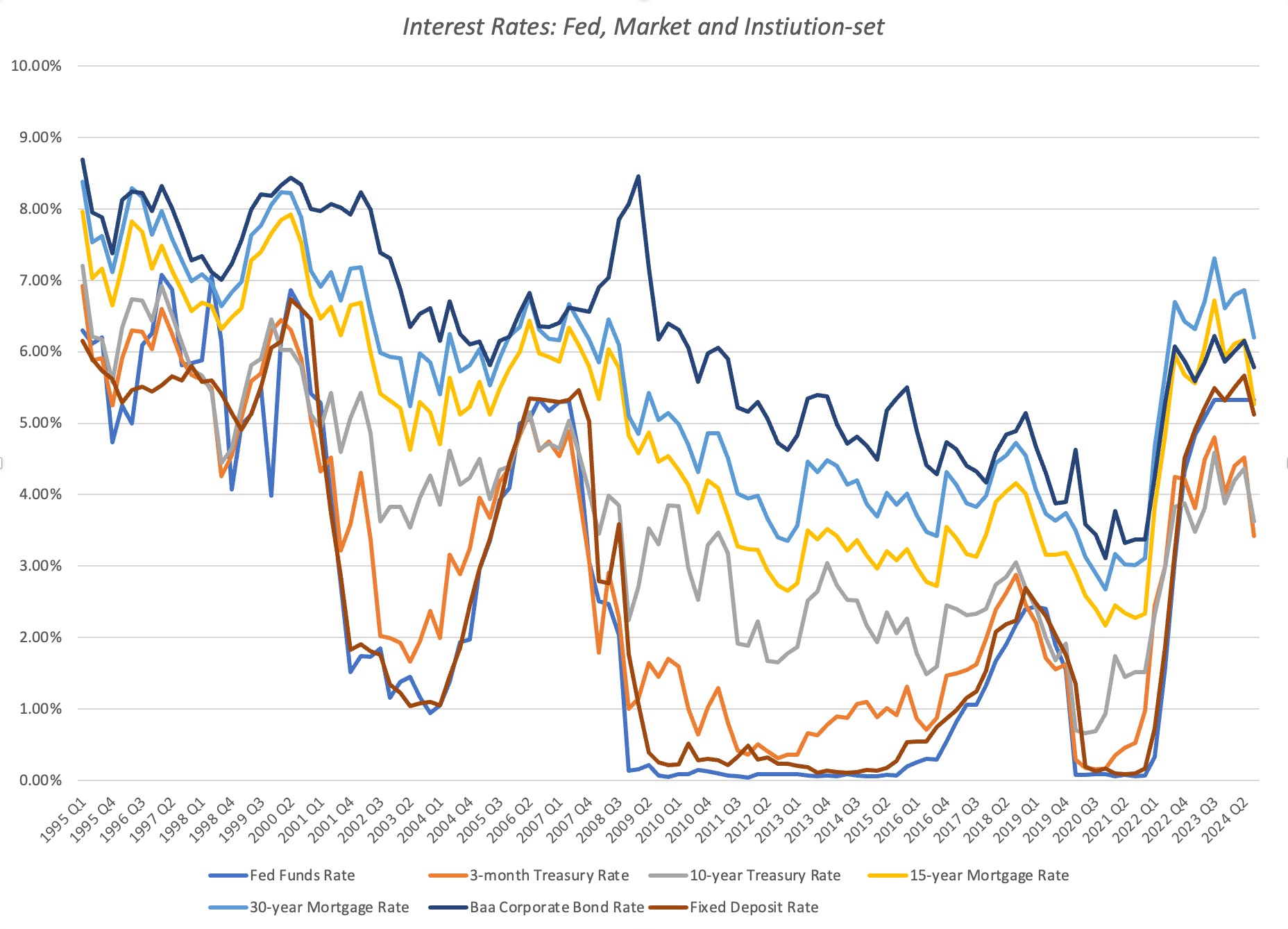

As noted that the Fed only set FFR, there are undoubtedly other interest rates you will encounter, but are not set by the Fed. Those other rates will fall into one of three buckets – (1) market-set interest rates, (2) rates indexed to market-set rates and (3) institutionally-set rates. None of these rates are set by the Federal Reserve, thus rendering the “Fed sets interest rates” as myth.

Myth 2. The Fed as Rate Leader

Although the Fed does not set rate directly, you may still believe that the Fed influences these rates with changes it makes to the Fed Funds rate.

The rates all seem to move in sync, though market-set rates move more than institution-set rates, which, in turn, are more volatile than the Fed Funds rate. The reason that this is a superficial test is because these rates all move contemporaneously, and there is nothing in this graph that supports the notion that it is the Fed that is leading the change. In fact, it is entirely possible, perhaps even plausible, that the Fed’s actions on the Fed Funds rate are in response to changes in market rates, rather than the other way around.

Some Statistics are provided by Professor Damodaran, as the Table below. To test whether changes in the Fed Funds rate are a precursor for shifts in market interest rates, a simple (perhaps even simplistic) test is provided. At the 249 quarters that compose the 1962- 2024 time period, each quarter was broken own into whether the effective Fed Funds rate increased, decreased or remained unchanged during the quarter. It seems undeniable that the “Fed as leader” hypothesis falls apart. In fact, in the quarters after the Fed Funds rate increases, US treasury rates (short and long term) are more likely to decrease than increase, and the median change in rates is negative. In contrast, in the periods after the Fed Fund decreases, treasury rates are more likely to increase than decrease, and post small median increases.

.jpeg)

Findings how that the Fed is more like an follower rather than a leader, when it comes to interest rate. What is the cause of the those interest rate then? How else can you explain why interest rates remained low for the last decades, other than the Fed?

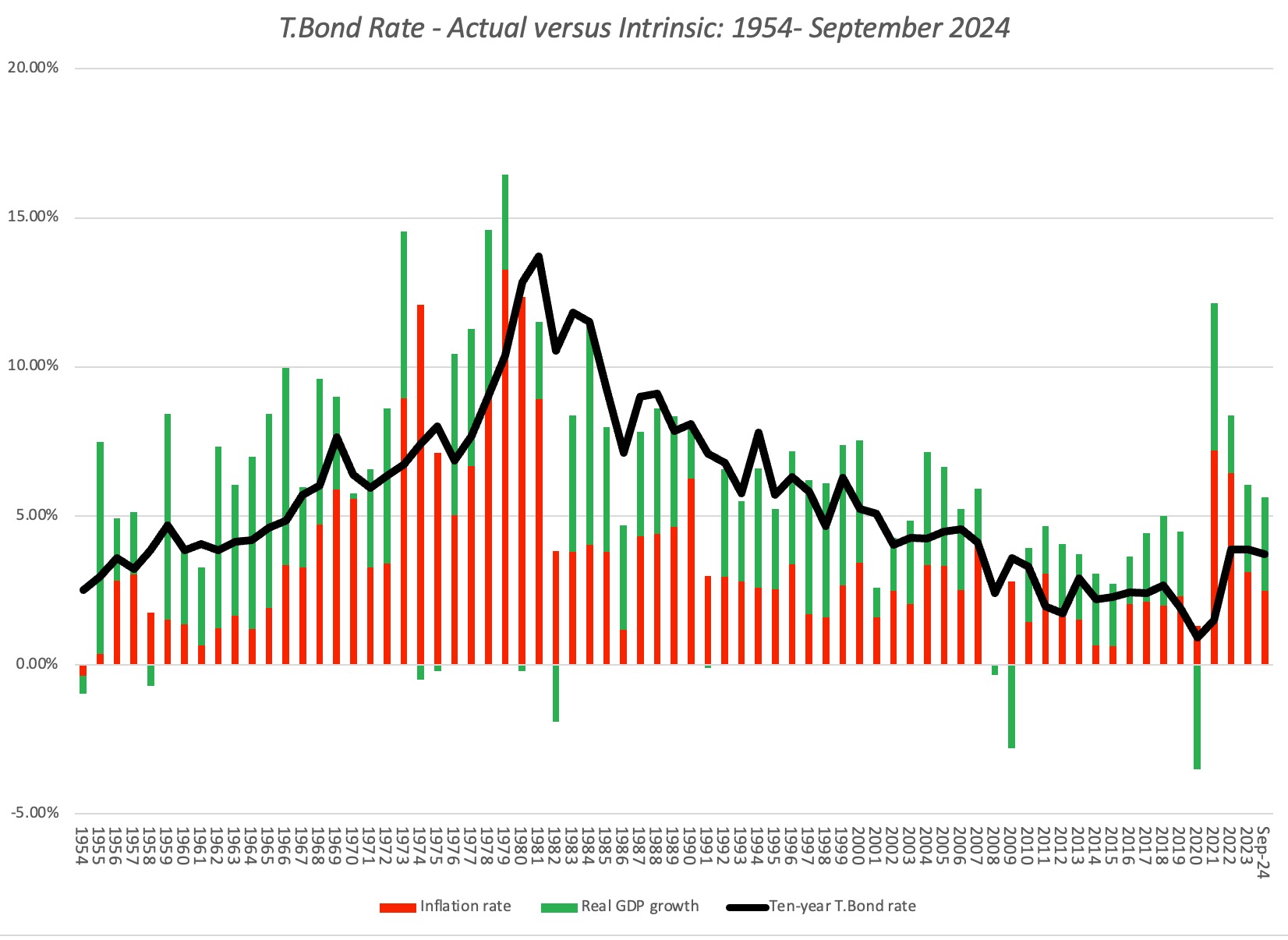

The answer is recognizing that market-set rates ultimately are composed of two elements: (1) expected inflation rate and (2) expected real interest rate, reflecting real economic growth. In the graph below, which the professor have used multiple times in prior posts, he compute an intrinsic risk free rate by just adding inflation rate and real GDP growth each year:

The figure is like the Taylor Rule. Interest rates were low in the last decade primarily because inflation stayed low (the lowest inflation decade in a century) and real growth was anemic. Interest rates rose in 2022, because inflation made a come back, and the Fed scrambled to catch up to markets, and most interesting, interest are down this year, because inflation is down and real growth has dropped. As you can see, in September 2024, the intrinsic risk-free rate is still higher than the 10-year treasury bond rate, suggesting that there will be no precipitous drop in interest rates in the coming months.

Myth 3. The Fed as Signalman

There are two major macroeconomic dimensions on which the Fed collects data,

- (1) real economic growth (how robust it is, and whether there are changes happening), and

- inflation (how high it is and whether it too is changing).

The Fed’s major signaling device remains the changes in the Fed Funds rate, and it is worth pondering what the signal the Fed is sending when it raises or lowers the Fed Funds rate.

- On the inflation front, an increase or decrease in the Fed Funds rate can be viewed as a signal that the Fed sees inflationary pressures picking up, with an increase, or declining, with a decrease.

- On the economic growth front, an increase or decrease in the Fed Funds rate, can be viewed as a signal that the Fed sees the economy growing too fast, with an increase, or slowing down too much, with a decrease.

These signals get amplified with the size of the cut, with larger cuts representing bigger signals.

The 50bp cut on the 18th of Sep means the mix. If you are an optimist, you could take the action to mean that the Fed is finally convinced that inflation has been vanquished, and that lower inflation is here to stay. If you are a pessimist, the fact that it was a 50bp decrease, rather than the expected 25bp, can be construed as a sign that the Fed is seeing more worrying signs of an economic slowdown than have shown up in the public data on employment and growth. There is of course the cynical third perspective, which is that the Fed rate cut has little to do with inflation and real growth, and more to do with an election that is less than fifty days away.

In sum, signaling stories are alluring, and you will hear them in the coming days, from all sides of the spectrum (optimists, pessimists and cynics), but the truth lies in the middle, where this rate cut is good news, bad news and no news at the same time, albeit to different groups.

Myth 4. The Fed as Equity Market Whisperer

The Fed’s capacity to influence the interest rates that matter is limited, but you may still hold on to the belief that the Fed’s actions have consequences for stock returns. In fact, Wall Street has its share of investing mantras, including “Don’t fight the Fed”, where the implicit argument is that the direction of the stock market can be altered by Fed actions.

Based on the professor’s data, the S&P 500 did slightly better in quarters after the FFR decreased than when the rate increased, but reserved its best performance for quarters after those where there was no change in the FFR. Stock markets will be better served with fewer interviews and speeches from members of the FOMC and less political grandstanding (from senators, congresspeople and presidential candidates) on what the Federal Reserve should or should not do.

Myth 5. The Fed as Chanticleer

The Fed is like Chanticleer, with investors endowing it with powers to set interest rates and drive stock prices, since the Fed’s actions and market movements seem synchronized. As with Chanticleer, the truth is that the Fed is acting in response to changes in markets rather than driving those actions, and it is thus more follower than leader. That said, there is the very real possibility that the Fed may start to believe its own hype, and that hubristic central bankers may decide that they set rates and drive stock markets, rather than the other way around.

Conclusion

The delusion shall be broken. The Fed did not lead the market but follow the market. Analyse the instruction of Fed might miss the cause and effect. Should do analyse the following factors.

It has distracted us from talking about things that truly matter, which include growing government debt, inflation, growth and how globalisation may be feeding into risk, and allowed us to believe that central bankers have the power to rescue us from whatever mistakes we may be making.

The Fed Delusion has destroyed enough investing brain cells for those who holding on to the delusion cannot let go. Do not hear talking among this group about what the FOMC may or may not do at its next meeting (and the meeting after that), and what this may mean for markets, restarting the Fed Watch. The insanity of it all!

Reference

https://aswathdamodaran.blogspot.com/2024/09/fed-up-with-fed-talk-central-banks.html