We here derive why \(MRS_{x,y}=\frac{MU_x}{MU_y}\).

Let \(U(x,y)=f(x,y)\), and we know, by definition, MRS measures how many units of x is needed to trade y holding utility constant. Thus, we keep the utility function unchanged, \(U(x,y)=C\), and take differentiation and find \(-dy/dx\).

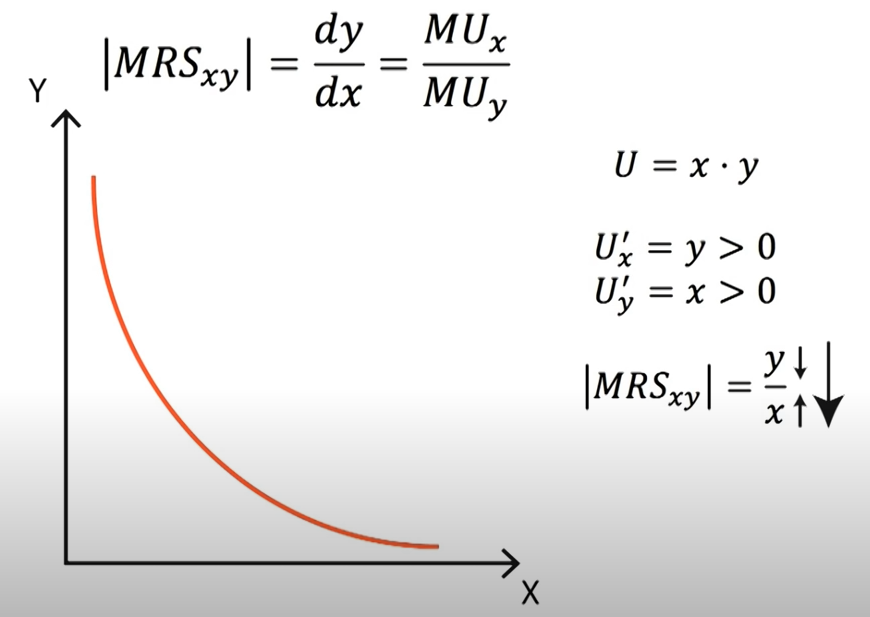

, which is similar as the Cobb-Douglas form but has exponenets zero.

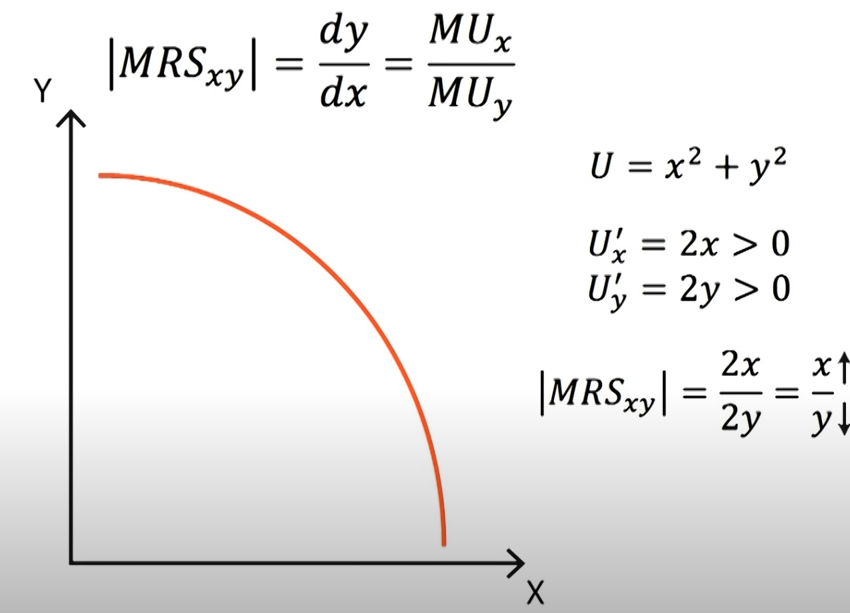

$$MRS_{x,y}=\frac{MU_x}{MU_y} =\frac{y}{x}$$

Example 3

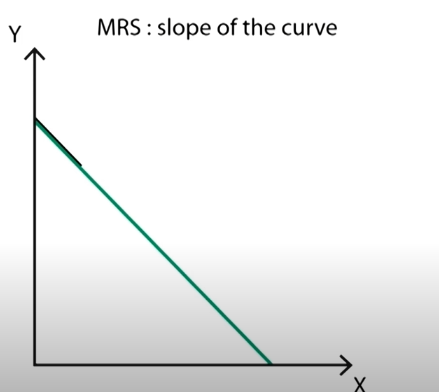

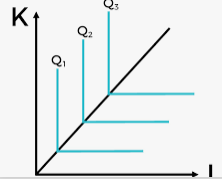

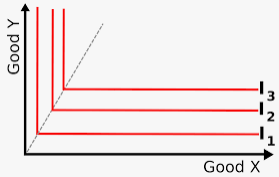

Perfect Substitution: MRS constant

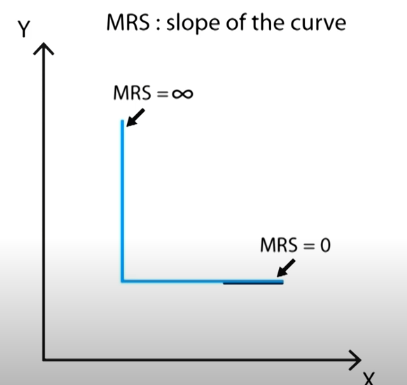

Perfect Complement

MRTS

Marginal Rate of Technical Substitution (MRTS) measures the amount of cost which a specific input can be replaced for another resource of production while maintaining a constant output.

While applying the Cobb-Douglas formed utility function, we are actually proxy the preference of people. (The utility function is like a math representation if individuals’ preference is rational). In the utility function, we are focusing more on the Marginal Rate of Substitution between goods.

P.S. Cobb-Douglas gives the same MRS to CES utility function. While solving the utility maximisation problem, we take partial derivatives to the lagrangian and then solve them. Those steps are similar to calculating the MRS.

The key is that the number or value of the utility function does not matter, but the preference represented by the utility function is more important. Any positive monotonic transformation will not change the preference, such as logarithm, square root, and multiply any positive number.

Exponents Do Not Matter

The powers of the Cobb-Douglas function does not really matter as long as they are in the “correct” ratio. For example,

$$ U_1=Cx^7y^1,\quad and \quad U_2=Cx^{7/8}y^{1/8} $$

$$MRS_1=\frac{7y}{x}\quad and \quad MRS_2=\frac{7y/8}{x/8}=\frac{7y}{x}$$

Therefore, we can find that those two utility functions represent the same preference!

Or we can write \(U_1=(U_2)^8 \cdot C^{-7}\). Both taking exponent and multiplying a positive constant are positive monotonic transformations. Therefore, the powers of Cobb-Douglas do not really matter to represent the preference. (\(U=Cx^a y^{1-a}\) the exponents of the utility function does not have to be sum to one).

CES could be either production or utility function. It provides a clear picture of how producers or consumers choose between different choices (elasticity of substitution).

CES Production

The two factor (capital, labour) CES production function was introduced by Solow and later made popular by Arrow.

Here, we get the substitution of K and L is a function of the price, w & r. As we are studying the elasticity of substitution, in other words how W/L is affected by w/r, we take derivatives later. We denote \(V=K/L\), and \(Z=w/r\). Then,

Therefore, we get the elasticity of substitution becomes constant, depending on \(\rho\). The interesting thing happens here.

If \(-1<\rho<0\), then \(\sigma>1\).

If \(0<\rho<\infty\), then \(\sigma<1\).

If \(\rho=0\), then, \(\sigma=1\).

Utility Function

Marginal Rate of Substitution (MRS) measures the substitution rate between two goods while holding the utility constant. The elasticity between X and Y could be defined as the following,

The elasticity of substitution here is defined as how easy is to substitute between inputs, x or y. In another word, the change in the ratio of the use of two goods w.r.t. the ratio of their marginal price. In the utility function case, we can apply the formula,

\(MRS_{X,Y}=\frac{dy}{dx}=\frac{U_x}{U_y}=p_x/p_y\) marginal price in equilibrium.

In the

$$ u(x,y)=(a x^{\rho}+b y^{\rho})^{1/\rho} $$

$$\sigma=\frac{1}{1-\rho}$$

If \(\rho=1\), then \(\sigma\rightarrow \infty\).

If \(\rho\rightarrow -\infty\), then \(\rho=0\).

Two common choices of CES production function are (1) Walras-Leontief-Harrod-Domar function; and (2) Cobb-Douglas function (P.S. but CES is not perfect, coz sigma always equal one).

As \(\rho=1\), the utility function would be a perfect substitute.

As \(\rho=-1\), the utility function would be pretty similar to the Cobb-Douglas form.

Later, the CES utility function could be applied to calculate the Marshallian demand function and Indirect utility function, and so on. Also, easy to show that the indirect utility function \(U(p_x,p_y,w)\) is homogenous degree of 0.

Reference

Arrow, K.J., Chenery, H.B., Minhas, B.S. and Solow, R.M., 1961. Capital-labor substitution and economic efficiency. The review of Economics and Statistics, 43(3), pp.225-250.

Say’s Law argues that the ability to purchase something depends on the ability to produce and the wealth. In order to have something to buy, the buyer has to get something to produce and sell. Thus, the source of demand is production, not the money itself. Therefore, production drives economic growth.

Say drew four main conclusions.

More producers would boost the economy.

If members of the society do not produce would drag the society.

Business entities with trading are benefitial when they near each other.

Encouraging consumption is harmful. Production adn accumulation of goods constitutes prosperity, but consuming without producing eat away the economy.

The implication is that government should support and control production rather than consumption.

Global Cooperation (Prof. Stiglitz is upset about the global cooperation): unable to supply vaccine, cannot egt the low cost of production

Country’s Government conduct government purchases (about 25% U.S. GDP), But developing countries and emerging markets do not have ability of finance the economy recovery by “G”.

SDR of CB: about to move money from CB to Treasury

Make funds recyclable

Problems of debts. We nned deep or restructure and cooperate between private and public sectors to solve the problems of extra debts.

Climate Risks

Weather uncertainty. Extreme weather.

Transformation to neclear energy.

Maket not works well. Asset price changes as well.

Systematic Consequence.

Wrong valuation of financial sectors

Banks need to ensure not over-exposure to value risks

Gov needs to response by policy that not allow risks to be tranfered to private sectors. i.e. ensure all mortgages are green mortgage.

Financial Secors commisions to allocate.

Companies also need to allocate and disclose financial risks.

China – Debt Finance + Real Estate

The economy relies highly on real estate, so highly exposed to debts problems. Therefore, alternative modes can be chosen.

more equity finance than debt finance. However, equity finance needs more information, and then better regulation. Equity based finance is better to absorb risks.

Focus on more small business lending. Use small business loan to stimulate the economy.

More public investment. Private sectores are polluted (driven by tendency of profitability). Thus, public sectors need to work and help movement from rural to city and further make city better. (common prosperity).

A transformation to service dominant mode.

Public investment is the engine of economy.

A country with rapid tranformation would be the winner.

朱民 (清华大学国家金融研究院院长,前IMF副总裁,央行副行长,中行副行长)

2022通胀之剑+央行的挑战

p.s. 参考Dalio经济weather取决于1. 经济增长; 2. 通胀。

Facts:

通胀呈现国际国与国之间不同,国内产业间不同的趋势。

全球:大宗商品价格上升 PPI上升,能源价格上升. PPI+CPI剪刀差导致企业利润被严重压缩。

问题:通胀,暂时性 or 持久性?— Ideas:持久性

Demand side: 需求持续上升,由于Fiscal & Monetary Policy的传递最终传向demand side

Supply side: cannot be stable coz covid continues + fluctuations of econ

大宗商品价格上升 (主要 油+能源+稀有金属),价格上升的来源为:1. supply structure changes;2. Targets of carbon neturality

Labour Market: 劳动力参与率低 low skill workers 导致unemployment。但是demand高,i.e. 卡车司机+港口集装箱问题。 最终导致low skill workers wage 上升 => 导致 all wages 上升。

Summary: structural inflation becomes persistent because both supply and demand sides changes. Fed are less affected to the inflation.

Future

U.S. debts 提升 interest rate下降 => achieve a balance。 但是当Fed要提高 interest rate收缩经济时,U.S. unable to pay back debts because of higher cost of interest payment. 最终导致 interest 难以提升的问题。

Mechanism Design: start with the outcomes, then work backward to find what mechanism can create that outcomes.

E.G. Seperate a cake to two kids. Aims to make those kids think they get same size. Ideal way to do so is halve the cake. However, kids may not consider sizes are same. We the mechanism design does is 1. as one kid to cut, and then 2. ask the other kid to choose a piece.

Two Realistic Problems can be solved by mechansim design.

1. Supply Chain Disruption: Economy is complex that there are goods and inputs, and producers get multi-sources.

Problems: producer does not seek multi-sources, coz they would prefer protect itself & its downstream by using single source supply chain. => supply side market is inefficient.

Solve: Government conduct i.e. 1. government subsidies to achieve multi-sources; 2. government encourage producers through other ways.

By government is the mechanism

Climate changes: Human emission gas into atmosphere. A firm that uses coal to generate electicity has no incentives to switch to clean energy, coz 1. high cost of tranformation; 2. CO2 has less effects on that certain firm.

Solution: conduct carbon tax. 1. reduce carbon uses; 2. high cost of coal encourage firms to switch to clean power.

Carbon Tax is the mechanism

Chinese Government did good:

carbon trade system (,which is similar to carbon tax). Also, what banks can do higher rate for high carbon emission firms (my simple idea).

ban Cryptocurrency (加密货币). Cryptocurrency would reduce the effects of monetary policy, coz people would instead use Cryptocurrency.

陆磊 (国家外汇管理局副局长)

PPI 上涨来自 supply shocks,上游利润上升,CPI上涨来自demand shocks,下游利润下降(利润被上游收割)。

高质量发展: 工具+动力

工具:

需求侧:宏观调控需要continuous & persistent & transparent

供给侧:增强competitivity,竞争性由technology带来。

结构:优化分配(见李扬)。

Green Finance。

动力:

改革创新 – 灵活有效的fiscal policy

发展源泉激励

Focus on also the liquidity risk (, which exceeds the credit risks already)

Jeffrey Sachs

In the long-term future, there is a fundamental changes of the realtionship between China and U.S.. Need strengthen the cooperation.

At the end of North Atlantic dominant, Asia takes doninant instead. Geographic driven by economic divergence,

Environmental Crisis – Fragile ecosystem

Demographic changes. Massive urbanisation.

Common prospertiy – demand for social inclusion.

Smart machines and digital socity

Wealth and well-being. How to shift the focus from wealth to well-being.

All countries, governments need to consider the global environment regulation goal.

Smart chiens and technology declines labour demands => reallocation of wealth (conflicts exist that the wealthy people rejects to pay higher tax)

The Arrow-Pratt coefficient of absolute risk aversion

Definition (Arrow-Pratt coefficient of absolute risk aversion). Given a twice differentiable Bernoullio utility function \(u(\cdot)\),

$$ A_u(x):=-\frac{u”(x)}{u'(x)} $$

Risk-aversion is related to concavity of \(u(\cdot)\); a “more concave” function has a smaller (more negative) second derivative hence a larger \(u”(x)\).

Normalisation by \(u'(x)\) takes care of the fact that \(au(\cdot)+b\) represents the same preferences as \(u(\cdot)\).

In probability premium

Consider a risk-averse consumer:

1. prefers \(x\) for certain to a 50-50 gamble between \(x+\epsilon\) and \(x-\epsilon\).

2. If we want to convince the agent to take the gamble, it could not be 50-50 – we need to make the \(x+\epsilon\) payout more likely.

3. Consider the gamble G such that the agent is indifferent between G and receiving x for certain, where

$$G= \begin{cases} x+\epsilon, & \text{with probability $\frac{1}{2}+\pi$}.\\ x-\epsilon, & \text{with probability $\frac{1}{2}-\pi$ } \end{cases}$$

4. It turns out that \(A_u(x)\) is proportional to \(\pi/\epsilon\) as \(\epsilon \rightarrow 0\); i.e., \(A_u(x)\) tells us the “premium” measured in probability that the decision-maker demands per unit of spread \(\epsilon\).

ARA.

Decreasing Absolute Risk Aversion. The Bernoulli function \(u\cdot)\) has decreasing absolute risk aversion iff \(A_u(\cdot)\) is a decreasing function of \(x\). Increasing Absolute Risk Aversion… Constant Absolute Risk Aversion – Bernoulli utility function has constant absolute risk aversion iff \(A_u(\cdot)\) is a constant function of \(x\).

Relative Risk Aversion

Definition (coefficient of relative risk aversion). Given a twice differentiable Bernoulli utility function \(u(\cdot)\),

$$ R_u(x):=-x\frac{u”(x)}{u'(x)}=xA_u(x) $$

There could be decreasing/increasing/constant relative risk aversion as above.

Implication: DARA means that if I take a 10 gamble when poor, I will take a10 gamble when risk. DRRA means that if I gamble 10% of my wealth when poor, I will gamble 10% when rich.

Ramsey (1928), followed much later by Cass (1965) and Koopmans (1965), formulated the canonical model of optimal growth for an economy with exogenous ‘labour augmenting technological progress. The R.C.K model (or called. Ramsey (Neo-classical model) can be considered as an extension of the Solow model but without an assumption of a constant exogenous saving rate.

Assumptions

Firms

Identical Firms.

Markets, factors markets and outputs markets, are competitive.

Profits distributed to households.

Production fucntion with labour augmented techonological progress, \(Y=F(K,AL)\). (Three properties of the production: 1. CRTS; 2. Diminishing Outputs, second derivative<0; 3. Inada Condition.)

\(A\) is same as in Solow model, \(\frac{\dot{A}}{A}=g\). Techonology grows at an exogenous rate “g”.

Households

Identical households.

Number of households grows at “n”.

Households supply labour, supply capital (borrowed by firms).

The initial capital holdings is \(\frac{K(0)}{H}\)., where \(K(0)\) is the initial capital, and \(H\) is the initial number of households.

Assume no depreciation of capital.

Households maximise their lifetime utility.

The utility fucntion is constant-relative-risk-aversion (CRRA).

The lifetime utility for a certain household is represented by,

We denote \(w(t)=W(t)/A(t)\) as the efficient wage rate, then we get,

$$ w(t)=f(k(t))-k(t)f'(k(t)) $$

Another key assumption of this model is,

$$ \dot{k}(t)=f(k(t))-c(t)-(n+g)k(t) $$

, which represents the actual investment (outputs minus consumptions), \(f(k(t))-c(t)\); and break-even investment, \((n+g)k(t)\). The implication is that population growth and technology progress would dilute the capital per efficient work.

The difference with the Solow model is that we do not assume constant saving rate “s” in \(sf(k)\) now, instead we assume the investment as \(f(k)-c\).

Households

The budget constraint of households is that: the PV of lifetime consumption cannot exceed the initial wealth and the lifetime labour incomes.

, where \(R(t):=\int_{\tau=0}^ t r(\tau) d\tau\) to represent the discount rate overtime. When \(r\) is a constant, \(R(t)=r\cdot t\) and \(A(t)=A(0)e^{rt}=A(0)e^{R(t)}\).

We plug the \( \begin{cases} C(t)=A(t)c(t)\\L(t)=L(0)e^{nt}\\A(t)=A(0)e^{gt} \end{cases} \) into households’ lifetime utility function (objective function), and then get the,

, where \(B:=A(0)^{1-\theta} \frac{L(0)}{H}\) and \(\beta:=\rho-n-(1-\theta)g\) (we need \(\beta>0\) to make the utility function convergence), and the utility function is, \(u(c_t)=\frac{c_t^{1-\theta}}{1-\theta}\).

The budget constraint is the households’ lifetime budget constraints divided by \(A(0)\) and \(L(0)\),

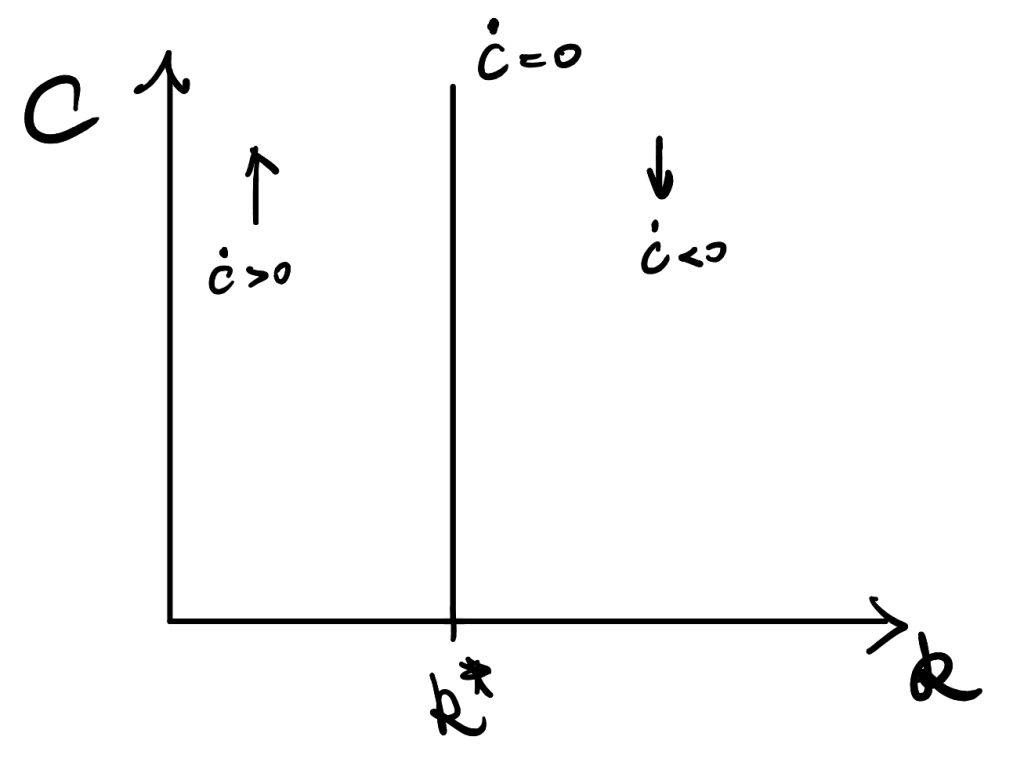

Therefore, we find the time-path of consumption depends on \(f'(k)\). We define \(k*\) is the solution when \(f'(k)=\rho+\theta g\). So, at \(k^*\), the numerator of RHS equals zero.

As \(f(k)\) is an increasing function but with diminishing returns, so \(f”(k)<0\) and that means \(f'(k)\) is a decreasing function in k. Thus,

at \(k<k^*\), \(f(k)>\rho+\theta g\) and \( \frac{\dot{c_t}}{c_t} >0\);

at \(k>k^*\), \(f(k)<\rho+\theta g\) and \( \frac{\dot{c_t}}{c_t} <0\).

Figure 1

The dynamics of k

We recall the assumption,

$$ \dot{k}(t)=f(k(t))-c(t)-(n+g)k(t) $$

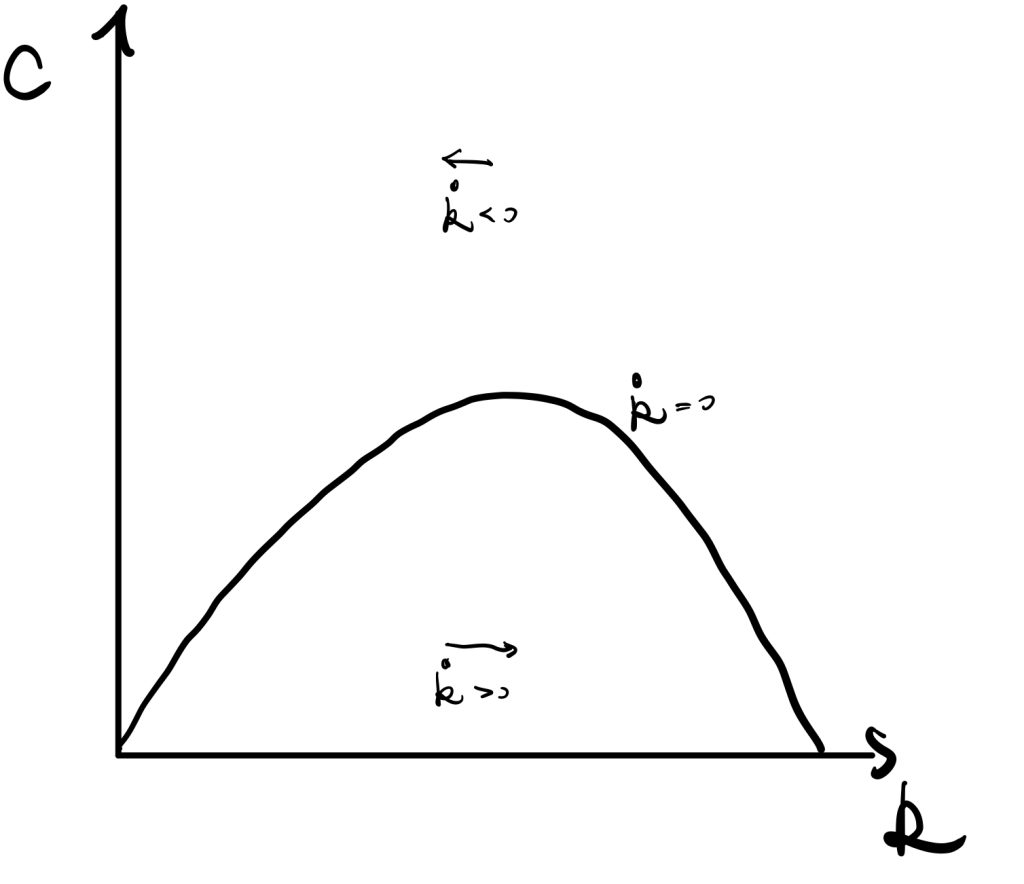

At \(\dot{k}=0\), consumption, \(c(t)=f(k(t))-(n+g)k(t)\), equals outputs minus break-even investment.

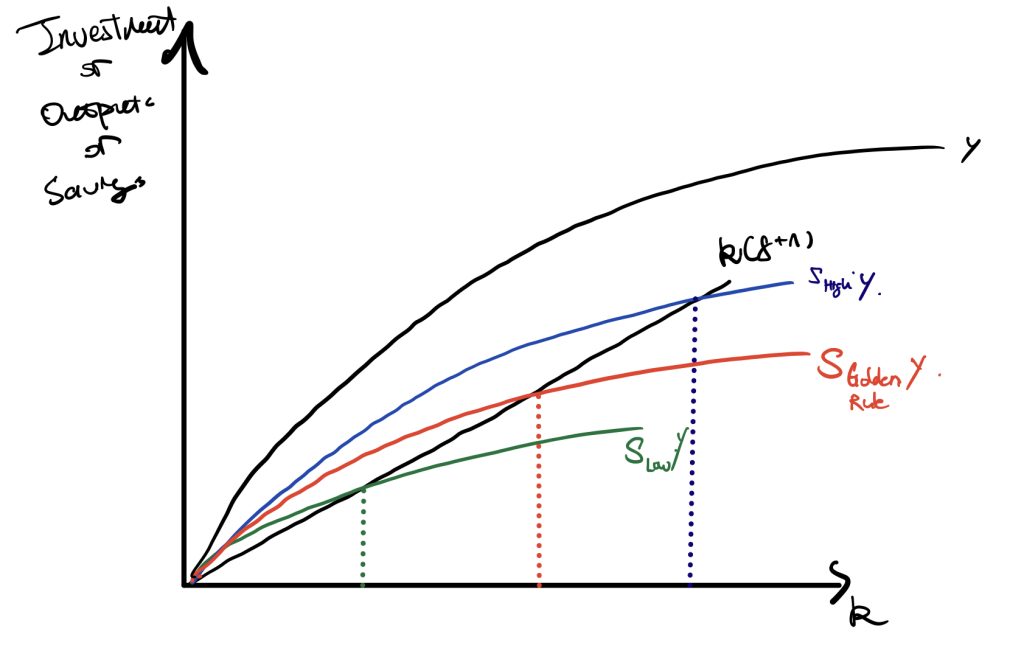

We now consider the Solow model without the depreciation term. Recall the difference between the RCK model and the Solow model is that we do not assume a constant saving rate over time, but other things keep similar. Thus, the term \(c(t)\) is “equivalent” to \(sy\) in Solow model.

Figure 2

In the Solow model, changes in saving rate would change the magnitude of \(sy\) curve. The Golden Rule saving rate is “s” that maximises consumption (the difference between Y and the interaction between \(sy\) and \(k(g+n)\)). The shape of the production function determines the property of the Golden Rule saving rate.

An equilibrium level of consumption is determined in mainly two steps. 1. the interaction between saving \(sy\) and \((n+g)k\) determines the \(k^*\). 2. plug \(k^*\) back to \(sy\) and find the difference between outputs and savings to get consumption.

We here focus on the second step, the equilibrium level of \(k^*\) determines consumption and thus consumption is a function of \(k^*\). At a lower saving rate (see Figure 2), \(k^*\) is too small, so there is less consumption. At a higher saving rate, \(k^*\) is too large, so there is also less consumption. Therefore, we can find that consumption is in a quadratic form w.r.t. \(k^*\).

Figure 3. \(c(t)=f(k(t))-(n+g)k(t),\ \dot{k}=0\)

$$ (s\downarrow) \Leftrightarrow k \downarrow \to c \downarrow$$

$$ (s\uparrow) \Leftrightarrow k \uparrow \to c \downarrow$$

Or, we can consider consumption as the difference between \(y\) and \((n+g)k\). The wedge like area gets large and then shrinks.

Overall, the above facts make the \(\dot{k}=0\) curve.

Recall \( \dot{k}(t)=f(k(t))-c(t)-(n+g)k(t) \).

Above the curve where \(c\) is large, then \(\dot{k}<0\) so \(k\) decreases. Below the curve where \(c\) is small, then \(\dot{k}>0\) so \(k\) increases. Implication is that if less consumption, then more saving, \(\dot{k}\) increases.

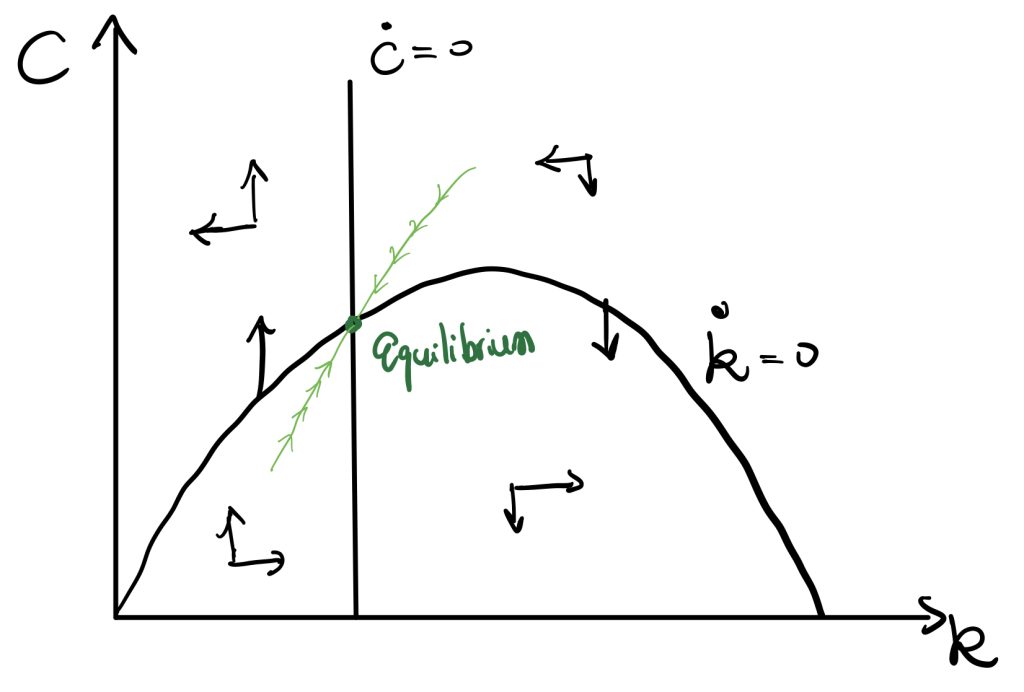

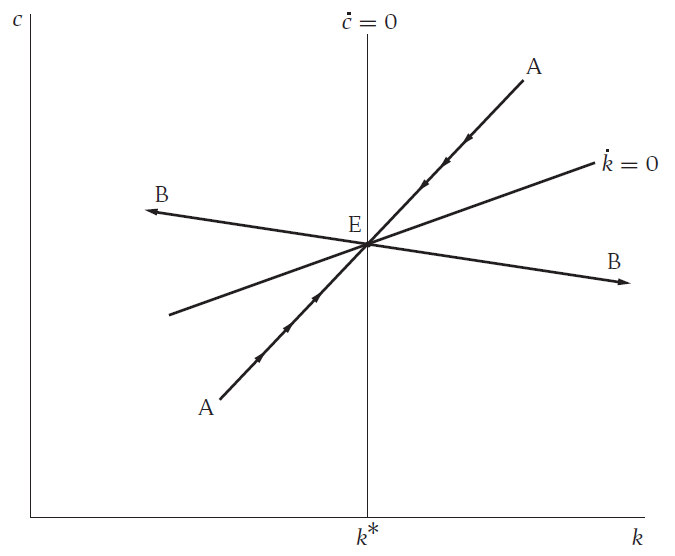

Phase Diagram.

Figure 4

Combining Figure 1 and Figure 3, we get the above Phase Diagram. The equilibrium is shown in the figure above.

P.S. We can prove that the equilibrium is less than Golden Rule level \(k^*_{GoldenRule}\) (which is the maximum point in the quadratic shaped curve). The proof is the following,

The value of k at \(\dot{c}=0\) is \(f'(k)-\rho-\theta g=0\), and the Golden Rule level is \(c=f(k)-(n+g)k\) (as we illustrated before), and take f.o.c. w.r.t. k to solve the Golden rule k. \(\frac{\partial c}{\partial k}=0 \to f'(k)=n+g\). Therefore, we get,

$$ \begin{cases} f_1:=f'(k_{equilibrium})=\rho+\theta g \quad\text{equilibrium in phase diagram}\\ f_2:=f'(k_{GoldenRule})=n+g\quad\text{golden rule level}\end{cases}$$

$$ \rho+\theta g>n+g \quad \text{by our assumption of \beta convergence}$$

So, we get,

$$ f_1>f_2 $$

$$ k_{equilibrium}< k_{GoldenRule} $$

Thus, we find the equilibrium level capital per efficient workers, \(k_{equilibrium}\), must be less than the Golden Rule level \( k_{GoldenRule} \).

From the phase diagram, we can get the saddle path that can achieve equilibrium.

BGP

At the Balanced Growth Path, the economy is in equilibrium. So the time-paths satisfy \( \frac{\dot{c}}{c}=0, and \frac{\dot{k}}{k}=0 \). Therefore, we can get the BGP of others,

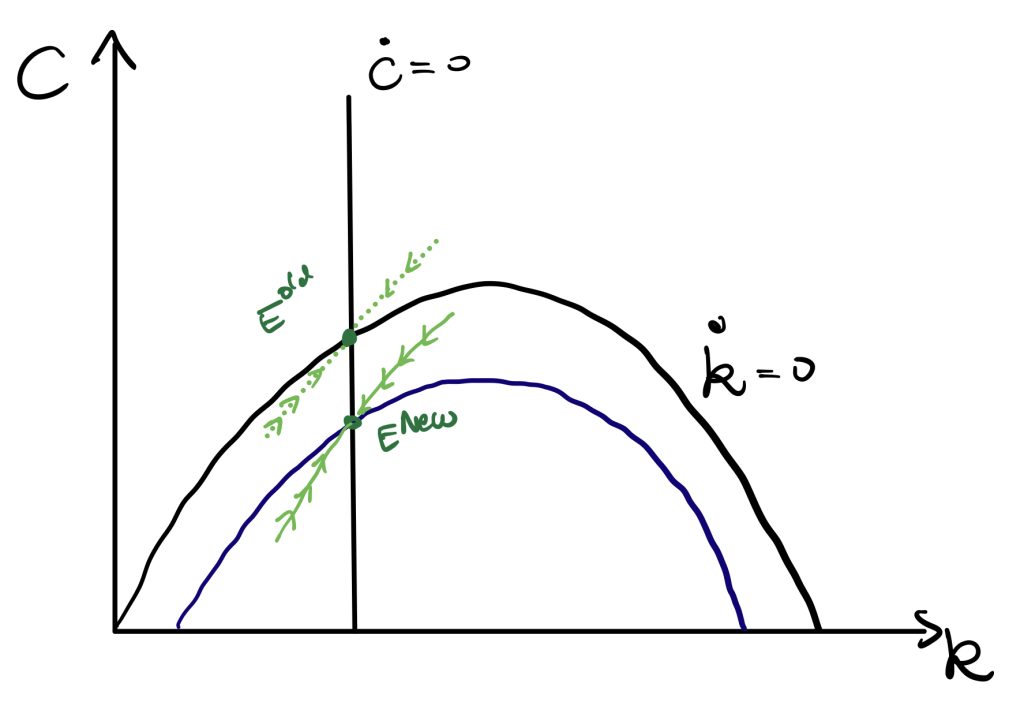

Assumption: government conducts government purchases, \(G(t)\). The government purchases do not affect the utility of private sectors, and future outputs. Government finances, G(t), by lump-sum taxes.

We can consider the crowding-out effect. Under full employment, government purchases take away part of the consumptions. In our case, government spending takes away some of the savings. Therefore, the dynamics of capital per efficient workers become (the minus government spending term shifts the curve downward by G(t)),

$$\dot{k}(t)=f(k(t))-c(t)-G(t)-(n+g)k(t)$$

In short, government purchases would make the economy achieve a new equilibrium where there is less consumption but the same capital (investment from the private sector) level. Also, the saddle path moves downward.

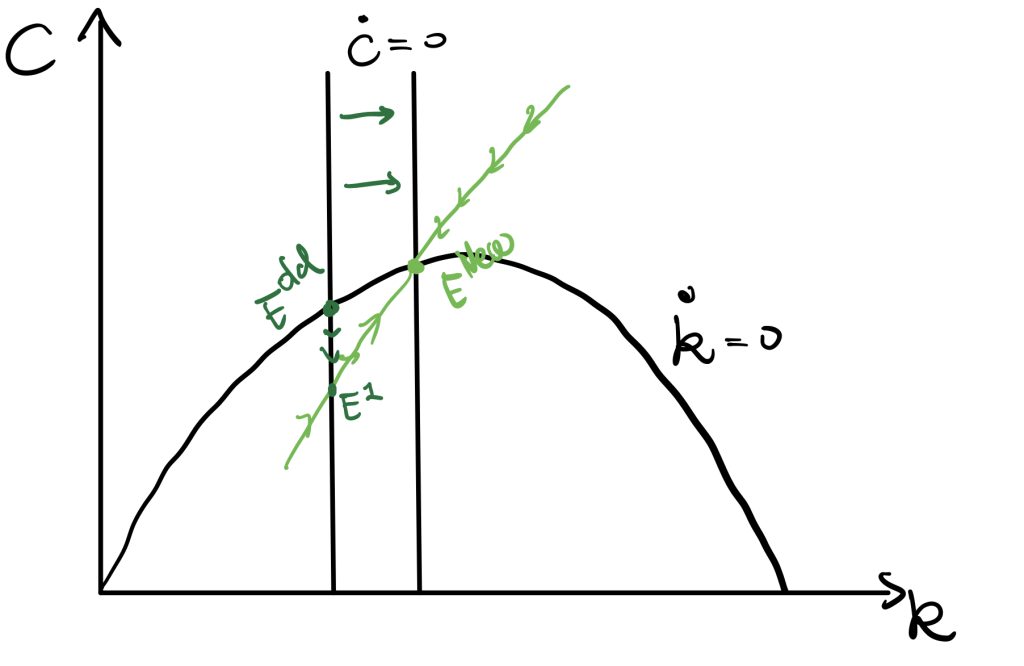

\(\rho\) Changes

A fall in \(\rho\) can be considered as the effect of monetary policy. A fall in \(\rho\) would result in a movement of \(\dot{c}=0\) curve to the right by the equality, \(\frac{\dot{c}}{c}= \frac{r(t)-\rho-\theta g}{\theta} =\frac{f'(k)-\rho-\theta g}{\theta}\).

P.S. \(\dot{c}=0 \Leftrightarrow f'(k)=\rho-\theta g \to k=f’^{-1}( \rho-\theta g )\)

As \(\rho\) changes, a new path generates. The economy is at \(E^1\), and then follows the new path moving to \(E^{new}\). We would finally end up with a new equilibrium with higher consumption.

We replace this non-linear equation with the linear approximation, so we take the first order Taylor approximation around the equilibrium \(k^*\) and \(c^*\).

We then replace \( \dot{c}=\frac{f'(k)-\rho-\theta g}{\theta}c \) ) and \( \dot{k}=f(k(t))-c(t)-(n+g)k(t) \) into \( \dot{k}_{approx} \) and \( \dot{c}_{approx} \). Also, we denote \(\tilde{c}=c-c^*\) and \(\tilde{k}=k-k^*\).

From the above two equations we can find growth rate of \(\dot{\tilde{c}}_{approx}\) and \( \dot{\tilde{k}}_{approx} \) depend only on the ratio, \(\frac{\tilde{k}}{\tilde{c}}\).

Later, we apply a very strong assumption that \(\tilde{c}\) and \(\tilde{k}\) changes at the same rate, and also the rate make LHS of two equations equal. By this assumption, we denote,

We can see \(\mu\) must be negative, otherwise the economy cannot converge (see the path BB). If \(\mu<0\), the economy would be in the path AA instead. The path is the saddle path of R.C.K. model.

Applying such as the Cobb-Douglas form production, we can plug second derivatives of the production into \(\mu\) and get the speed of adjustment.